The dollar’s latest surge offers a textbook example of how macro data, bond markets, and expectations for central bank policy interact to reshape FX and rate futures in real time. Strong U.S. economic reports have pushed the dollar index to recent highs while nudging Treasury yields upward, forcing traders to reassess how many cuts – or even whether a hike – the Federal Reserve might deliver this year.[5][8][11] For active and simulated traders alike, this environment is rich with lessons on how to read and trade cross‑asset repricing.

MACRO DATA: WHY “BETTER-THAN-EXPECTED” MATTERS

Recent U.S. releases have painted a picture of an economy that is stronger and more resilient than markets had priced in just a few weeks ago.[5][8][11] Jobless claims have remained low and even came in below forecasts, reinforcing the idea of a still‑tight labor market.[5][8] Job cuts have dropped to their lowest level in many months, suggesting employers are in no rush to shed workers despite previous fears of a slowdown.[5]

On the inflation side, producer price data and wholesale inflation prints have surprised to the upside.[7][8] That combination – robust employment and stickier inflation – is precisely the kind of signal that tends to make central banks more cautious about easing, and in some cases more open to further tightening.[2][8][11] Strong readings in service‑sector activity (such as the ISM services index) and factory orders have only added to the story of solid demand and momentum in the real economy.[6][11]

For the bond market, these data points translate into higher yields, especially at the front end and in the benchmark 10‑year note. In one recent move, stronger inflation and jobs data nudged the U.S. 10‑year yield up from around 2.48% to above 2.50%, helping to lift the dollar as rate‑sensitive pairs such as USD/JPY reacted.[7] Higher yields reflect investors demanding more compensation to hold U.S. debt in a world where the Fed may have to stay restrictive for longer – or even raise rates again if inflation and growth remain firm.

Key takeaway: when economic data exceed expectations on both growth and inflation, the default market response is to price in fewer rate cuts (or more hikes), push yields higher, and support the dollar.

Fx Reaction: Eur, Gbp, Jpy Under Dollar Pressure

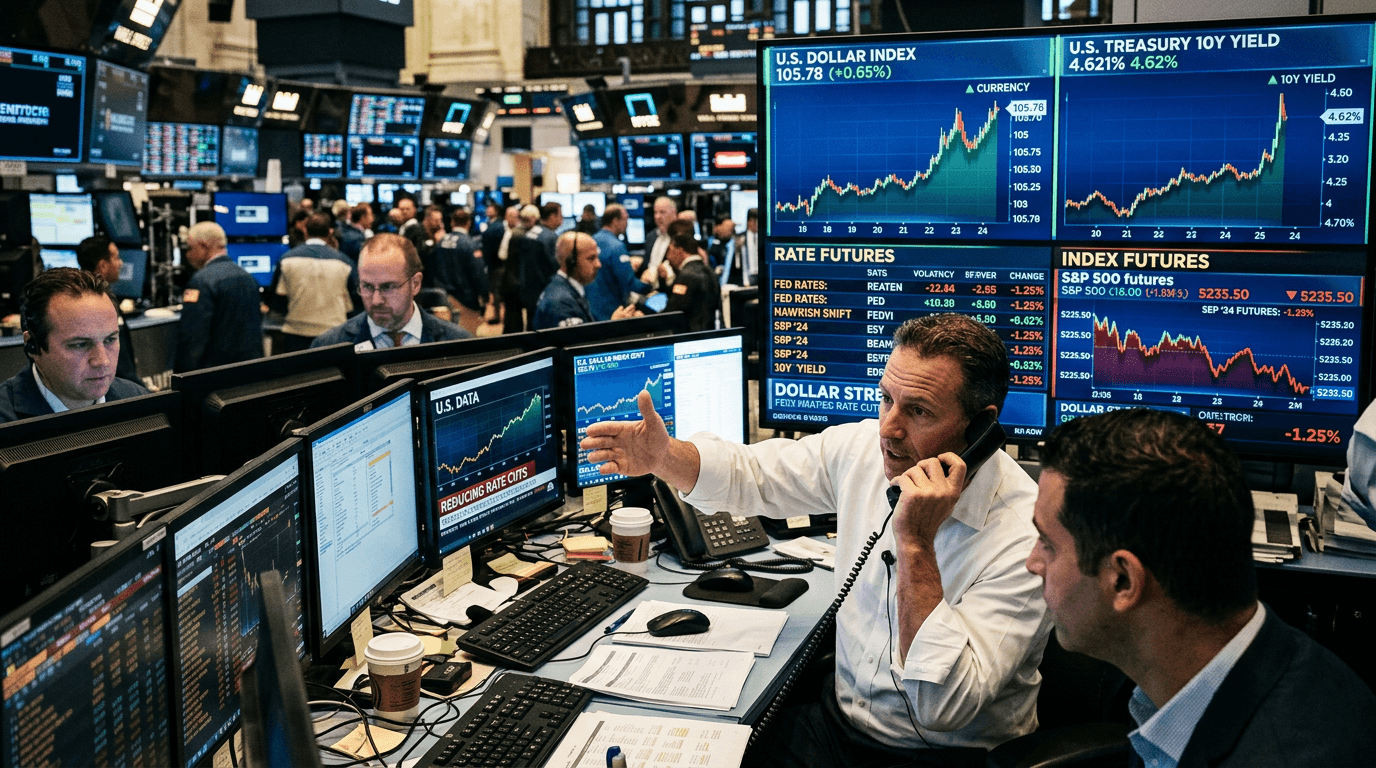

The dollar index – which measures the greenback against a basket of major currencies – has climbed to multi‑week or even one‑month highs on the back of these releases.[5][10] A stronger dollar typically shows up as:

- Lower EUR/USD and GBP/USD, because the U.S. now offers relatively higher yields and better growth prospects than the eurozone or the UK.

