Indonesia’s central bank is putting banking-system liquidity under a sharper microscope, signaling that how cash flows through domestic banks is now a frontline issue for safeguarding financial stability and supporting growth.[1] This shift matters not only for Indonesian lenders, but also for traders watching the rupiah, local bond markets, and broader emerging‑market FX sentiment.[4] As global conditions remain fluid, Bank Indonesia’s focus on liquidity distribution is a key clue to its policy priorities and risk tolerance.[1]

Why Bank Indonesia Is Watching Liquidity More Closely

In its latest communication, Bank Indonesia (BI) emphasized that it is monitoring the distribution of liquidity across domestic banks, aiming to ensure that every lender has adequate cash buffers to support lending and maintain stability.[1] The emphasis on distribution is crucial: stability risks often arise not when aggregate liquidity is low, but when it is unevenly concentrated in parts of the system.[9] If smaller or weaker banks find themselves short of liquidity while larger institutions are flush, credit to the real economy can slow and confidence can erode.

Importantly, BI is stressing that overall banking liquidity remains ample, providing a reassuring backdrop to this closer scrutiny.[2] One key indicator, the INDONIA interbank overnight rate, has eased to around 6.17% from 6.62% a month earlier, a sign that money‑market liquidity is still comfortable and funding pressures are limited.[2] Rather than reacting to visible stress, BI appears to be leaning into a more proactive, macroprudential stance—using liquidity monitoring as an early‑warning and calibration tool.[9]

This approach is consistent with broader policy moves in recent years, where BI has blended interest‑rate tools with targeted liquidity measures and incentives.[9] From pandemic-era liquidity support to ongoing macroprudential liquidity policies, the central bank has increasingly treated banks’ funding conditions as a key lever for balancing growth and financial stability.[3] Closer monitoring of liquidity distribution simply pushes that lever further into the spotlight.

How Liquidity Monitoring Works In Practice

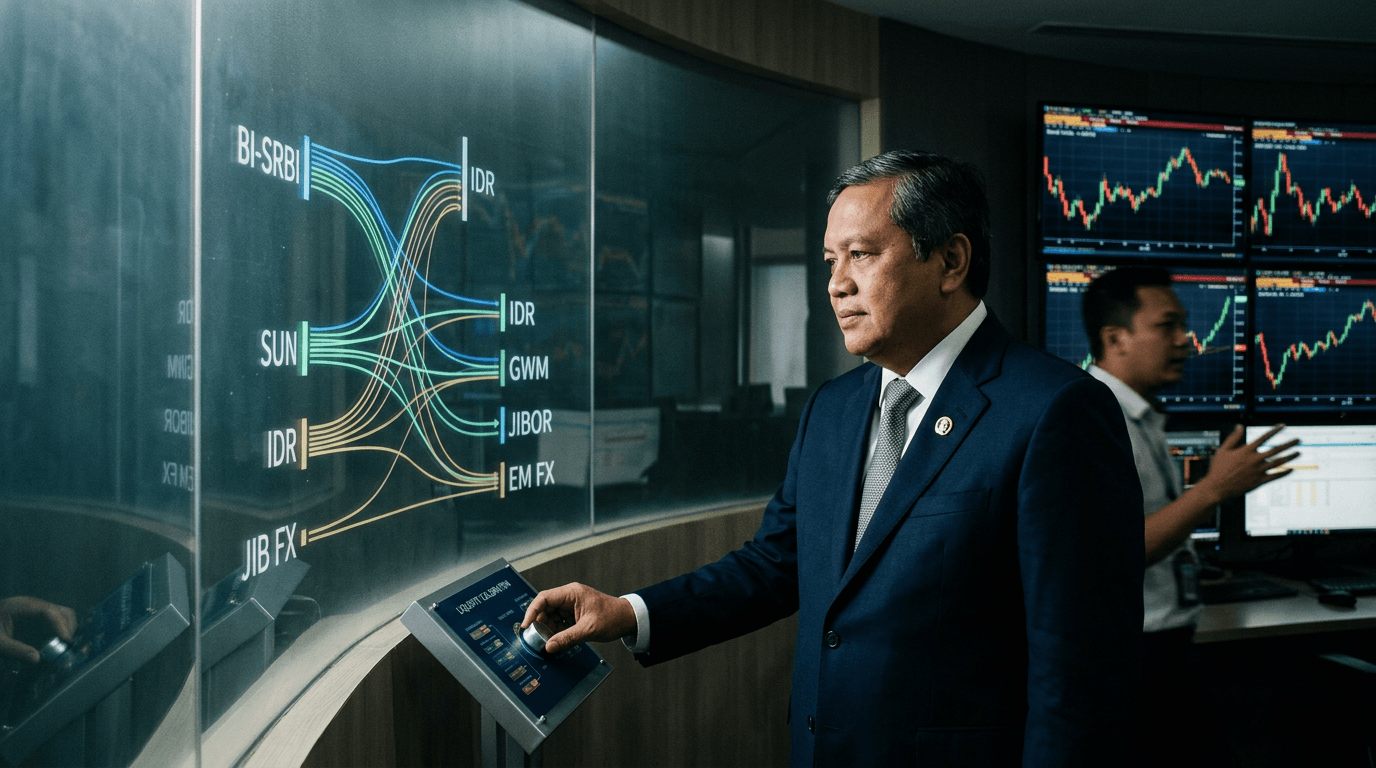

For traders, “monitoring liquidity distribution” can sound vague, but in practice it rests on concrete data and tools. BI and the financial regulator track a mix of indicators: interbank rates, loan‑to‑deposit ratios, liquidity coverage ratios (LCR), and banks’ foreign currency positions.[8] Indonesia has adopted Basel‑style liquidity coverage requirements and requires banks to monitor LCR by significant currencies, providing granular visibility into funding resilience in both rupiah and FX.[8]

