The US Dollar Index sliding below the key 100 threshold marks a sharp reversal in the greenback’s narrative, and markets are treating it as more than just a technical break. A renewed flare-up in US–China trade tensions, with China announcing tariffs on selected US imports as high as 125%, has jolted risk sentiment, driven broad USD selling, and forced traders to rethink both Federal Reserve policy and global growth trajectories. The result is a fast, disorderly repricing across major currencies and emerging markets, with implications that go well beyond FX charts.

What A Break Below 100 Really Signals

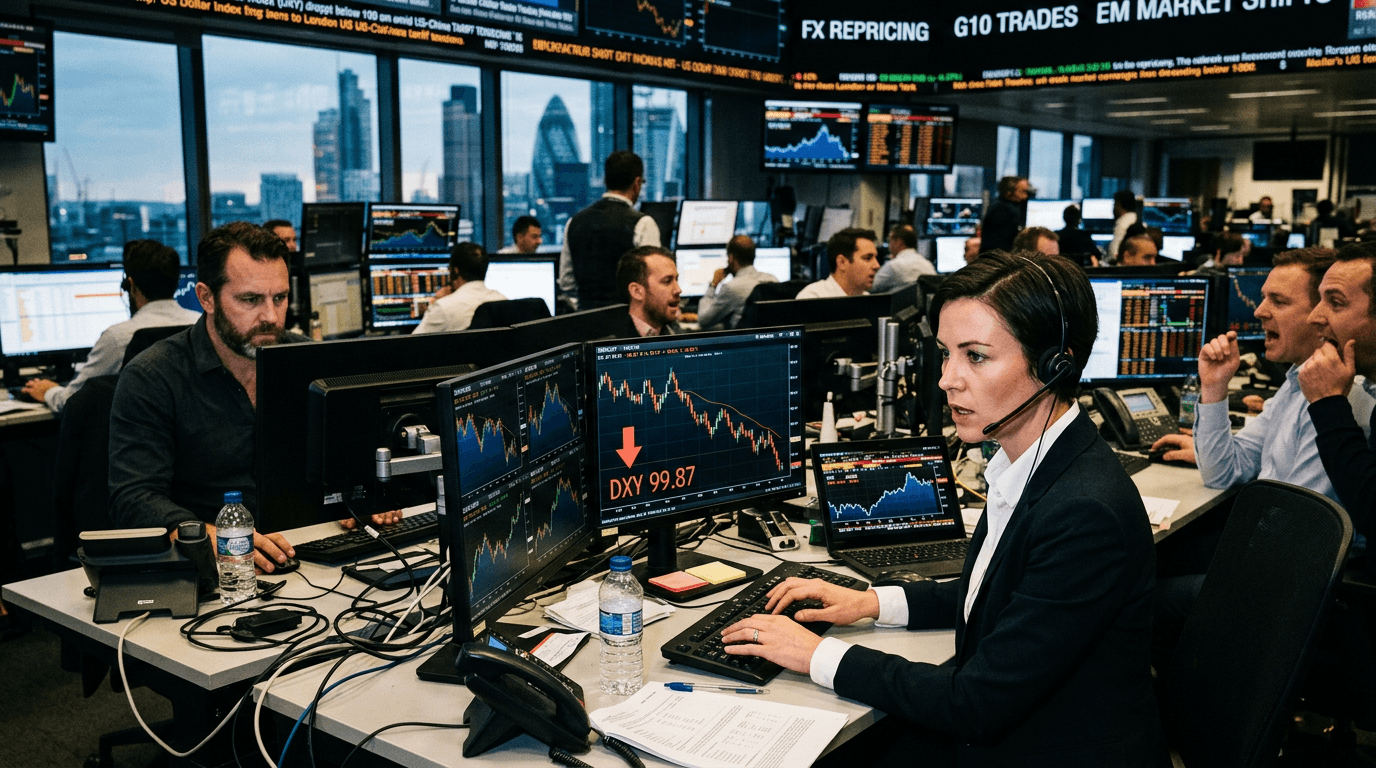

The U.S. Dollar Index (DXY) measures the value of the dollar against a basket of major currencies, dominated by the euro, Japanese yen, British pound, Canadian dollar, Swedish krona, and Swiss franc.[4][7] When the index rises, the dollar is strengthening versus this basket; when it falls, the dollar is weakening.[4] Levels around 100 have historically acted as a psychological pivot between “strong-dollar” and “neutral-to-weak-dollar” regimes, especially over the past decade.[3]

Breaking below 100 is thus not just a chart event; it often signifies a shift in the macro backdrop. A sustained move lower typically reflects changing expectations around US interest rates, growth relative to the rest of the world, and demand for safe-haven assets.[4][7] When investors move out of the dollar, they are implicitly expressing views on where capital will earn better risk-adjusted returns—whether in other developed markets, commodities, or emerging economies.

For traders, the key takeaway is that big index breaks usually coincide with regime change. That means strategies built for a strong-dollar environment—like shorting commodity currencies or favoring dollar-denominated assets—may need to be re-evaluated, stress-tested, or even rotated out entirely.

