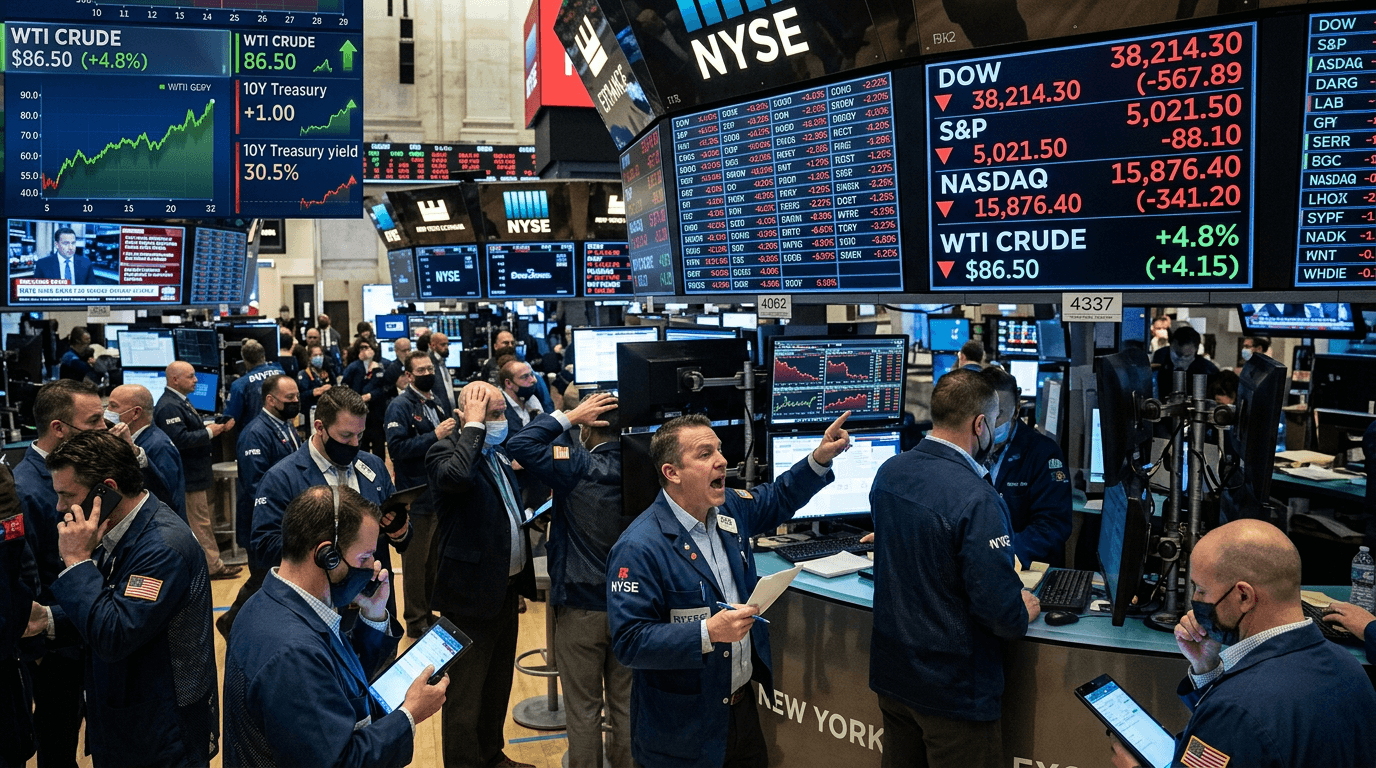

U.S. equity indices extended their slide as a sharp spike in energy prices and a repricing of interest-rate expectations rippled through risk assets. What started as a move in crude oil and the U.S. dollar quickly morphed into a broader de-risking across growth, small caps, and other rate-sensitive corners of the market, with volatility picking up as traders reassessed earnings, valuations, and the path of Federal Reserve policy.

WHAT’S DRIVING THE LATEST SELL-OFF?

Two forces are hitting the tape simultaneously: an energy shock and a shift in rate expectations.

Oil has pushed aggressively higher on renewed geopolitical tensions and supply concerns, with crude briefly trading near levels not seen in months. The speed of the move matters as much as the magnitude: rapid spikes tend to stress hedging programs, disrupt corporate planning, and force funds to rebalance risk in a hurry.

At the same time, markets are dialing back expectations for rapid Fed rate cuts. Sticky services inflation, firm wage data, and now higher energy prices complicate any narrative of quick disinflation. Fed funds futures have been repricing toward fewer and later cuts, pushing real yields and the U.S. dollar higher.

Equity futures responded in classic risk-off fashion. S&P 500, Nasdaq, and Dow contracts all traded lower through the session, with intraday rallies sold and volatility measures such as the VIX grinding higher. The message from price action: investors are adjusting to a world where both input costs and discount rates may stay higher for longer.

How Energy Shocks Filter Through Equities

Higher oil prices don’t just hit the pump; they work through multiple channels that matter for equity valuations.

First, they squeeze profit margins. Energy is a direct cost for transportation, manufacturing, airlines, logistics, and many industrials. Companies with low pricing power find it hard to pass higher fuel and input costs on to customers, which pressures earnings. Even firms that can raise prices may see demand soften over time.