At the system level, the central bank watches daily movements in money‑market rates and volumes, using indicators like INDONIA to gauge whether cash is flowing smoothly between banks.[2] A sustained rise in interbank rates or a fragmentation in trading could flag emerging stress. BI can respond with liquidity injections through open market operations, repos, or, where needed, targeted support measures.[9]

In recent years, BI has also adjusted structural parameters to give banks more flexibility in managing liquidity. It reduced the secondary reserve requirement from 5% to 4%, freeing up around 78 trillion rupiah in additional liquidity for banks.[6] At the same time, it lifted the cap on foreign funding that local banks can access, raising the limit to 35% of capital from 30%, to broaden funding options and support loan expansion.[6] On top of this, BI has deployed macroprudential liquidity incentives—Kebijakan Likuiditas Makroprudensial (KLM)—with hundreds of trillions of rupiah earmarked to encourage lending to strategic sectors.[10]

Taken together, these measures show that BI’s monitoring is backed by a toolkit that can quickly translate observations into action. The latest emphasis on distribution suggests that future moves, if needed, may be more targeted—channeling liquidity to specific banks or sectors rather than simply flooding the system.

Implications For The Rupiah, Bonds, And Money Markets

For FX and rates traders, liquidity policy is increasingly intertwined with currency strategy. By highlighting liquidity monitoring, BI is signaling that it wants to keep credit flowing without allowing pockets of stress to threaten the rupiah or local bond markets.[1] A well‑funded banking system tends to dampen the risk of sudden funding squeezes, which can otherwise trigger forced asset sales and currency volatility.

In the rupiah market, this stance may reduce tail‑risk perceptions even if it does not immediately change the interest‑rate trajectory. Investors can read BI’s communication as a commitment to pre‑emptive stabilization: should global conditions tighten or capital outflows pick up, the central bank is prepared to use its liquidity tools to cushion the impact on domestic funding and the currency.[4] That can support carry‑trade strategies where confidence in the policy framework is as important as the nominal yield.

Local bonds and money markets are also directly in the line of impact. Ample and well‑distributed liquidity tends to anchor short‑term rates near the policy corridor and limit spikes in repo or interbank costs.[2] Stable funding costs, in turn, help keep government bond yields from overshooting due to technical pressures. Conversely, if BI’s monitoring were to reveal strains and prompt visible intervention—such as large liquidity injections or special facilities—markets might reprice both risk and future policy moves.

Because Indonesia is a key component of emerging‑market benchmarks, its liquidity stance feeds into broader EM FX sentiment. A central bank that communicates actively about liquidity and shows a willingness to act can be seen as reducing systemic risk in the region, supporting risk‑on behavior when macro conditions allow.[4]

What Traders And Simfi Participants Should Watch

For market participants and SimFi traders, the practical question is: what to watch, and how to translate this into strategy?

First, pay attention to BI’s language around liquidity in its press briefings and statements. When the emphasis shifts from “ample” to “uneven” or “tightening,” that is a signal that policy action—through liquidity tools or, eventually, rates—may be on the table. Monitoring references to specific indicators like interbank rates or sectoral lending can provide early hints of where the central bank is focusing its concern.[1]

Second, track key market gauges. The INDONIA rate, term money‑market rates, and bid‑ask conditions in rupiah funding all offer real‑time feedback on whether liquidity distribution is smooth or fragmenting.[2] For bond traders, watching the spread between short‑dated government bonds and policy rates can reveal whether funding premiums are creeping in.

Third, integrate these signals into simulated trading strategies. On a SimFi platform, traders can model scenarios where a rise in interbank rates triggers BI liquidity injections, leading to lower short‑term yields and a modest firming of the rupiah. Conversely, a deterioration in liquidity indicators could be linked to increased volatility assumptions, wider credit spreads, and a more defensive EM FX stance. By treating liquidity metrics as dynamic inputs rather than background noise, simulated portfolios become more realistic and better aligned with how macro desks operate in practice.

Looking Ahead: Liquidity As A Core Policy Pillar

Indonesia’s decision to step up liquidity monitoring is not a sign of crisis; it is a sign of a more vigilant, data‑driven approach to financial stability.[1] With aggregate liquidity still described as loose and money‑market rates signaling comfortable conditions, BI is moving to ensure that the distribution of that liquidity does not become a blind spot.[2] That shift matters because episodes of stress often start at the margins—through isolated funding problems that, left unchecked, can scale into broader instability.

For traders, the takeaway is clear: liquidity conditions are now a central pillar of Indonesia’s policy mix, sitting alongside interest rates and FX management as a driver of market outcomes.[4] As global financial cycles evolve, BI’s monitoring and response framework will help shape the path of the rupiah, local yields, and Indonesia’s position within the wider EM complex. Building liquidity indicators into your analysis—whether in live trading or simulated strategies—will be essential for staying ahead of the narrative in this new phase of policy signaling.