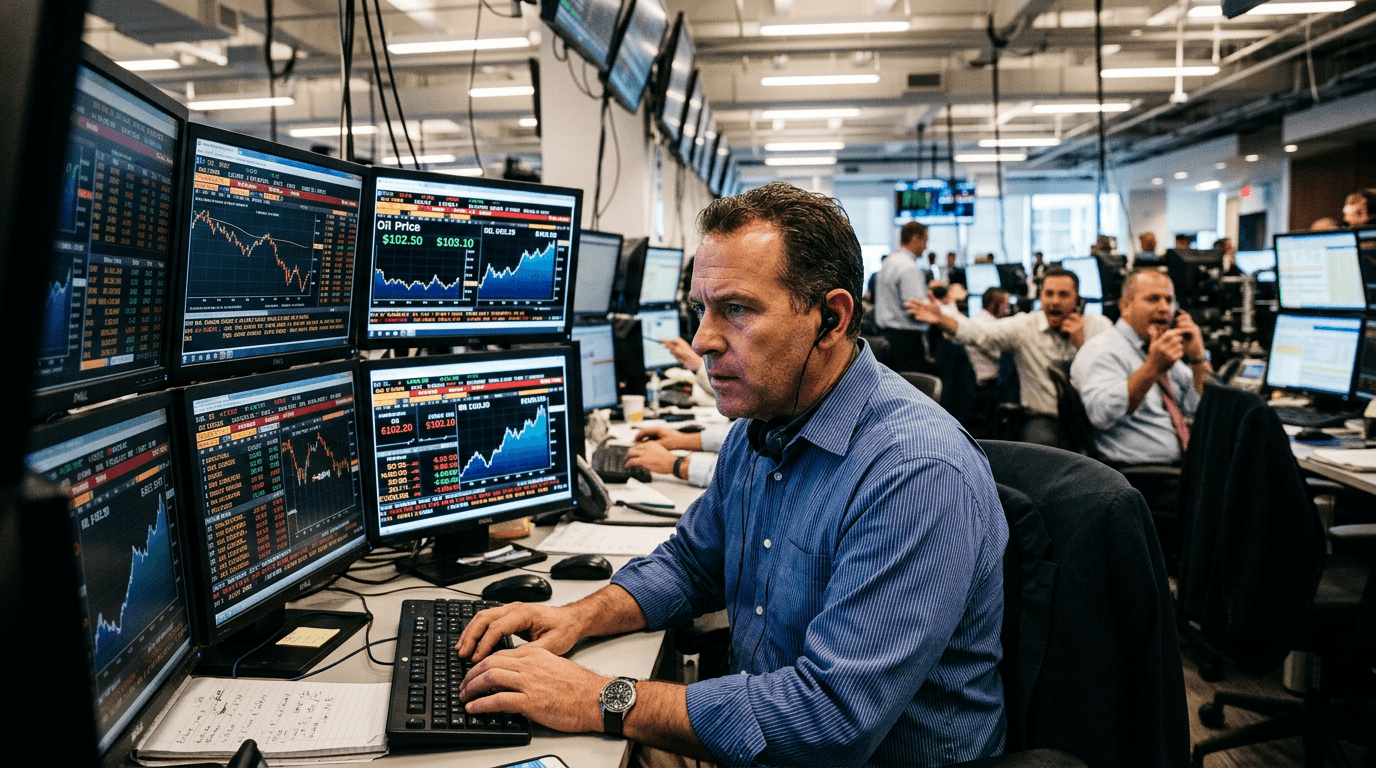

Oil prices have punched back above the psychological $100 mark, with WTI crude extending gains toward $102.50 and Brent trading even higher, as the Iran war and fresh drone attacks on Gulf energy facilities reignite fears of supply disruption. The move isn’t just about expensive gasoline; it’s reshaping currency markets, equity sectors, and inflation expectations, and it’s forcing traders to reassess how much geopolitical risk is really priced in.

WHAT’S DRIVING THE LATEST OIL SPIKE

The core driver is a rapid escalation of geopolitical risk layered onto an already tight market narrative.

Iran’s conflict with Israel and the United States has spilled over into critical energy infrastructure across the Middle East. Reports point to shutdowns and disruptions at oil and gas facilities in key exporters, including Saudi Arabia and the UAE, after renewed drone attacks. In parallel, previous strikes and the threat of further retaliation have increased the vulnerability of production sites, refineries, and export terminals.

At the same time, the Strait of Hormuz — the narrow chokepoint through which roughly a fifth of seaborne crude flows — has become the focal point for traders. Shipping delays, damaged tankers, and heightened naval presence in the area raise the tail risk of a partial or full disruption to traffic, even if just for a few weeks. Banks have flagged that a multi-week squeeze through Hormuz could force Gulf producers to shut in output, potentially pushing Brent well above $100 and into triple digits for an extended period.

On top of that, Iran’s Revolutionary Guard has issued warnings that oil prices could surge toward $200 per barrel if attacks on Iran continue, underscoring the market’s worst-case scenario. Even if that level isn’t the base case, such rhetoric reinforces the risk premium traders are willing to pay.

Importantly, this spike comes despite relatively comfortable global supply projections. The International Energy Agency and several analysts still expect additional output from the US, Guyana, and some OPEC+ members to outpace demand this year. That means the current move is less about a structural shortage and more about immediate logistical and geopolitical risk being priced into futures.

