Global markets were jolted as China announced a sweeping new round of tariffs on US goods, lifting duties on some products to an eye-watering 125–145% and explicitly warning that Washington must bear responsibility for the economic fallout. The move immediately hit risk sentiment, pressured US equity futures, and drove investors into classic safe havens in FX and US Treasuries, signaling that the US–China trade conflict is entering a more hostile phase rather than cooling down.

WHAT CHINA JUST DID – AND WHY IT’S SO IMPORTANT

China’s new measures target a broad basket of US imports, sharply increasing the cost of bringing many American products into the Chinese market. While the detailed product list is still being digested by analysts, the headline is clear: some lines will now face tariffs as high as roughly 125–145%, effectively pricing many US exports out of contention for Chinese buyers.

This escalation comes after a period in which both sides had partially backed away from the most extreme tariff levels reached during the height of the 2025 trade flare-up. Research from the Peterson Institute shows that after peaking at average tariffs of around 147.6% on US goods in mid‑2025, China later rolled those back to about 31.9% following negotiations.[5][7] In other words, Beijing is now deliberately moving back toward the kind of punitive rates associated with the most intense phase of the trade war.

The messaging is as significant as the numbers. Officials in Beijing explicitly framed the move as a response to US trade and technology policies, insisting that Washington must “bear responsibility” for any damage to global growth or supply chains. That framing matters because it reduces the political space for quick de‑escalation: when tariffs become a question of national resolve, compromise gets harder.

Trade Wars And Markets: Why Risk Sentiment Turned So Fast

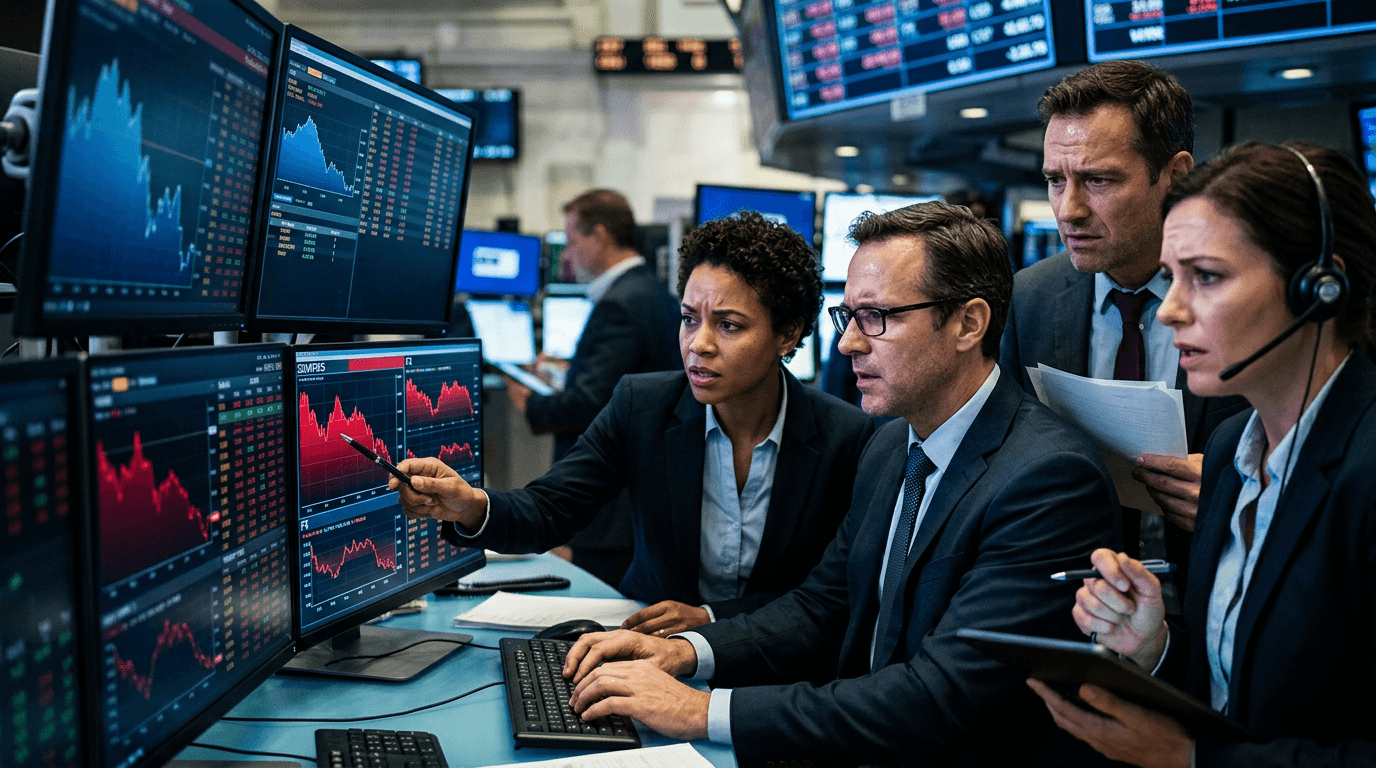

The immediate market reaction followed a familiar risk-off pattern.

