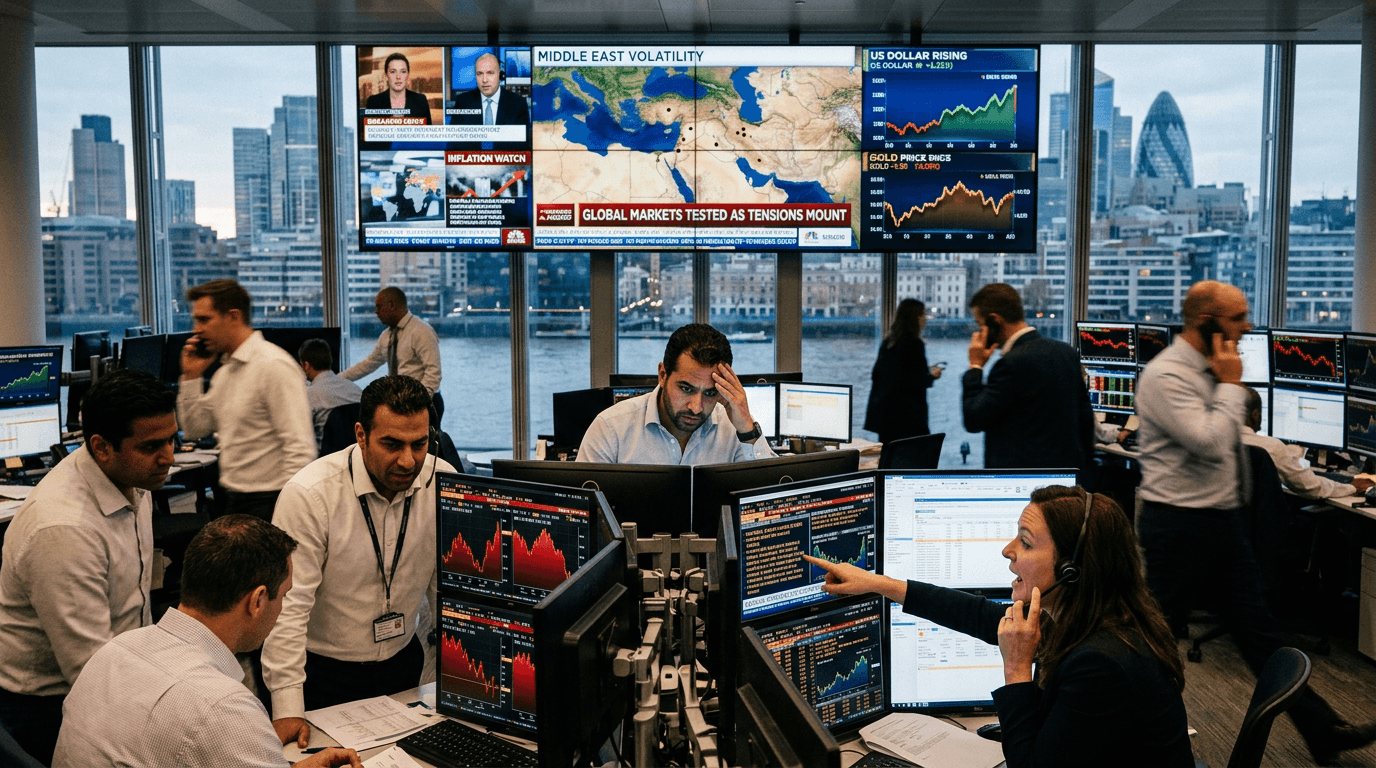

Fears of a wider Iran war and persistent conflict across the Middle East are rippling through global markets, reigniting classic worries about oil, inflation, and the path of interest rates. Crude futures have rebounded after a near‑10% spike as traders reassess war‑related disruptions to energy flows and shipping routes, and that volatility is feeding directly into expectations for a stronger dollar and renewed demand for safe‑haven assets.

Global Oil Market On Edge

The Middle East remains the beating heart of global energy supply, so any sustained conflict involving Iran has outsized implications for oil markets. The region’s war has already created what major energy authorities describe as one of the largest supply disruptions in the history of oil markets, as ongoing hostilities impede tankers from moving millions of barrels of crude each day through key routes such as the Strait of Hormuz.[3]

Tehran’s targeting of vessels and energy infrastructure, combined with mine risks in narrow shipping lanes, has forced major producers to halt or reroute shipments.[10] In some scenarios, flows through the Strait have come close to a standstill, sidelining roughly 20% of global crude and natural gas supply and pushing regional exporters like Saudi Arabia, the UAE, Iraq, and Kuwait to suspend tens of millions of barrels of shipments.[10] Authorities estimate Middle Eastern output could fall by at least 10 million barrels a day, translating into an 8 million barrel per day drop in global production even after accounting for higher output elsewhere.[3]

To cushion the shock, the International Energy Agency coordinated the largest emergency release of government reserves in its history, with member countries agreeing to inject around 400 million barrels of crude into the market.[3] These measures have helped prevent prices from spiraling out of control, but they do not fully offset the risks of prolonged disruption—and traders know that any new escalation around critical infrastructure or shipping lanes could trigger another leg higher in oil.

