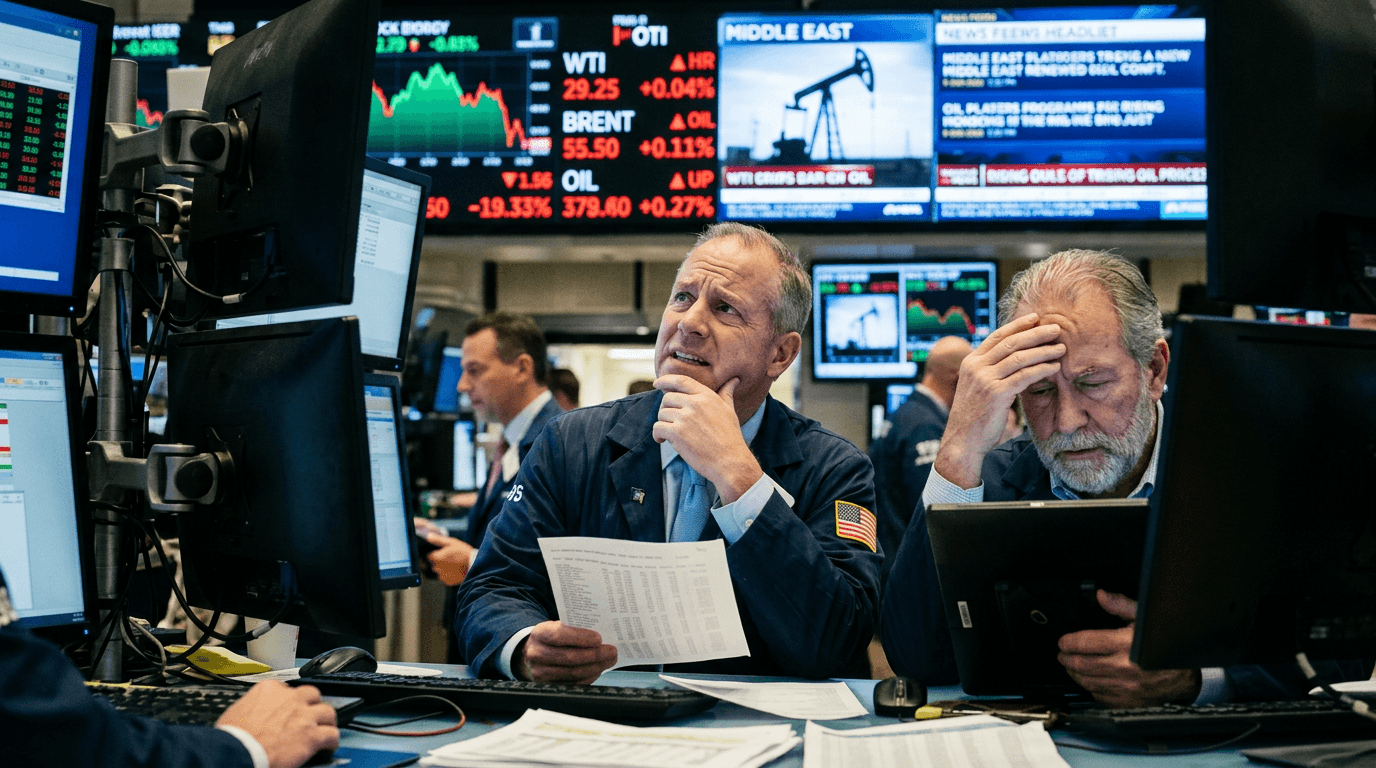

Oil prices have jumped sharply on the back of escalating conflict in the Middle East, and U.S. stocks are feeling the pressure as investors reassess both growth and inflation risks.[3][6][7] The combination of war-related supply fears and rising energy costs is reviving memories of past oil shocks – and raising serious questions about the future path of U.S. inflation and Federal Reserve policy.[1][6]

Markets React To Oil Shock

The immediate market reaction has been classic “risk-off.” Crude prices surged after U.S. and Israeli strikes on Iran, with U.S. benchmark oil jumping around 7–8% in a single session and Brent crude rising more than 6%, briefly trading above the low-$80s per barrel.[3][6] Concerns that the conflict could disrupt flows through key shipping routes and major producers have pulled forward fears of a broader supply shock.[6]

Equities have struggled under the weight of these moves. U.S. indexes have come off recent highs, and reports show trillions of dollars of market value erased in the first month of the conflict as investors price in higher industrial costs and trade disruptions.[4][7] While day-to-day index moves have been mixed, the broader picture is one of elevated volatility and a cautious tone, with many traders reducing risk exposure and rotating defensively.[3][7]

Safe-haven assets are back in favor. The U.S. dollar has strengthened against major currencies, gold has risen, and government bond yields have moved higher as inflation worries begin to overshadow early flight-to-safety buying.[3] This combination – stronger dollar, higher yields, and weaker equities – is typical of an environment where markets are worried that central banks might have to stay restrictive for longer.

