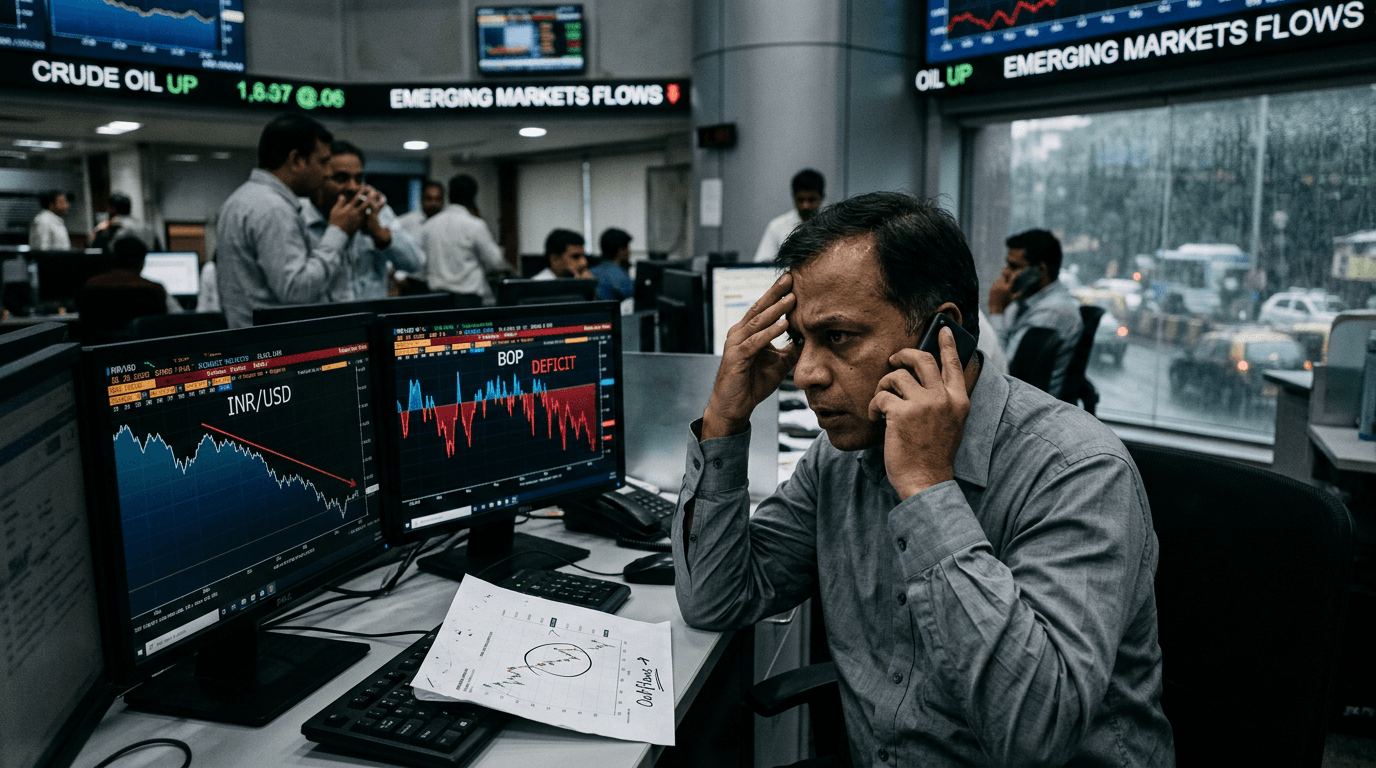

India’s latest balance of payments (BoP) data underline how quickly sentiment can swing in emerging markets: after years of comfortable surpluses, the country is now running a BoP deficit for the second straight month, driven largely by foreign portfolio outflows even as long‑term investment and services exports remain resilient.[1][2] That combination is putting renewed pressure on the rupee and forcing FX traders to reassess both the trajectory of emerging‑market flows and the Reserve Bank of India’s (RBI) policy playbook.[1][4][9]

What The Latest Numbers Show

Preliminary RBI data show India’s overall BoP recorded a deficit of about $4.4 billion in May, following a larger $6.6 billion deficit in April.[1] A year earlier, May had seen a BoP surplus of a similar magnitude, underscoring how sharply the external position has deteriorated.[1] For the first two months of the current fiscal year, the BoP shortfall has reached roughly $11 billion, compared with a surplus of $5 billion in the same period last year.[6]

Crucially, the picture on the current account is more nuanced than the headline deficit suggests. In May, India posted a current account deficit (CAD) of about $2 billion as a wider merchandise trade gap outweighed robust services exports and transfer receipts.[2] Yet over April–May as a whole, the country still managed a current account surplus of $2.8 billion, a turnaround from the deficit recorded in the same period a year earlier.[2] Similar patterns have appeared in recent quarters: strong services and remittance inflows have generated sizable current account surpluses even when the goods trade deficit has remained large.[10]

The message for traders is clear: the deterioration in the BoP is not being driven primarily by India’s ability to earn foreign exchange through exports of goods and services, but by what is happening on the capital side of the ledger.[1][2][6]

