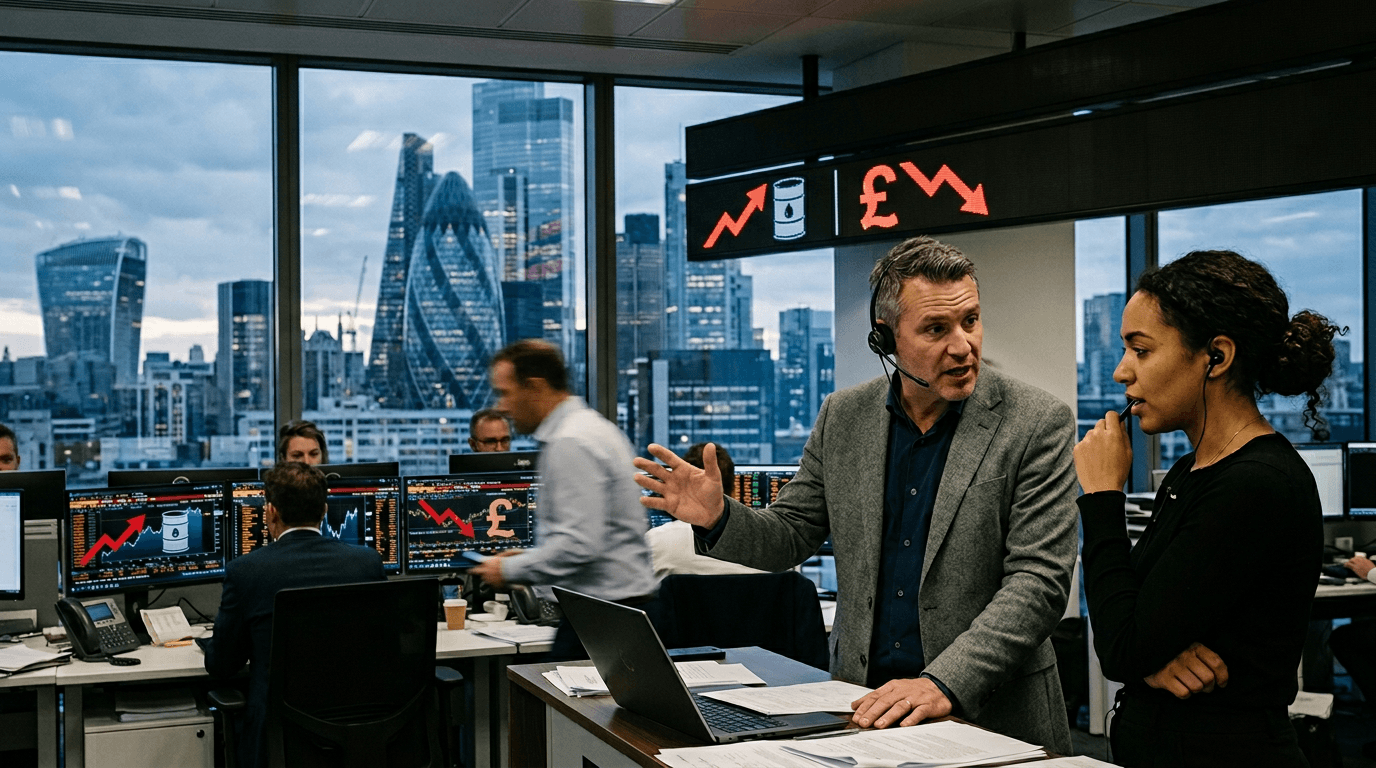

The global currency markets are experiencing a significant recalibration as multiple headwinds converge to pressure commodity-linked currencies and sterling alike. Rising oil prices driven by geopolitical tensions, combined with mounting domestic risks in the UK, have created a challenging environment for the British pound and other currencies tied to commodity exports. Recent trading data shows GBP/USD has retreated from February highs, with the pair now trading near 1.3407 and analysts warning of potential weakness toward the 1.3200-1.3400 support zone.[1][2]

The Perfect Storm: Oil Shock Meets Geopolitical Risk

The confluence of rising energy costs and geopolitical instability has become a defining feature of current market dynamics. When oil prices surge due to supply-side concerns or regional tensions, this typically signals broader economic headwinds ahead. Higher input costs ripple through global supply chains, raising inflation expectations and reducing consumer purchasing power. Simultaneously, geopolitical risk appetite tends to diminish, pushing investors away from growth-oriented assets and toward traditional safe havens like the US dollar and Japanese yen.