Tariff Fears, Fed Expectations, And Risk Sentiment

Tariff shocks are uniquely complex for FX markets because they hit multiple channels at once: trade volumes, inflation, and growth. Higher tariffs on US exports to China and vice versa can dampen global trade, weigh on corporate margins, and slow investment. At the same time, they can push up prices on imported goods, adding an inflationary layer to an already uncertain backdrop.

Initially, traders often respond by reducing risk and cutting leveraged USD positions, especially if the dollar has run up strongly in prior weeks. As risk aversion builds, markets re-examine the Federal Reserve’s path. If tariffs are seen as more damaging to growth than inflationary, the market may start pricing in a lower terminal rate or a faster pivot toward easing, pulling US yields down and undermining the dollar’s rate advantage.

The latest tariff headlines have triggered exactly this type of reassessment. FX and rates markets are now simultaneously discounting weaker US growth, a less aggressive Fed, and more volatility in global trade flows. That combination has historically been negative for the dollar and supportive for currencies tied to regions expected to benefit from trade diversion or stronger relative growth.

The practical takeaway: FX traders should think beyond a binary “tariffs = risk-off = stronger USD” narrative. The interaction between growth fears and rate expectations can turn the dollar down even in a risk-off environment. Watching both Treasury yields and inflation expectations alongside DXY becomes critical.

Major Fx Repricing Across G10 And Em

When the Dollar Index cracks a major level, repricing tends to be broad-based rather than limited to one or two pairs. In the G10 space, EUR/USD and GBP/USD often see outsized moves, as their heavy weightings in the index amplify shifts in USD sentiment.[4][7] A break below 100 typically coincides with these pairs pushing toward or through key resistance levels, as short-dollar flows seek liquid alternatives.

Safe-haven currencies like the Japanese yen and Swiss franc can behave more subtly. In a tariff-driven risk-off episode, they may strengthen on risk aversion, but if the dollar itself is being sold as a funding currency, USD/JPY and USD/CHF can move lower even as risk assets wobble. That interplay creates both opportunity and complexity for directional trades.

Emerging markets often welcome a weaker dollar, as it can reduce external financing pressure and support local assets.[9] However, the effect is uneven. Countries heavily reliant on exports to the US or China may still suffer under tariff uncertainty, while commodity exporters can benefit if a softer dollar supports raw material prices. Carry trades—borrowing in low-yield currencies to invest in higher-yielding EM FX—can look more attractive when US yields and the dollar decline, but the accompanying volatility means position sizing and risk controls are critical.

Key takeaway for traders: treat this as a cross-market regime shift, not just a DXY headline. Scenario analysis across G10 and EM, combined with a clear understanding of each currency’s exposure to trade and rates, becomes essential in navigating the repricing.

Implications For Traders And The Value Of Simulated Strategies

A rapid move below 100 in the Dollar Index tends to expose the strengths—and weaknesses—of trading plans. Strategies that performed well in a steady strong-dollar regime may struggle when volatility spikes and correlations change. For example, dollar-centric trend-following systems can be whipsawed by sudden reversals, while carry strategies may encounter sharp mark-to-market swings.

This is precisely the kind of environment where simulated finance (SimFi) platforms become powerful learning tools. In a risk-free environment, traders can:

- Test how their strategies behave when DXY breaks major levels and volatility jumps.

- Explore hedging approaches, such as balancing USD exposure with baskets of G10 and EM currencies.

- Experiment with cross-asset signals, using moves in rates, equities, and commodities to refine FX entries and exits.

By running structured simulations around scenarios like “DXY below 100 after tariff shock,” traders can build playbooks that are ready for real-world market stress, without the cost of live mistakes.

The takeaway: use episodes of major FX repricing as templates for building and refining robust strategies. Whether on live markets or a simulation platform, the goal is to understand how your approach behaves under regime change—not just under normal conditions.

Key Levels And Scenarios To Watch

Historical price action suggests that once the Dollar Index breaks a major psychological level, nearby support and resistance zones become focal points for market positioning.[1][3] Recent analyses have highlighted areas in the mid-90s to high-90s as important support bands, with former resistance around 100 now potentially acting as a ceiling if the bounce is limited.[1]

Traders should map out three broad scenarios

- Consolidation: DXY stabilizes in a range just below 100 as markets digest tariff news and wait for clearer signals from economic data and the Fed.

- Extension lower: Growth fears intensify, yields fall further, and the dollar slides toward prior multi-year lows, intensifying the shift into non-USD assets.

- Snapback: Tariff rhetoric cools or policy clarity improves, leading to a relief rally in the dollar and a partial unwind of recent FX moves.

Each scenario has distinct implications for G10 and EM currencies, as well as for risk assets. Aligning trade ideas with a clear view of which path is unfolding—and being ready to switch when the data changes—can provide a crucial edge.

Final takeaway: the break below 100 is a signal that the dollar regime is in flux. The coming sessions will be about whether this move evolves into a durable trend or proves to be a sharp, sentiment-driven shakeout. Either way, it is a real-time stress test for FX strategies, risk management frameworks, and the ability to adapt to fast-moving macro narratives.