Portfolio Outflows: The New Pressure Point

Foreign portfolio investors (FPIs) have shifted from being a stabilising force to a source of volatility. In April, net FPI outflows were estimated at around $8.7 billion, large enough to push the overall BoP into deficit despite a sizeable current account surplus that month.[7] Over the 2025–26 fiscal year, RBI data show FPIs pulled out about $4.3 billion more than they invested, reversing the positive trend of persistent net inflows seen in the prior two years.[3]

These outflows are occurring against a backdrop of heightened global risk and region‑specific shocks. The Iran‑linked energy disruption has driven a sustained increase in oil prices, raising India’s import bill and darkening the outlook for external balances.[4] Since the conflict escalated, foreign investors have withdrawn more than $20 billion from Indian equities, with outflows this year already exceeding last year’s record.[4] Volatile portfolio flows have been explicitly flagged in official economic reviews as a key source of pressure on the rupee, even as foreign direct investment (FDI) inflows have remained near record highs—around $94.5 billion in FY26.[9]

From a macro perspective, this is a classic BoP story: structural dependence on imported oil and gold amplifies vulnerability to commodity shocks, and portfolio investors respond quickly to shifts in global rates, risk appetite, and geopolitical risk.[3][4][12] For traders, the important point is that even a “good” current account cannot fully insulate an emerging market when capital flows turn risk‑off.

Current Account Vs Capital Account: Why The Deficit Matters

A BoP deficit simply means that, over a given period, more foreign currency is leaving the country than coming in, across both the current account (trade in goods and services, income, transfers) and the capital/financial account (FDI, portfolio flows, loans, deposits).[5][12] When that deficit persists, it has to be financed—typically by drawing down foreign exchange reserves or incurring new external liabilities.

India’s recent experience shows how quickly the financing burden can grow. The RBI’s annual report indicates that in FY25–26 the overall BoP deficit widened to about $30.8 billion, and this gap was funded entirely by dipping into the central bank’s foreign exchange reserves.[3][5] While India’s reserve stock remains “comfortable” by conventional metrics,[9] relying solely on reserves to plug ongoing deficits is not a strategy that can be pursued indefinitely without market participants starting to question the sustainability of the external position.

Historically, episodes of widening current account deficits—often driven by surging import costs during commodity price spikes—have created macro pressure through weaker growth, higher inflation, and currency depreciation.[4][11][12] What makes the present episode notable is that the BoP deficit is being shaped as much by capital flows (especially portfolio outflows) as by the trade balance, which alters both the speed and the channels through which market stress can emerge.[1][4][7]

Implications For The Rupee And Rbi Policy

The rupee is already showing the strain. Since the onset of the Iran‑related conflict, the currency has depreciated by more than 5%, hitting record lows and ranking as the worst‑performing major Asian currency in 2026.[4] Official data and commentary highlight that FPI outflows, combined with a more expensive energy import bill, are key drivers of this weakness.[4][9]

In response, policymakers have turned to a crisis‑style toolkit. The RBI has been selling dollars from its reserves to smooth volatility and support the rupee, while the government has raised tariffs on precious metal imports to curb demand and conserve foreign exchange.[4] Public appeals to moderate FX‑intensive consumption and maintain external discipline echo measures seen in previous periods of BoP stress.[4][12]

For FX traders, these actions matter in two ways. First, active FX intervention can temper the pace of rupee depreciation in the short term, affecting carry and trend‑following strategies. Second, the scale and persistence of intervention offer clues about the RBI’s tolerance for currency weakness and its broader policy reaction function: heavy reserve use without accompanying rate or macroprudential adjustments may be read as a sign that policymakers want to avoid tightening domestic financial conditions too aggressively, at least for now.[4][9]

Practical Takeaways For Traders And Simulated Strategies

The current episode is a live case study in how BoP dynamics translate into market opportunities and risks.

For discretionary and systematic FX traders, three practical lessons stand out:

1. Watch the BoP, not just the current account. A country can show a respectable current account position while its overall BoP slides into deficit if capital flows turn sharply negative, as India’s April–May data illustrate.[1][2][6][7] Positioning solely off trade and services trends without tracking portfolio flows can miss the real driver of currency moves.

2. Treat FPI flow data as a high‑frequency sentiment gauge. The sheer scale of recent equity outflows—over $20 billion since the energy shock—has acted as a powerful headwind for the rupee and local assets.[4] In simulated environments, building strategies that respond to changes in net portfolio flows (for example, using them as a filter for EM FX carry or momentum trades) can sharpen risk management.

3. Incorporate policy and reserves into your risk framework. A BoP deficit of more than $30 billion funded entirely by reserves is a warning sign that external buffers are being used actively to manage stress.[3][5][9] For both real and simulated trading, monitoring reserve trends alongside BoP releases and policy statements helps anticipate when an intervention‑heavy regime might give way to more durable adjustments, such as rate hikes, capital flow measures, or targeted macroprudential steps.

For SimFi participants, India’s BoP story is an ideal scenario to practise navigating complex macro cross‑currents: strong structural positives (services exports, remittances, robust FDI) coexisting with cyclical pressures (commodity shocks, portfolio outflows, currency weakness).[2][9][10][12] Designing simulated portfolios that stress‑test rupee exposure, EM carry trades, and equity allocations under varying assumptions about BoP outcomes and RBI responses can build the discipline needed to trade real markets when data surprises and sentiment shift abruptly.