Asian equity markets are enjoying a welcome bounce, powered by a sharp rebound in semiconductor and broader technology stocks, yet the move feels more cautious than euphoric. Gains in chipmakers from Tokyo to Seoul have pulled regional indices higher, but a parallel rise in oil prices and renewed inflation worries is clearly tempering how far investors are willing to chase risk. This tension between sector-specific optimism and macro uncertainty is shaping the tone of the session—and the opportunity set for active and simulated traders alike.

Chip Rebound Lifts Asian Equities

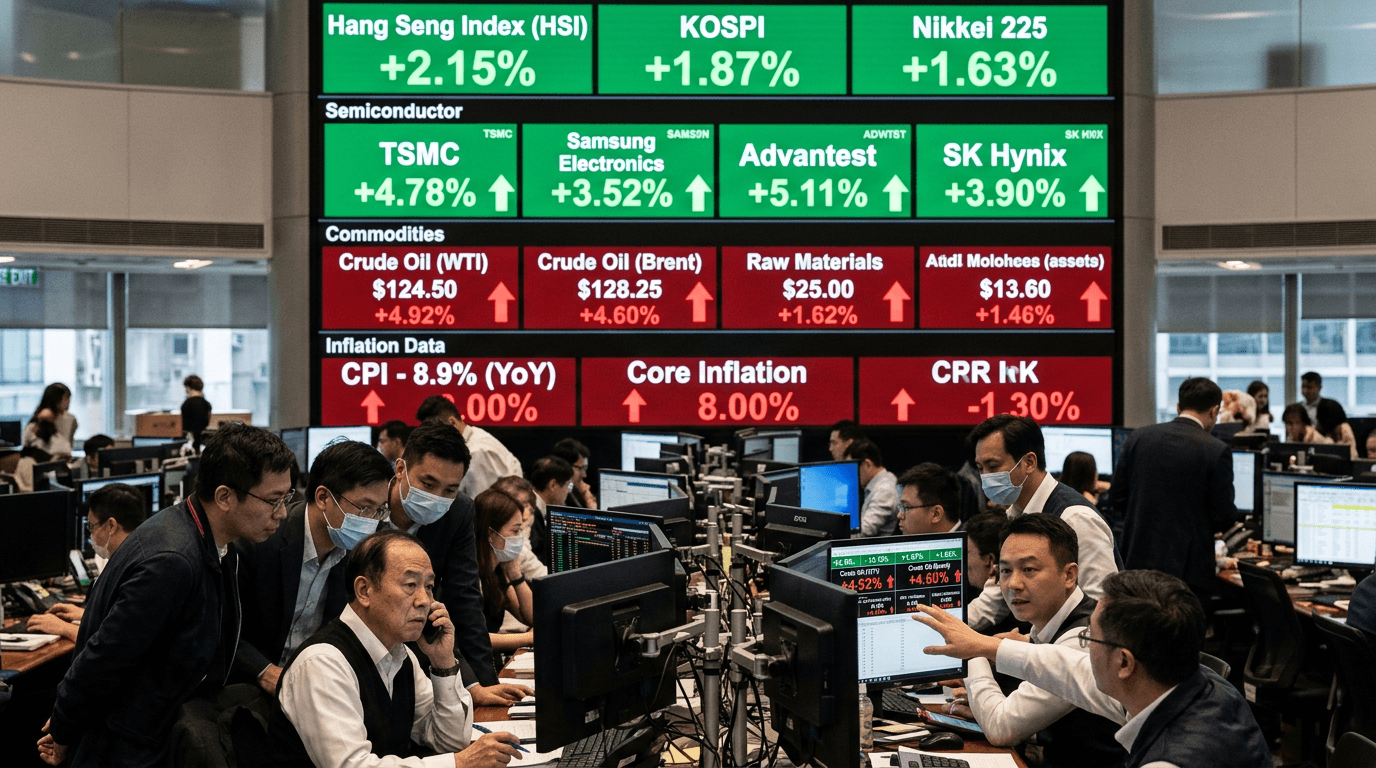

The immediate driver of the move higher in Asian shares is a strong recovery in semiconductor names, following upbeat trading and earnings news from major U.S. chipmakers.[1][2][7] After a bout of profit-taking in AI-related stocks, investors are re-engaging with the theme, seeing the recent pullback as an opportunity rather than the end of the cycle.

In Japan, leading chip equipment makers such as Tokyo Electron and Advantest have posted outsized gains, reflecting renewed confidence in demand for high-end fabrication tools tied to AI and data center growth.[2] In South Korea, memory giants SK Hynix and Samsung Electronics have rallied as investors rotate back into names at the heart of the global AI hardware stack.[1][6] Taiwan’s TSMC and key suppliers like Foxconn and other contract manufacturers have also participated, underscoring how broad the semiconductor supply chain is—and how quickly capital flows can return when sentiment shifts.[9]

This rebound is not happening in isolation. Wall Street’s race back into chip stocks, particularly companies tied to AI accelerators and advanced processors, has provided a clear signal that the recent correction was more about positioning than fundamentals.[7] Asian tech investors are effectively echoing that view: earnings visibility for leading chipmakers remains solid, capex plans from cloud and hyperscale buyers are intact, and the long-term narrative around AI-driven demand is unchanged.