For commodity-dependent economies, this scenario presents a double bind. While rising energy prices might theoretically benefit oil-exporting nations, they often signal demand destruction elsewhere in the economy. The fear of weaker global growth combined with input cost pressures creates a risk-off sentiment that overwhelms any temporary benefit from higher commodity prices. In this environment, investors reassess their positioning in currencies linked to commodity exports, leading to selling pressure across emerging market and commodity FX complexes.

Commodity Currencies Under Siege

The term "commodity currencies" refers to those currencies of nations heavily dependent on exporting raw materials—including currencies like the Australian dollar, Canadian dollar, and Norwegian krone, alongside the British pound given the UK's energy sector exposure. These currencies tend to appreciate when commodity prices rise and global growth expectations are strong, but they face selling pressure in the opposite scenario.

Historical exchange rate data from early 2026 illustrates this dynamic. GBP/USD averaged 1.3535 for the year through early March, but the worst rate—1.3354 on March 3rd—reflects the pressure building as oil prices and risk concerns escalated.[1][4] The move from February highs near 1.3670-1.3810 down toward March lows demonstrates how quickly sentiment can shift when multiple negative factors align.

When global demand concerns emerge, commodity prices typically weaken, reducing export revenues for commodity-dependent nations. Capital inflows that would normally support these currencies dry up as investors seek exposure elsewhere. The result is a cascading decline in commodity currency valuations, which can accelerate once key technical support levels are breached.

GBP/USD: CAUGHT BETWEEN GLOBAL AND DOMESTIC HEADWINDS

The British pound faces a particularly complex backdrop. Beyond the global risk-off pressures affecting all commodity-linked currencies, sterling must contend with UK-specific challenges. Political uncertainty and economic vulnerabilities at the domestic level compound the international pressures, creating a multifaceted headwind for GBP/USD.

Recent trading activity tells a compelling story. Over a one-month period from late February to early March, GBP/USD declined from highs near 1.3484 to lows near 1.3354—a move of roughly 130 pips.[1][2] This correction reflects both the global deterioration in sentiment and heightened concerns about UK-specific risks. When international conditions weaken, currencies facing domestic challenges typically underperform peers, as investors become more selective about where they deploy capital.

The technical picture reinforces this narrative. The convergence of lower highs and lower lows in GBP/USD creates a downtrend structure that traders view as vulnerable. Analysts have specifically highlighted the 1.3200-1.3400 zone as support, suggesting that without a significant shift in sentiment, further weakness could test these levels.

Technical Support Levels And Market Implications

For traders monitoring GBP/USD, understanding the current technical structure is essential. The pair has retreated from February's 1.3670+ highs, and the recent lows near 1.3354 represent a test of intermediate support. The identified support zone at 1.3200-1.3400 provides a framework for positioning, with breaks below this range potentially triggering additional selling.

These technical levels matter because they represent price areas where historical supply and demand have been meaningful. Support levels often attract buyers, but in a sustained downtrend driven by fundamental deterioration, support can break. The interplay between technical levels and fundamental drivers—oil prices, geopolitical risk, UK domestic concerns—will determine whether GBP/USD stabilizes or breaks toward lower targets.

Takeaways For Market Participants

The current environment rewards careful risk management and an understanding of the connections between commodities, geopolitics, and currency valuations. Traders should monitor three key factors: the trajectory of oil prices, changes in global risk sentiment, and UK-specific economic and political developments. A reversal in any of these could alter the pressure on GBP and other commodity currencies.

For those with exposure to sterling or commodity FX, now is a critical time to reassess positioning. The technical backdrop suggests vulnerability, while the fundamental backdrop—rising input costs, weaker demand expectations, and UK domestic uncertainty—remains challenging. Until sentiment shifts materially, commodity currencies and GBP will likely remain under pressure.