U.S. electricity demand is entering a new phase of structural growth, with the Energy Information Administration (EIA) projecting record consumption in 2026 and 2027 as AI data centers and electrification reshape the grid.[2][7] For traders and investors, this is not just a headline—it signals a sustained shift in the fundamentals of power, natural gas, and related commodity markets.[5]

What The Eia Is Signaling

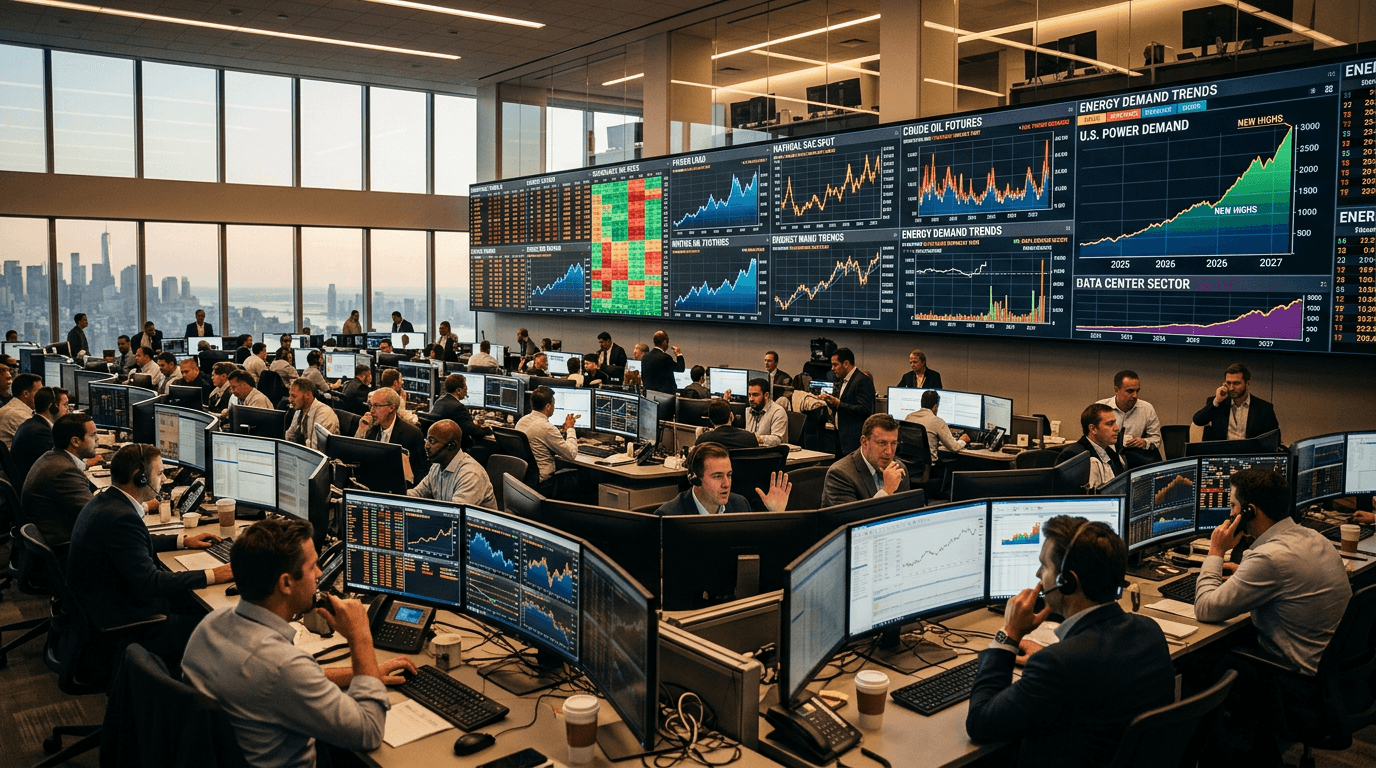

After roughly 15 years of nearly flat U.S. electricity use, demand has started growing again at an average of more than 2% per year in recent years.[7] The EIA’s Short-Term Energy Outlook now projects total U.S. electricity demand rising from a record 4,195 billion kilowatt-hours (kWh) in 2025 to around 4,244 billion kWh in 2026 and 4,381 billion kWh in 2027, marking consecutive all-time highs.[2] This is a meaningful acceleration compared with the historically slow pace of load growth.

The composition of demand is also shifting. Commercial sector electricity sales—where most data centers are classified—are on track to match or exceed residential consumption for the first time on record as early as 2026.[1][2] The EIA expects commercial sales to climb while residential use grows more modestly, reflecting the rise of large, power-intensive facilities rather than just household usage.[1][2]

On the supply side, the EIA projects coal’s share of generation to fall to about 15–17% by 2027, while natural gas holds roughly 40% and renewables expand from 24% of generation in 2025 to about 25% in 2026 and 27% in 2027.[1][3] Solar is the standout, with expected generation growth of 17% in 2026 and another 23% in 2027, while wind grows 6% and 7% over the same years.[3] These shifts matter for fuel demand, emissions, and the pricing dynamics across power and gas markets.