- Higher USD/JPY, as the yen is anchored by near‑zero rates and a Bank of Japan that remains far more dovish than the Fed.[7][10]

Recent sessions have illustrated this dynamic clearly. The dollar has risen against the euro and yen as traders cut back on the number of Fed cuts they expect this year.[8][10] Against the yen specifically, the dollar has climbed to levels not seen in months, reflecting widening yield differentials and the appeal of carry trades funded in JPY.[7][10]

For simulated and live FX traders, this is a classic rates‑driven dollar move. The fundamental story is not about idiosyncratic news in Europe or Japan; it is about U.S. macro outperformance and shifting Fed expectations. In such environments:

- Trend‑following strategies often favor long‑dollar positions against lower‑yielding currencies.

- Mean‑reversion traders watch for overextensions when the data surprise fades or when positioning becomes crowded.

- Options traders may look at skew and implied volatility in pairs like EUR/USD or USD/JPY to express views on upcoming data and central bank meetings.

Key takeaway: stronger U.S. data and rising Treasury yields typically pressure EUR, GBP, and JPY against the dollar, with USD/JPY often the most sensitive due to stark policy and yield differences.

Rate Futures: Repricing The Fed Path

Perhaps the clearest window into changing Fed expectations is the rate futures market. Fed funds futures and other short‑rate contracts embed the market’s implied path for policy rates over the coming meetings. As incoming data have surprised to the upside, traders have pared back expectations for near‑term cuts and reduced the total number of cuts priced for the year.[5][8]

Recent moves show that probabilities of a rate cut at upcoming Fed meetings have fallen, and the curve now implies fewer than three cuts over the year versus three to four not long ago.[8] In prior episodes of strong data, markets have even leaned toward the possibility of renewed tightening if inflation reaccelerates, underscoring how quickly the narrative can flip from “imminent easing” to “extended restriction.”[2][11]

For rate futures traders, this repricing opens a range of strategies:

- Taking views on whether the market has over‑ or under‑reacted to recent data.

- Spreads between different meeting months to express relative views on timing.

- Using Treasury futures and swaps in combination with Fed funds contracts to build more nuanced curve trades.

Simulated traders can practice translating data surprises into probability shifts, tracking tools such as Fed‑watching apps and comparing those implied odds with their own macro assessment.[4][5][8]

Key takeaway: strong data reduce the odds of near‑term cuts and can even revive hike probabilities, making short‑rate futures a central arena for expressing views on the Fed.

Equity Index Futures: Growth Versus Yield Headwinds

Equity index futures are also reacting to the same macro drivers, though the impact can be more nuanced. On one hand, better growth data support corporate earnings prospects and reduce immediate recession fears, which can be positive for indices.[5][11] On the other hand, higher yields raise discount rates, pressure high‑duration growth stocks, and tighten financial conditions, which can weigh on valuations.

Historically, strong “growth‑and‑inflation” prints often lead to sector rotation rather than a uniform move in indices. Rate‑sensitive sectors such as tech or real estate may underperform, while financials and cyclicals benefit from higher yields and better activity. Index futures traders watch not only the headline move but also the internal composition and correlation with bonds and FX.

In a simulated environment, this is an ideal scenario for practicing cross‑asset thinking: how a surprise in PPI or jobs can simultaneously move the dollar, the yield curve, and index futures – and where those moves may diverge if markets begin to worry more about inflation than growth.

Key takeaway: stronger data and higher yields create a tension in equity index futures between better earnings prospects and tighter financial conditions, encouraging more selective, sector‑aware strategies.

Practical Lessons For Simulated And Active Traders

The current dollar rally, powered by strong data and rising yields, offers several practical lessons:

First, macro surprises matter more than absolute levels. Markets care about data relative to expectations. A “good” number that is already fully priced in may move markets less than a moderately strong number that significantly beats forecasts.[5][8][11]

Second, always link FX moves to rate expectations. When the dollar moves on macro news, the underlying driver is usually yield differentials and the changing path of policy. Watching Fed funds futures, short‑maturity Treasury yields, and central bank commentary helps contextualize every FX move.[2][5][8][11]

Third, think in scenarios around central bank meetings. Strong data ahead of key meetings often leads to pre‑positioning in FX and rate futures as traders try to anticipate potential shifts in guidance or dot plots.[2][4][8] SimFi environments are ideal for stress‑testing these scenarios without capital at risk.

Finally, integrate risk management into macro trading. Strong data can trigger sharp moves and volatility spikes, especially when positioning is one‑sided. Practice adjusting position size, using options, and setting clear invalidation levels when trading macro‑sensitive assets like the dollar index, USD/JPY, or short‑rate futures.

As the dollar climbs on robust U.S. data and higher Treasury yields, traders across FX, rates, and equities are reminded that macro still drives the big picture. Whether you trade live or in a simulated environment, understanding how data flow reshapes expectations for the Fed is essential to navigating the next leg of the dollar cycle.