Inflation Fears And Central Banks

Higher oil prices do not just pinch motorists; they ripple through almost every corner of the economy via increased transportation, manufacturing, and input costs. Analysts estimate that if crude stabilizes in the $90–$100 range and stays there, inflation in developed economies could run about 0.8 percentage points hotter than previously forecast.[1] That would be a meaningful setback for central banks that have spent the last several years trying to bring price growth back down toward targets.

Rising energy costs are already expected to feed into both consumer and producer prices, particularly in countries heavily dependent on Middle Eastern imports.[6] A prolonged period of elevated oil prices tends to raise the cost of everyday goods as shipping and production expenses jump, creating broad inflationary pressure.[12] Economists warn that this mix of higher prices and weakening growth prospects—sometimes labeled “stagflation risk”—is a real possibility when an energy shock coincides with an already fragile global recovery.[10][13]

Central banks now face a difficult dilemma. On one hand, an oil‑driven inflation shock argues for keeping policy tight or even hiking again to prevent expectations from becoming unanchored.[1][6] On the other, aggressively tightening into an energy crisis could deepen the slowdown in real activity and financial conditions. In recent episodes, institutions like the Federal Reserve, the European Central Bank, and the Bank of England have opted to hold rates steady while they assess how the energy shock is reshaping the inflation and growth outlook.[4] Markets are therefore highly sensitive to incoming data and central‑bank communication, knowing that a shift in tone toward renewed tightening would be a powerful driver for both bonds and currencies.

Dollar Strength And Safe-haven Flows

Against this backdrop, the U.S. dollar typically finds support from two channels: expectations that the Federal Reserve will remain comparatively hawkish, and global risk aversion. When investors price in the possibility of higher U.S. rates relative to other major economies, U.S. yields tend to rise, drawing capital into dollar‑denominated assets. At the same time, geopolitical shocks that threaten growth often lead global investors to seek liquidity and perceived safety in the world’s reserve currency.

Geopolitical stress also tends to revive demand for classic safe havens such as gold and, to a lesser extent, silver. Historically, periods of war in the Middle East have coincided with elevated precious‑metal prices as investors hedge against both inflation and financial‑system risk—this pattern reflects long‑standing market behavior rather than a specific data point from this week. Overlapping flows into the dollar and havens can create an unusual environment where both “risk‑off” assets and a strong U.S. currency outperform simultaneously, while higher‑beta currencies and equities struggle.

For traders, this means oil, FX, and metals are all being pulled by the same narrative: conflict risk, inflation expectations, and central‑bank reaction functions. Even if the oil price itself stabilizes or pulls back on signs of improving supply, the lingering uncertainty around Iran and regional stability can keep a geopolitical risk premium embedded across assets.

What This Means For Traders And Investors

In practical terms, the current Middle East backdrop demands tighter risk management and scenario planning. Energy traders should watch not only headline price levels but also indicators of physical stress such as tanker traffic through key chokepoints, inventory data, and official reserve releases.[3][10] A sudden drop in flows or renewed attacks on infrastructure could quickly revive the possibility of triple‑digit crude, with knock‑on effects for gasoline and distillates.

Macro and FX traders need to track how inflation expectations and rate‑hike probabilities evolve as new data arrive. If markets begin to price a materially more hawkish Fed response, the dollar could extend its strength against both developed‑market and emerging‑market currencies, potentially pressuring countries with large external financing needs. Conversely, any sign that central banks are willing to “look through” an energy‑driven inflation bump and prioritize growth could weaken the dollar and support risk assets, at least temporarily.[1][4][6]

For multi‑asset portfolios, one practical takeaway is to avoid relying on a single macro outcome. A balanced approach might combine exposure to energy equities or commodity indices—benefiting from sustained higher oil—with hedges in safe havens and selective dollar strength trades, while keeping position sizes modest enough to withstand headline‑driven volatility.

Simulated Finance: Practicing Risk Management In Real Time

Because the situation is fluid, it is an ideal environment to use simulated finance platforms to test strategies before committing real capital. War‑driven markets often produce sharp, fast moves followed by equally rapid reversals as new information emerges or diplomatic developments change the trajectory of conflict and energy supply.[12][13] That can punish traders who are over‑leveraged or relying on static assumptions about price behavior.

By practicing in a SimFi setting, traders can:

– Build and refine playbooks for different scenarios, such as “oil above $100 with hawkish Fed” versus “oil normalizes but growth slows.” – Experiment with position sizing, leverage, and hedging techniques in high‑volatility environments without financial damage. – Learn how cross‑asset correlations can change when geopolitics, inflation, and central‑bank policy all intersect, rather than relying on peacetime patterns.

Ultimately, the Middle East conflict and Iran war are a reminder that macro risk can re‑price markets quickly, especially where energy and inflation are concerned. Traders who understand how these forces support the dollar, shape safe‑haven flows, and challenge central banks will be better equipped—not just to react to the next headline, but to navigate the entire cycle of shock, adjustment, and eventual normalization.