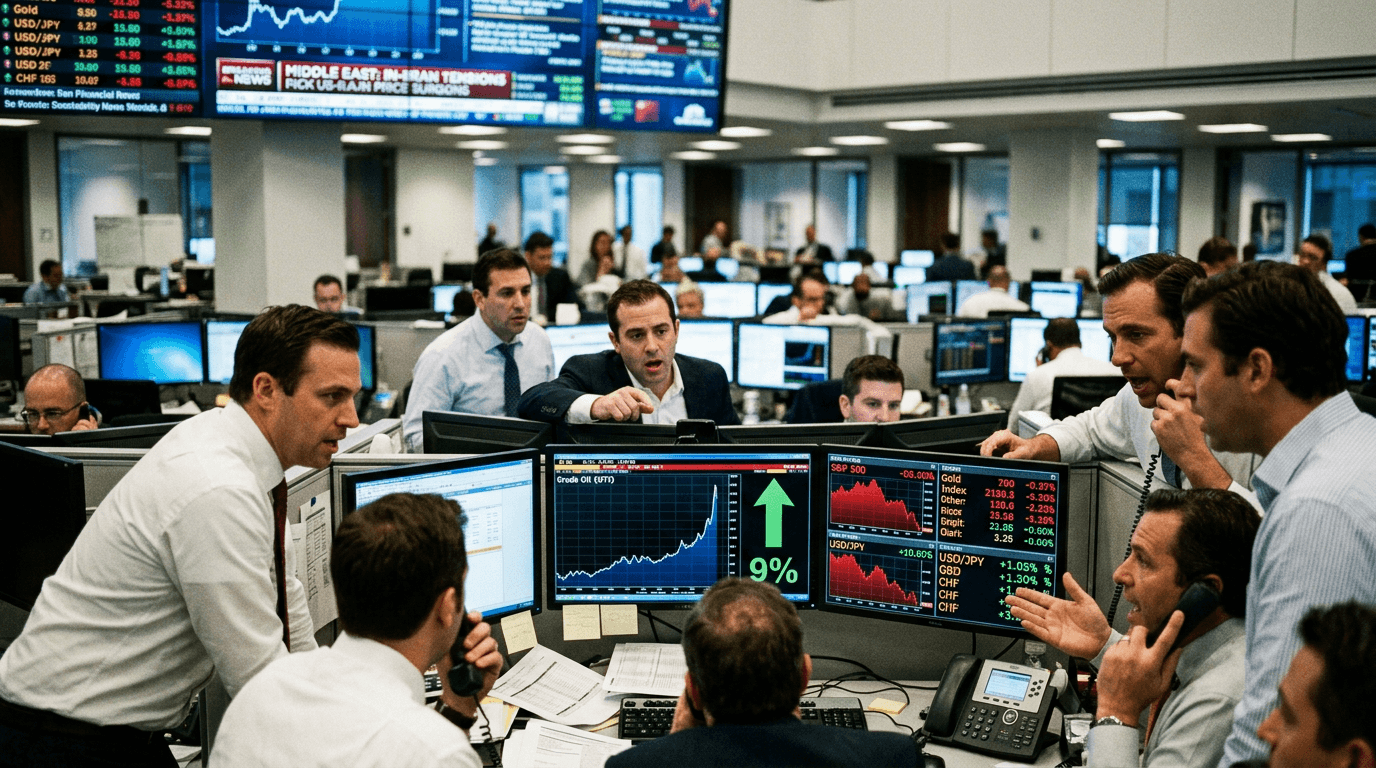

Crude oil futures have surged more than 9% as the US‑Iran conflict intensifies, thrusting energy markets back into the spotlight and rattling global risk sentiment. The sharp move is not just about oil—equities, currencies, and safe-haven assets are all recalibrating to a new geopolitical risk regime that traders cannot afford to ignore.

WHAT’S DRIVING THE 9% OIL SURGE

This spike in crude is rooted in supply risk, not a sudden demand boom. The key pressure point is the Strait of Hormuz, the narrow chokepoint through which roughly one‑fifth of the world’s oil supply typically passes. As military tensions escalate and shipping routes face heightened threat, markets are rapidly repricing the probability of a prolonged disruption.

When oil jumps more than 9% in a single session, that move is almost always about geopolitics or a major supply event—pipeline outages, embargoes, or war. Here, the market is effectively placing a risk premium on every barrel that must transit through a contested region.

For traders, the distinction between a demand shock and a supply shock matters. Demand-driven rallies often fade as growth cools or central banks step in. Supply shocks tied to physical disruption and geopolitical uncertainty tend to:

- Persist longer than expected

- Generate higher volatility and intraday reversals

- Spill over more aggressively into other asset classes

In other words, this is the kind of move that can reshape correlations and trading conditions for weeks or months, not just days.

How Energy Shocks Hit Equities

Equity markets responded quickly. US stock index futures moved lower as traders reassessed growth, margins, and inflation expectations.

Higher oil prices work through several channels

1. Cost pressure for corporates Energy is a key input cost for transportation, manufacturing, logistics, and chemicals. A sudden surge squeezes margins, especially for companies with limited pricing power. Airlines, shipping, trucking, and consumer discretionary names are typically among the first to feel the pressure.