How The Shock Is Rippling Through Global Markets

Oil at $100+ is not an isolated story. It is feeding into multiple asset classes in ways that are typical for geopolitical supply shocks — but with some nuances.

Currency markets are reacting quickly. Oil-importing countries, particularly in Asia, are feeling the squeeze as higher energy bills widen trade deficits and strain external balances. The Indian rupee and several other Asian currencies have come under renewed pressure as importers must buy more dollars to pay for expensive crude. Conversely, some energy exporter currencies and related credit markets are seeing support, reflecting improved terms of trade.

Equity markets are split. Energy stocks and service providers are broadly higher, as investors price in stronger cash flows and improved margins for producers with stable output. By contrast, energy-intensive sectors such as airlines, logistics, and some manufacturing names are under pressure, with concerns about margin compression if companies can’t fully pass on higher fuel costs.

Inflation expectations are ticking higher, especially in economies that had just begun to see relief from previous energy spikes. Higher crude filters through to gasoline, diesel, jet fuel, and eventually into transportation and goods prices. This complicates the narrative for central banks that were inching toward easier policy, raising questions about how much room they have to cut rates if energy-driven inflation persists.

The overall risk tone has shifted to “risk-off.” Global equity indices are seeing heavier selling on down days, safe-haven assets such as the dollar and short-dated government bonds are seeing inflows, and implied volatility in both equity and oil options has risen. Markets are signaling that while this may not be a systemic crisis yet, it is a serious geopolitical shock with the potential to escalate.

What This Means For Traders

For traders, the current environment is rich with opportunity but also fraught with trap doors. Volatility is elevated across commodities, FX, and indices, which means both potential for outsized gains and the risk of sharp reversals.

In energy markets, directional traders may be tempted to chase the move higher. But geopolitical spikes are notoriously prone to “buy the rumor, sell the fact” behavior once immediate fears subside or new information emerges. Managing position size and avoiding over-leverage is critical. Intraday ranges in crude can expand dramatically, and overnight gaps around headlines can trigger slippage and stop-outs.

FX traders should watch oil-linked relationships carefully. Traditionally, currencies of oil importers weaken when crude spikes, while exporters strengthen, but the strength of these correlations can vary. It’s useful to combine macro logic with actual price behavior: Is the rupee, for example, underperforming its regional peers, or has the move already been largely priced in?

Index and equity traders can use sector rotation as a framework. Rising oil tends to benefit energy producers and sometimes value-oriented, cash-generating names, while hurting energy-intensive sectors and some consumer stocks if higher fuel prices erode disposable incomes. Exchange-traded funds (ETFs) tied to energy and airlines, for instance, provide clean ways to express these themes.

For those practicing in simulated environments, this is an ideal case study in event-driven trading. Traders can:

- Test how their strategies handle sudden volatility spikes and gaps.

- Practice scenario planning: How do their positions perform if oil jumps another $10? What if it drops back below $90?

- Refine risk management rules around news releases and geopolitical headlines.

Scenarios To Watch Next

Markets are forward-looking. Pricing today reflects not just current disruptions but expectations about what happens next. Several paths stand out:

1. De-escalation and normalization Diplomatic efforts could reduce hostilities, drone attacks may subside, and shipping lanes might normalize. In this case, the risk premium embedded in oil prices could deflate, pushing WTI and Brent back toward levels more consistent with underlying supply-demand balances. That doesn’t necessarily mean a collapse in prices, but a grinding move lower and volatility compression.

2. Prolonged but contained disruption Drone and missile attacks might continue sporadically, keeping key facilities and shipping routes at risk without a complete shutdown. Oil could remain elevated in a broad range — for example, Brent trading in the $80–$100+ zone — with frequent headline-driven spikes and pullbacks. This scenario favors nimble, tactical trading over set-and-forget positioning.

3. Severe escalation and chokepoint crisis A more extreme scenario involves significant damage to infrastructure or a serious disruption through the Strait of Hormuz. That could lead to genuine supply shortfalls, drawing down inventories and potentially sending prices sharply higher, with some houses warning of upside scenarios well above current levels. This would likely deliver a stronger stagflationary shock to the global economy, with deeper equity drawdowns and more stress in emerging markets.

In each scenario, traders should monitor not only price but also volatility, term structure (contango vs backwardation), and positioning data to gauge whether the market is crowded in one direction.

Key Takeaways

- The move above $102 in WTI is driven primarily by a geopolitical risk premium tied to the Iran war, drone attacks on Gulf energy assets, and concerns about the Strait of Hormuz, not an immediate global supply collapse.

- The shock is rippling through FX, equities, and rates: oil-importing currencies are under pressure, energy equities are outperforming, and inflation expectations are nudging higher, contributing to a broader risk-off tone.

- For traders, elevated volatility creates opportunity but demands disciplined risk management, especially around news headlines and overnight gaps.

- The outlook hinges on the trajectory of the conflict and the security of key shipping routes; de-escalation could see the risk premium fade, while escalation could transform a geopolitical shock into a more systemic macro problem.

In the meantime, treating this episode as a live stress test — for portfolios, strategies, and risk frameworks — is one of the most constructive ways to navigate an oil market once again defined by geopolitics as much as by barrels.