US equity futures slipped as traders quickly marked down earnings expectations for companies heavily exposed to China, whether through exports, supply chains, or China-related revenue. The sectors most at risk typically include industrials, autos and parts, high-end machinery, certain tech hardware, and agricultural exporters, although the precise impact will depend on the final tariff list.

In FX, the announcement supported safe-haven flows. That usually means:

- Stronger demand for currencies like the Japanese yen and Swiss franc

- A bid for the US dollar versus higher‑beta currencies linked to global trade and commodities

- Selling pressure on emerging market currencies, particularly those closely tied to Asian supply chains

US Treasuries also caught a safety bid. When geopolitical or trade risks rise, investors often rotate out of equities and riskier credit into highly liquid, perceived “risk‑free” assets like US government bonds. That demand pushes Treasury prices up and yields down, especially on the long end of the curve.

For traders, the key point is that trade headlines can hit multiple asset classes at once. Equity futures, FX, rates, commodities, and even volatility indices all become tightly linked when the market’s dominant narrative is “growth risk from policy shocks.”

How These Tariffs Can Filter Into The Real Economy

Beyond the knee‑jerk market reaction, steep tariffs of 125–145% have real economic implications if they remain in place.

First, they act as a tax on bilateral trade. For many products, a tariff at that level is essentially prohibitive: Chinese importers will either switch to non‑US suppliers or, where that’s not possible, pass higher costs on to consumers or downstream manufacturers. That means:

- Lower export volumes for affected US firms

- Higher input costs for Chinese companies relying on US components or materials

- Potential price increases in end‑products, adding to inflation pressures in some niches

Second, tariffs tend to distort supply chains. Over time, firms respond to persistent trade barriers by re‑routing production, re‑sourcing inputs, or shifting final assembly to third countries. This was already visible in earlier phases of the US–China trade war, when production of some goods migrated to Southeast Asia and Mexico.[3][5] A renewed tariff spike could accelerate that trend, with long‑term implications for where value is created and captured in global manufacturing.

Third, there is the growth channel. Higher trade barriers are, in effect, a negative shock to global demand and efficiency. Studies of the previous rounds of US–China tariffs showed measurable drag on both economies and on global trade volumes.[5] With average Chinese tariffs having previously dropped back toward the low‑30% range,[7] a jump back to triple‑digit rates on key products would once again tighten the screws.

The macro impact will depend on how broad the new measures are and whether the US responds with further escalation. A contained, targeted move hurts specific sectors; a tit‑for‑tat spiral can start to weigh on GDP forecasts and central bank reaction functions.

Key Risks And Scenarios To Watch

From a trading and investing perspective, the path ahead will likely follow one of a few broad scenarios:

1. Controlled escalation Both sides maintain tough rhetoric, but the new tariffs are confined to specific sectors, and back‑channel talks continue. Markets stay volatile around headlines but gradually adapt as the new tariff structure becomes “the new normal.”

2. Tit‑for‑tat spiral Washington retaliates with its own round of sharply higher tariffs or new export controls, particularly in sensitive areas like semiconductors, batteries, or critical minerals, building on earlier US trade actions under Section 301 and Section 232 authorities.[3][5] In this scenario, risk assets could re‑price more sharply, with global equities, cyclical FX, and trade‑linked commodities under pressure, while volatility and safe havens gain.

3. Negotiated off‑ramp After an initial show of force on both sides, political incentives (such as growth concerns or domestic market stress) push Washington and Beijing back to the table. Tariffs may not fully reverse, but some reductions or exemptions could be traded for concessions in other areas.

For traders, assigning probabilities to these scenarios and updating them as new information emerges is more useful than trying to predict a single “correct” outcome.

What Traders And Investors Should Do Now

In an environment where policy risk is driving markets, a few practical principles can help:

- Map your exposure Identify which positions are directly tied to US–China trade: exporters with large China revenue, Chinese firms dependent on US tech or components, and economies plugged into the US–China supply chain. Equity indices, sector ETFs, and single names can all behave very differently depending on that exposure.

- Watch cross‑asset signals Equity futures, the US dollar, yen, Treasury yields, and credit spreads often move together when trade risk is in focus. Divergences between these markets can provide early clues about whether the narrative is intensifying or fading.

- Manage gap and headline risk Trade announcements tend to hit outside regular cash hours and can trigger gaps on open. Position sizing, use of options, and clear levels for invalidating a trade thesis become more important when the main driver is political news rather than scheduled data.

- Stress‑test scenarios Whether using a live account or a simulated environment, it is valuable to model how your portfolio would behave under deeper escalation: lower global growth, stronger dollar, weaker EM FX, and higher volatility. That exercise can highlight concentration risk before markets force a repricing.

Finally, keep in mind that trade wars rarely move in a straight line. Phases of escalation are often followed by partial truces, only to flare up again when political calendars or strategic priorities shift. For active traders, that means opportunity and risk go hand‑in‑hand: the key is having a framework, not just a reaction.