Second, they act as a tax on consumers. When households spend more on fuel and heating, they often cut discretionary spending elsewhere. That’s one reason why travel, leisure, autos, and parts of retail can be vulnerable when crude spikes. Equity markets discount that future hit to revenue and profits.

Third, oil shocks complicate inflation and policy dynamics. A persistent move higher in energy can keep headline inflation elevated and bleed into core components over time, especially if transport and shipping costs rise. That can force central banks to stay restrictive longer than growth alone would justify.

Historically, it’s not the level of oil that causes trouble, it’s the velocity of the move. Gradual increases driven by strong demand can be absorbed. Sudden spikes driven by supply fears or geopolitics tend to trigger risk-off behavior, tighter financial conditions, and a change in sector leadership.

The major exception, of course, is energy equities. Producers, refiners, and some services firms can see earnings upgraded in a higher-price environment, particularly if their costs are fixed and hedging is well managed. That’s why index-level pain can coincide with strength in the energy sector.

Rates Repricing: Why Yields And The Dollar Matter

The second leg of the current sell-off is about the discount rate investors apply to future cash flows.

When traders price in fewer Fed cuts, the entire yield curve can shift higher. Even modest moves in real yields have outsize effects on so-called “long-duration” assets—those whose valuations rely heavily on profits far in the future. That includes many growth and technology names, as well as speculative small caps.

Higher yields also mean that the opportunity cost of owning equities rises. If investors can get more attractive returns in cash and high-quality bonds, the equity risk premium must adjust—often via lower price-to-earnings multiples. That’s the valuation channel of rates repricing.

A firmer U.S. dollar adds another layer. A stronger greenback tightens global financial conditions, weighs on commodity prices in non-dollar terms, and can pressure multinational earnings when overseas revenue is translated back into dollars. It also tends to be a headwind for emerging markets, limiting the global risk appetite that often supports U.S. equities at the margin.

For traders, monitoring the interplay between oil, yields, and the dollar is crucial. A market that was previously comfortable with a “soft-landing plus Fed easing” narrative is now questioning how benign the macro backdrop really is.

Sector And Style Winners And Losers

Not all parts of the equity market respond to energy shocks and rate repricing in the same way.

Growth and high-valuation tech: These names are particularly sensitive to higher real yields. When the discount rate rises, the present value of future earnings falls more for companies expected to deliver profits many years out. After a strong run driven by AI and digital themes, even small shifts in yields can trigger profit-taking.

Small caps and cyclicals: Smaller companies often face higher funding costs and have less pricing power, making them vulnerable to both higher rates and higher input costs. Cyclical sectors tied to discretionary demand may see double pressure from squeezed consumers and tighter financial conditions.

Energy and commodities: Energy producers typically benefit from sustained higher prices, though the path is rarely smooth. Services and equipment providers can gain if higher prices translate into increased investment and drilling activity. Conversely, energy-intensive sectors—like airlines, chemicals, and some industrials—can come under pressure.

Defensive sectors: Utilities, staples, and health care sometimes outperform in risk-off episodes. But when the driver is higher yields, defensives that trade like bond proxies can also suffer, as their dividends become less compelling versus safer fixed-income alternatives.

Style factors: Quality balance sheets, strong free cash flow, and low leverage tend to be rewarded when markets are worried about both costs and rates. Low-quality, highly leveraged, and speculative names often underperform.

How Traders Can Navigate This Regime

For active traders and investors, this environment rewards preparation and discipline more than bold predictions.

Clarify your time horizon. Short-term traders may focus on intraday responses to data releases, Fed commentary, and energy headlines. Longer-term participants should think in terms of regime shifts: is this a temporary spike or the beginning of a structurally tighter energy and rates backdrop?

Look beyond spot oil. The shape of the futures curve—backwardation versus contango—can reveal whether markets see the shock as short-lived or persistent. A persistently tight curve suggests deeper supply concerns and a more durable impact on inflation and equities.

Track inflation expectations. Breakeven inflation rates derived from inflation-linked bonds can signal whether markets see energy moves feeding into broader inflation or being absorbed. A sharp rise in breakevens alongside crude strength reinforces the “higher-for-longer” rate narrative.

Revisit correlations and hedges. In stress regimes, relationships between assets can change. Bonds may not always rally when equities sell off, and traditional hedges might underperform. Testing strategies against past oil shock episodes can help reveal hidden vulnerabilities.

Adjust risk, not just direction. Volatility cuts both ways. Wider intraday ranges mean that using the same position sizes, leverage, or stop distances as in calmer periods can lead to outsized drawdowns. Reducing size, focusing on higher-conviction setups, and considering options for defined-risk exposure can help protect capital.

Think in relatives, not absolutes. Instead of only betting on index direction, traders can explore relative-value trades: energy versus the broader market, value versus growth, or quality versus high leverage. These can express macro views while reducing exposure to overall market swings.

Conclusion

The latest slide in U.S. equity indices is less about a single headline and more about a repricing of an entire macro narrative. An energy shock and a shift in rate expectations are forcing investors to reassess margins, valuations, and the speed at which monetary policy can normalize.

For traders, the challenge is to adapt faster than the market consensus. That means understanding how oil, yields, and the dollar interact, recognizing which sectors and styles are most exposed, and tightening risk management as volatility rises. While the adjustment can be painful for complacent positioning, it also creates opportunities for those with a clear framework and the discipline to stick to it when conditions change.