For traders, the key takeaway is that sector momentum can reassert itself quickly once selling pressure abates. Semiconductors remain a beta-rich, narrative-driven segment of the market, offering both opportunity and volatility for those trading equity index futures, single-stock CFDs, or simulated portfolios.

Oil And Inflation: Why Risk Appetite Stays Capped

Offsetting the tech enthusiasm is a less cheerful story in commodities. Oil prices have been grinding higher, and that is reigniting concerns over the inflation path just as many investors were hoping for a smoother disinflation narrative.[2] Rising energy costs tend to feed into transport, manufacturing, and eventually consumer prices, complicating central banks’ task and raising questions about the durability of any equity rally.

In the current cross-asset backdrop, every uptick in crude is interpreted through an inflation and policy lens. Higher oil means potentially stickier headline inflation, which in turn can keep interest rates elevated for longer than equity bulls would prefer. That dynamic is especially important for growth and tech names, where valuations are sensitive to discount rates and long-term cash flow assumptions.

This is why, even as chip stocks are surging, broader risk appetite feels constrained. Investors are willing to buy the semiconductor story, but they are doing so with one eye firmly on macro risk—particularly the possibility that renewed price pressures could delay rate cuts or even revive hawkish rhetoric from major central banks. For cyclicals, transport, and energy-intensive industries, that creates a more challenging backdrop and encourages selective rather than broad-based risk-taking.

Cross-asset Signals: What Futures Are Telling Us

Index futures and related derivatives are reflecting this mixed tone. Equity futures tied to major Asian benchmarks are generally pointing modestly higher, supported by tech strength and attempts to rebuild after recent volatility.[6] However, the degree of follow-through is limited; gains are not uniform across sectors, and volume tends to concentrate in technology and AI-related names rather than in the entire index.

Fixed income and foreign exchange markets, meanwhile, are showing the typical signs of macro caution. When oil rises and inflation concerns resurface, government bond yields can move higher on expectations of prolonged tight policy, while some investors seek safety in high-quality duration. At the same time, currencies of energy-importing countries may come under pressure, whereas those of commodity exporters can find support. These moves influence equity sentiment indirectly, as they reshape expectations for growth, corporate margins, and capital flows.

For futures traders, the cross-asset message is clear: this is not a “risk-on everywhere” tape. Instead, it is a market where positive micro stories in chips and AI are battling with negative macro impulses from energy and inflation. Strategy-wise, that tends to favor relative-value trades—such as long semiconductors versus broader indices—or volatility strategies that exploit the uncertain policy path, rather than simple directional bets on indices alone.

Implications For Traders And Simulated Finance Players

For participants on a Simulated Finance (SimFi) platform, this environment is an ideal case study in how sector themes and macro forces interact. On the one hand, chipmakers are demonstrating how quickly sentiment can swing when a dominant narrative—AI adoption, data center expansion, next-generation compute—remains intact. On the other, the oil-led inflation story shows how fragile that enthusiasm can become when broader economic risks loom in the background.

A practical approach in simulated trading is to construct scenario-based portfolios. One scenario assumes that semiconductor momentum persists and oil stabilizes, allowing tech-led indices to grind higher. Another assumes that oil keeps rising, inflation expectations re-anchor higher, and central banks push back against easing hopes—pressuring valuations, particularly in rate-sensitive growth segments. Testing strategies across these scenarios can help traders understand how their exposure behaves under different combinations of micro and macro shocks.

Risk management is central here. Even in simulation, applying position sizing rules, stop-loss triggers, and diversification across sectors and asset classes is crucial. Tech and AI names can deliver strong returns, but they are also prone to rapid drawdowns when sentiment turns or when macro headlines catch the market off guard. Balancing sector conviction with hedges—via index futures, options, or defensive sectors—is a core skill this environment can help build.

Key Takeaways For The Next Session

First, the chip rebound is genuine and broad-based across Asia, reflecting renewed confidence in AI-linked demand and positive signals from U.S. peers.[1][2][7][9] This supports a constructive view on technology, particularly leading-edge semiconductors and equipment makers, even after recent volatility.

Second, the rally is not yet a full-blown risk-on wave. Oil’s climb and the associated inflation worries are capping risk appetite, reminding investors that macro conditions remain uncertain and that policy risks are still in play.[2] That tension explains why gains are strongest in select tech names rather than evenly distributed across all sectors.

Third, the cross-asset picture—equity futures, bonds, FX, and commodities—encourages nuanced positioning. Traders who can read these signals and express views through relative trades, hedges, and diversified exposure are better placed to navigate the current backdrop.

Finally, for both live and simulated traders, this is a rich learning environment. It rewards understanding of sector fundamentals, sensitivity to macro dynamics, and disciplined risk management. Asian shares may be rising on a chip rebound, but the true test for portfolios will be whether they are prepared for the next move in oil, inflation, and policy expectations.