Why Higher Oil Prices Matter For Inflation

Oil and gas feed into almost every corner of the economy. Rising crude prices quickly translate into higher gasoline and diesel costs, and from there into more expensive transportation, freight, and logistics.[1][5][6] Analysts warn that wholesale gasoline futures could jump significantly in the near term, feeding through to daily price increases at the pump.[6]

Recent inflation data already show energy reasserting itself as a key driver. Headline U.S. inflation has moved higher, with energy components – especially gasoline and fuel oil – posting double-digit year-on-year gains in some readings.[5] When fuel costs rise, the impact is not limited to drivers. It touches food prices (through transport), manufactured goods (through input and shipping costs), and services that rely on mobility or energy-intensive operations.[1][5]

Importantly, oil shocks can also shift inflation expectations. If households and businesses begin to assume that prices will keep rising, they may push for higher wages or increase prices preemptively. That dynamic can make inflation more persistent and harder to bring back to target. With core inflation still above central bank goals in many economies, an energy-driven flare-up is particularly unwelcome.[1][2]

Central Banks Walk A Tightrope

Central banks now face a familiar but difficult trade-off: contain inflation without choking off growth.[1] Economists note that the renewed Middle East conflict strengthens the case for many policymakers to keep interest rates higher for longer, rather than proceeding with aggressive cuts.[1] In effect, the oil shock is acting as a brake on the “dovish pivot” narrative that markets had started to price in.

For the Federal Reserve, the timing matters. Upcoming CPI releases are expected to show firm monthly gains in headline inflation, even if core measures are more subdued.[2] If gasoline and energy remain elevated, headline readings could surprise to the upside, forcing Fed officials to emphasize caution and data dependence. The central bank is unlikely to hike in response to a one-off shock, but a sustained rise in energy that spills into broader prices could keep rate cuts on hold.[1]

Other central banks, particularly in energy-importing regions, face similar dilemmas. Research from Asia, for example, suggests that a prolonged conflict could add several basis points to consumer inflation, especially in countries with a high energy weight in their CPI basket.[1] While the U.S. benefits from domestic production, it is still deeply tied to global pricing, and the Fed cannot ignore a durable oil shock.

WHAT THIS MEANS FOR U.S. STOCKS AND SECTORS

At the index level, higher oil prices tend to be a drag on equities because they compress margins and threaten consumer spending power.[4][7] However, the impact is far from uniform across sectors. Energy producers and some commodity-linked names can benefit from higher realized prices, while energy-intensive industries and consumer-focused companies generally suffer.

Sectors likely to feel pressure include airlines, travel, logistics, and parts of manufacturing, where fuel is a significant cost input. Retailers and consumer discretionary names may also be vulnerable if higher gasoline prices squeeze household budgets and redirect spending away from non-essential items. Meanwhile, utilities and defensives can attract flows from investors seeking stability amid macro uncertainty.

Financials sit in a nuanced position. On one hand, higher yields and a steeper curve can support banks’ net interest margins. On the other, volatility, potential credit stress, and weaker equity valuations can weigh on broader financial conditions. For index-level investors, this environment often leads to higher dispersion – the gap between winners and losers widens, making sector and stock selection more important.

How Traders Can Navigate This Environment

For traders and investors, the key is to understand that an oil shock is both a risk and an opportunity. The path of the conflict and the duration of elevated prices remain uncertain, and scenarios range from a short-lived disruption to a prolonged episode that could push crude toward $100 per barrel.[6] Staying flexible and scenario-aware is essential.

Several practical takeaways stand out

– Monitor energy data and inflation releases closely. Headline CPI, producer prices, and fuel cost indicators will drive central bank expectations and market narrative.[2][5]

– Watch correlations. In environments like this, oil, inflation breakevens, bond yields, and equity indexes can move together in distinctive patterns. Safe-haven flows into the dollar and gold, for instance, may signal rising systemic concern.[3]

– Focus on sector dynamics. Energy, materials, and select defensives may offer relative resilience, while high-duration growth stocks can be more sensitive to higher real yields and shifting Fed expectations.

– Use simulation and risk management tools. On a SimFi platform, traders can test strategies across different oil price and rate scenarios – from benign to stress – without putting real capital at risk. This can help refine approaches to hedging energy exposure, positioning around inflation data, or trading volatility in indexes and commodities.

Ultimately, the surge in oil prices and the Middle East conflict have reintroduced a classic macro risk into markets at a time when investors were hoping for a smooth disinflation and steady policy easing. Whether this becomes a brief scare or the start of a new inflation chapter will depend on both geopolitics and how quickly supply routes and expectations normalize. For now, markets are signaling that the inflation fight is not over – and that energy remains at the center of the story.