KEY TAKEAWAY: The EIA is flagging a multi-year, structural uptrend in U.S. electricity demand, led by the commercial sector and supported by a changing generation mix that leans more heavily on natural gas and renewables.[1][2][3][7]

Ai Data Centers As A New Load Giant

AI is not just a software story; it is an energy story. The rapid deployment of GPU-accelerated servers for AI has already contributed to more than a doubling of data center energy demand between 2017 and 2023, despite continued efficiency improvements.[4] New AI and cloud data centers typically consume hundreds of megawatts each, and collectively they are becoming one of the fastest-growing sources of electricity load.

Recent analysis finds that rising data center demand accounts for roughly 55% of forecast U.S. load growth over the next several years—about 90 gigawatts (GW) of new peak demand capacity.[4] Much of this growth is concentrated in regions such as Texas (ERCOT) and the Mid-Atlantic (PJM), which are already major hubs for both data centers and renewable generation.[4] Local grid constraints, transmission bottlenecks, and reliability concerns are therefore becoming critical issues in these markets.

For power traders, AI-driven data center build-outs translate into higher base load, more frequent peak constraints, and potentially greater price volatility during stress events. For natural gas, they support robust demand from gas-fired generation, particularly in regions where renewables and storage cannot fully cover the new load.

KEY TAKEAWAY: AI data centers are emerging as a dominant driver of U.S. electricity demand growth, reshaping regional load profiles and reinforcing the importance of gas-fired generation and flexible capacity.[1][2][4]

The Electrification Wave

Parallel to AI, broader electrification is adding steady, diversified demand. The EIA and independent research point to three main drivers:[4][7]

- Building electrification: Homes and commercial buildings are gradually shifting from fossil fuel heating to electric heat pumps and other electric systems, increasing baseline power use.[4][7]

- Transportation electrification: The growth of electric vehicles (EVs) is adding load through residential and commercial charging, particularly during evening peaks.[4]

- Industrial and manufacturing expansion: Onshoring and factory construction are boosting industrial electricity consumption, while some heavy industry (oil, gas, mining) begins to electrify processes.[4]

Together, residential and general commercial growth—including building electrification and EV charging—are estimated to contribute roughly 20% of expected new peak demand capacity over the next several years, with industrial and manufacturing adding another 20%.[4] This complements the more concentrated but intense demand from data centers, creating a broad-based load growth story.

KEY TAKEAWAY: Electrification across buildings, transport, and industry is a durable driver of electricity demand growth that supports the medium-term bullish case for power and gas alongside AI data centers.[4][7]

Implications For Power, Natural Gas, And Commodity Futures

In its latest outlook, the EIA expects U.S. natural gas consumption in the electric power sector to set a record next year, driven largely by rising overall electricity demand.[5] Gas-fired plants remain the primary source of flexible generation, filling gaps when solar and wind output fall short or when demand spikes.[1][3][5] The EIA forecasts Henry Hub spot prices averaging around $3.34 per MMBtu in the second half of 2026 and $3.55 in the second half of 2027, reflecting firm but not extreme pricing amid rising consumption.[5]

For power markets, the combination of record demand, regional constraints, and a complex fuel mix suggests:

- Higher baseline load and potentially tighter reserve margins in some regions, especially ERCOT and PJM.[4]

- Greater sensitivity of prices to extreme weather, outages, and transmission constraints, with more pronounced spreads between off-peak and peak periods.

- Increasing importance of renewables, storage, and demand response in balancing the system, but with gas remaining essential for reliability.[1][3][5]

From a futures and SimFi trading perspective, this structural demand growth is a medium-term bullish factor for U.S. power and natural gas contracts, and it is already influencing flows into utilities, midstream, and infrastructure-related equities.[1][5] Traders need to think less in terms of short-lived demand spikes and more in terms of a sustained upward shift in the load curve.

KEY TAKEAWAY: Record electricity demand and robust gas-fired generation underpin a constructive medium-term view on U.S. power and natural gas, with regional dynamics and volatility likely to become more important for trading strategies.[1][4][5]

How Traders And Investors Can Position

For market participants, the key is to translate these structural trends into actionable frameworks:

- Focus on regional fundamentals: Track load growth, capacity additions, and transmission constraints in specific hubs such as ERCOT and PJM, where data center and industrial growth are concentrated.[4]

- Monitor the generation mix: Rising solar and wind will increasingly shape daily price patterns, while gas sets marginal prices in many hours. Understanding when renewables saturate the grid—and when they fall short—will be critical for intraday and seasonal strategies.[1][3][5]

- Incorporate structural demand growth into scenarios: When modeling power or gas futures, assume a higher baseline of consumption through 2027 and stress-test portfolios against scenarios of faster AI deployment or accelerated electrification.[2][4][7]

- Watch policy and regulation: Grid planning, data center siting rules, transmission build-out, and incentives for renewables or storage can materially alter the balance between supply and demand. Policy risk is becoming central to power and infrastructure investing.

Whether you trade simulated power and gas futures or invest in utilities, pipeline operators, and renewable developers, the EIA’s outlook is a signal that the old paradigm of flat demand is over. The coming years are likely to be defined by higher loads, evolving fuel shares, and more complex regional price behavior—all of which reward informed, forward-looking strategies.

KEY TAKEAWAY: Integrating AI-driven load growth and electrification into your market framework is no longer optional; it is essential for anyone trading or investing in U.S. power, gas, and energy-linked assets.[2][4][5][7]