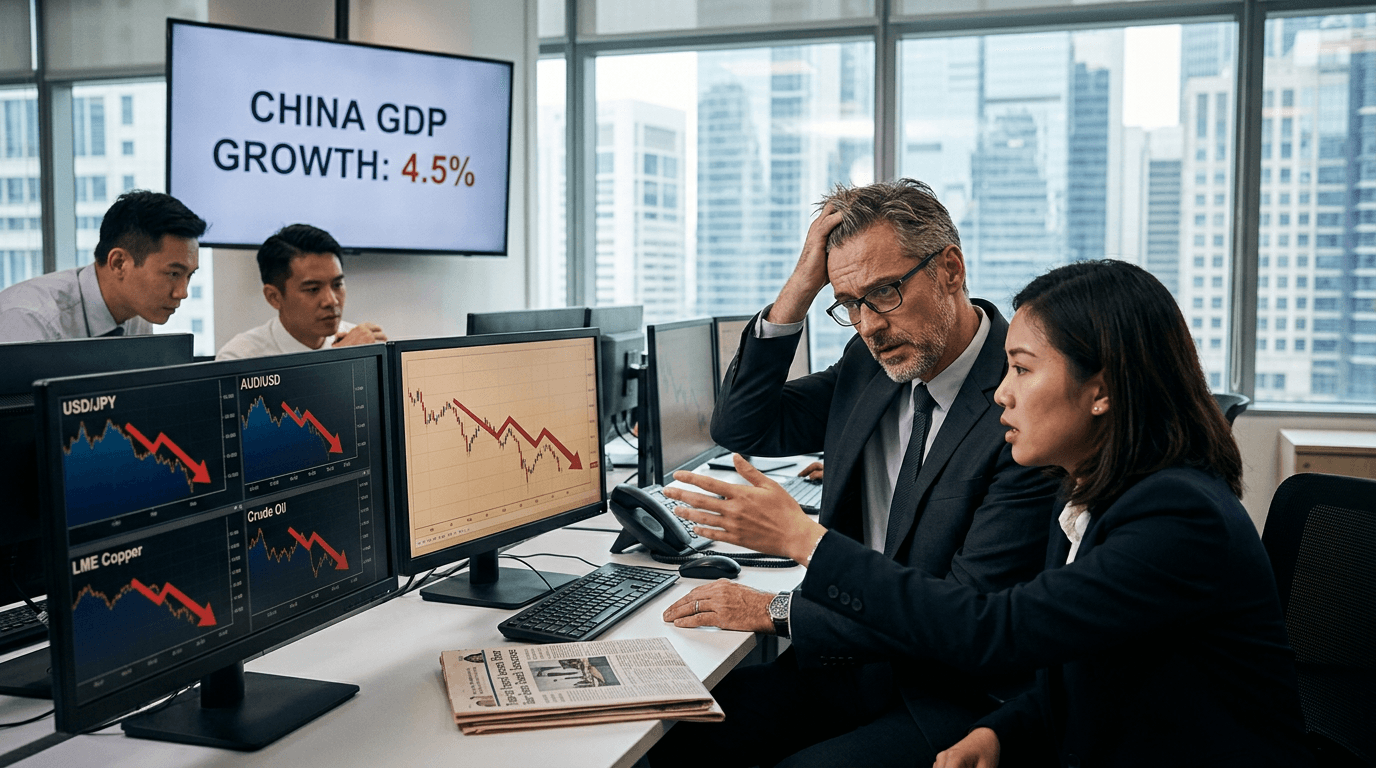

China’s latest GDP release has sent a clear signal to global markets: the world’s second‑largest economy is slowing, and the ripple effects are hitting Asian FX and commodity futures. Official data showed that gross domestic product grew 4.3% year‑on‑year in the second quarter of 2026, the weakest pace in more than three years and below market expectations.[8][9] For traders, this is not just another data point—it is a macro shock that reshapes the landscape for currencies and commodities tied to China’s growth story.

CHINA’S SLOWEST GROWTH IN OVER THREE YEARS

China’s 4.3% Q2 GDP print marks the slowest quarterly growth since the end of 2022, underscoring the fragility of its post‑pandemic recovery.[8][9] The figure missed consensus forecasts of around 4.5% and fell below the government’s target range of 4.5% to 5%, underlining the challenge Beijing faces in sustaining momentum.[1][8][9]

Beneath the headline number, the slowdown reflects a stark imbalance: robust factory output and exports contrasted with weak domestic demand.[1][9] Export growth has been buoyed by global demand for AI‑related chips and data‑processing equipment, with semiconductor and computing gear shipments surging year‑on‑year.[9] At the same time, consumption and investment have struggled under the weight of a prolonged property slump and the fallout from the earlier oil shock.[1][9]

Recent data highlight this uneven picture. Industrial production rose 5.3% in June, beating expectations and pointing to solid manufacturing activity.[9] Retail sales, however, grew just 1% year‑on‑year, a modest upside surprise but still indicative of cautious households and subdued consumer confidence.[9] Taken together, the numbers suggest an economy driven by external demand and high‑tech exports, but constrained by domestic structural issues—especially real estate and local government debt.[1][9]

Market Reaction: Pressure On Asian Fx

The downside surprise in China’s growth is weighing on China‑sensitive currencies, particularly the Australian dollar (AUD), New Zealand dollar (NZD), and Asian emerging‑market FX.[1] The transmission channel is straightforward: weaker Chinese growth implies softer demand for imports, lower pricing power for commodity exporters, and increased risk aversion across regional markets.