2. Consumer squeeze and sentiment If elevated crude filters into gasoline and heating costs, consumers effectively face a tax on disposable income. That can weigh on retail, travel, and broader cyclicals as markets price in weaker demand.

3. Inflation and yields A genuine energy supply shock raises near‑term inflation expectations. If markets start to believe central banks may need to stay restrictive for longer—or at least delay rate cuts—bond yields can push higher, putting additional pressure on growth and tech valuations.

4. Sector rotation Not all equities suffer equally. Historically: - Energy producers, oilfield services, and some commodity-linked industrials often benefit - Energy‑intensive sectors and longer-duration growth stocks tend to underperform

For equity traders, the key is to think in relative terms. Even if headline indices are under pressure, dispersion between winners (energy, defense, some materials) and losers (transport, airlines, parts of consumer discretionary) can create opportunities.

Fx Reaction: Commodity Currencies Vs Safe Havens

The FX market’s response has been nuanced. Commodity‑linked currencies such as the Australian dollar (AUD) and Canadian dollar (CAD) initially found support as traders priced in the positive terms‑of‑trade shock from higher energy and resource prices. At the same time, safe‑haven demand for the US dollar (USD) and gold strengthened as risk aversion rose.

This creates a two‑step dynamic:

1. Initial commodity boost Markets often respond first to the straightforward story: higher commodity prices can benefit exporters. CAD, for example, frequently tracks oil due to Canada’s sizable energy sector. AUD can react to broader commodity optimism.

2. Risk‑off and dollar dominance As the geopolitical risk sinks in and equities wobble, a broader “risk‑off” move can overwhelm that initial reaction. If global growth fears rise and volatility picks up, capital tends to flow into perceived safe havens: - USD as the world’s reserve and funding currency - Gold as a hedge against tail risk and inflation - To a lesser extent, JPY and CHF as traditional havens

The result can be choppy price action where commodity currencies rally early, then fade as the USD’s safe‑haven bid strengthens.

For currency traders, the crucial questions are: - Does the market view this as primarily a commodity story (supportive for AUD/CAD) or primarily a global risk story (supportive for USD/JPY/CHF)? - Are central banks in commodity economies likely to lean more hawkish on inflation, or more cautious on growth?

The answers will shape medium‑term trends, not just the intraday reaction.

Trading Implications In A Geopolitical Oil Shock

Moves of this magnitude shift the entire trading environment. A few practical implications for active traders:

1. Expect elevated and persistent volatility Oil futures, energy equities, and related FX crosses are likely to see: - Wider intraday ranges - More frequent stop‑outs for tight risk parameters - Faster regime shifts on headlines

Position sizing and stop placement should reflect this. Reducing leverage while volatility is elevated can be more effective than constantly widening stops.

2. Respect headline risk Geopolitical markets are headline‑driven: - A credible ceasefire or de‑escalation headline can trigger violent reversals lower in crude and higher in risk assets - A surprise escalation, attack on infrastructure, or shipping incident can trigger another leg higher in crude and deeper risk‑off

In practice, this means: - Avoiding overconfidence in directional calls - Considering hedges (e.g., smaller, option-based structures when available) - Being cautious about holding large, unhedged positions through weekends or known diplomatic events

3. Watch cross‑market confirmation Use multiple assets to validate the move: - If oil is surging but gold and USD are not bid, the market may be treating it as a narrower commodity story - If oil, gold, USD, and volatility indices are all spiking together, the signal is broader risk aversion

Cross‑asset confirmation can help avoid overreacting to a move that lacks broader support.

4. Use simulated environments to stress‑test strategies In a SimFi setting, traders can: - Back‑test how their strategies behaved in past geopolitical shocks (e.g., prior Middle East crises, 2019 tanker incidents, Russia‑Ukraine energy spikes) - Forward‑test new risk rules, wider stops, or reduced sizing without real capital at risk - Explore correlation breakdowns—how indices, energy names, and FX pairs behave when the usual relationships stretch or invert

This kind of scenario testing is especially valuable when markets move into regimes that are rare in historical data.

What To Watch Next

The path of oil from here depends less on traditional macro data and more on geopolitics and logistics. Key drivers to monitor include:

- Diplomatic headlines: Any credible signs of de‑escalation, ceasefire proposals, or mediated talks could unwind some of the risk premium in crude.

- Shipping flows and insurance: Real‑time data on tanker traffic through the Strait of Hormuz, as well as changes in shipping insurance costs, will show how much physical disruption is actually occurring.

- Strategic reserves and OPEC signals: Coordinated releases from strategic petroleum reserves or production shifts from major producers could help stabilize prices, but markets will question how long such measures can be sustained.

- Inflation expectations and central bank rhetoric: If energy‑driven inflation expectations push higher, central bankers may shift tone, altering the path of rates and thus the valuation framework for equities and FX.

For traders, this episode is a reminder that geopolitical risk can reprice multiple asset classes at once and alter correlations that previously felt stable. An adaptive approach—focused on risk management, cross‑asset awareness, and scenario planning—is essential when oil becomes the market’s central narrative.