For AUD and NZD, the impact is especially pronounced. Both economies are heavily tied to China through trade in bulk commodities—iron ore, coal, and agricultural products. When Chinese growth undershoots expectations, markets tend to reassess the outlook for these exports, pricing in slower volumes and potential downside to terms of trade. That reassessment typically translates into selling pressure on AUD and NZD as traders rotate away from pro‑growth, commodity‑linked currencies toward defensive or yield‑safe havens.

Asian EM currencies, including those of export‑oriented economies in Southeast Asia, also feel the strain. Slower Chinese demand can mean weaker orders for intermediate goods, electronics components, and consumer products, adding uncertainty to regional manufacturing cycles. At the same time, concerns about global growth amplify risk‑off sentiment, prompting outflows from higher‑beta EM FX into more stable currencies.

For traders, one key takeaway is that China data are not just local events—they’re regional risk catalysts. Positioning around AUD, NZD, and Asian EM FX should increasingly factor in China’s structural growth trajectory, not just headline surprise on release day.

Commodity Futures Under Pressure

Industrial commodity futures are another direct casualty of China’s softer GDP print.[1] With a property slump weighing on construction and investment, markets reassess demand for building‑related materials such as steel, copper, and cement, along with the energy commodities that power industry.[1][9]

Metals linked closely to infrastructure and property—iron ore and steel, in particular—are highly sensitive to Chinese growth and policy expectations. A weaker‑than‑expected GDP number reinforces fears that China’s long real‑estate downcycle is far from over, limiting upside for bulk commodity prices. That can trigger selling in related futures contracts, steepening contango in some curves or compressing backwardation as demand expectations are revised down.

Energy markets, which had previously been roiled by the oil shock, now face a more nuanced backdrop: high prices have already acted as a drag on activity, and weaker Chinese growth raises questions about future demand intensity.[1] While AI‑driven manufacturing and export strength support some baseline of consumption, the overall demand profile looks less aggressive than in previous cycles, which can cap rallies and increase the likelihood of range‑bound trading in crude and refined products.

Industrial metals like copper—often viewed as a bellwether of global growth—are caught between two forces: the structural demand story from electrification and technology, and cyclical weakness from slower Chinese construction and manufacturing capex. The latest GDP data tilt that balance toward caution in the near term.

Policy Outlook And Macro Scenarios

With growth below target and domestic demand underperforming, markets are increasingly focused on Beijing’s policy response. Analysts expect policymakers to lean more on fiscal stimulus—through infrastructure spending, support for strategic sectors, and targeted measures to stabilize the property market—rather than aggressive monetary easing.[1] The central bank is seen as constrained by financial stability concerns and the need to manage currency dynamics amid global rate differentials.[1]

For FX and commodity traders, policy expectations matter as much as the data. A credible stimulus package aimed at shoring up domestic demand could, over time, restore confidence in the Chinese growth path, offering support to AUD, NZD, and industrial commodities. Conversely, incremental or narrowly targeted measures may fail to shift sentiment, leaving markets in a regime of lower trend growth and episodic risk‑off episodes around data releases.

Scenario analysis becomes essential

- In a “strong stimulus” scenario, traders might expect a rebound in China‑linked FX and a stabilization or recovery in metals and energy demand.

- In a “gradual adjustment” scenario, volatility could persist, with rallies in China‑sensitive assets fading as structural constraints reassert themselves.

- In a “no major policy pivot” scenario, the market could continue to price China as a lower‑growth, export‑heavy economy, with more muted commodity cycles and narrower ranges in regional FX.

Practical Takeaways For Traders And Simulated Finance Participants

For both live and simulated finance traders, the latest China GDP data offer several practical lessons.

First, correlations matter. China’s growth surprises have outsized impact on AUD, NZD, Asian EM FX, and industrial commodities. Monitoring how these assets respond around major data releases can help refine macro trading strategies and risk management.

Second, structural themes trump short‑term noise. The persistent property slump, weak consumption, and reliance on exports and high‑tech manufacturing suggest that China’s growth model is evolving.[1][9] Strategies that assume a return to pre‑pandemic “old China” driven by property and heavy industry may need updating. Instead, traders should think in terms of uneven sectoral impacts: technology and AI‑related exports can outperform even as domestic demand lags.

Third, use simulated environments to stress‑test portfolios. In a SimFi setting, traders can model different policy paths and growth scenarios—strong stimulus versus slow grind—and observe how regional FX and commodity positions behave. This kind of rehearsal is valuable preparation for real‑world trading when the next major China data release hits the tape.

Finally, keep an eye on the macro calendar. China’s GDP, industrial production, retail sales, and property indicators are now central inputs for any strategy involving Asian FX or industrial commodities. Integrating these releases into a systematic trading framework can help avoid being caught off‑side when the world’s second‑largest economy surprises markets—up or down.