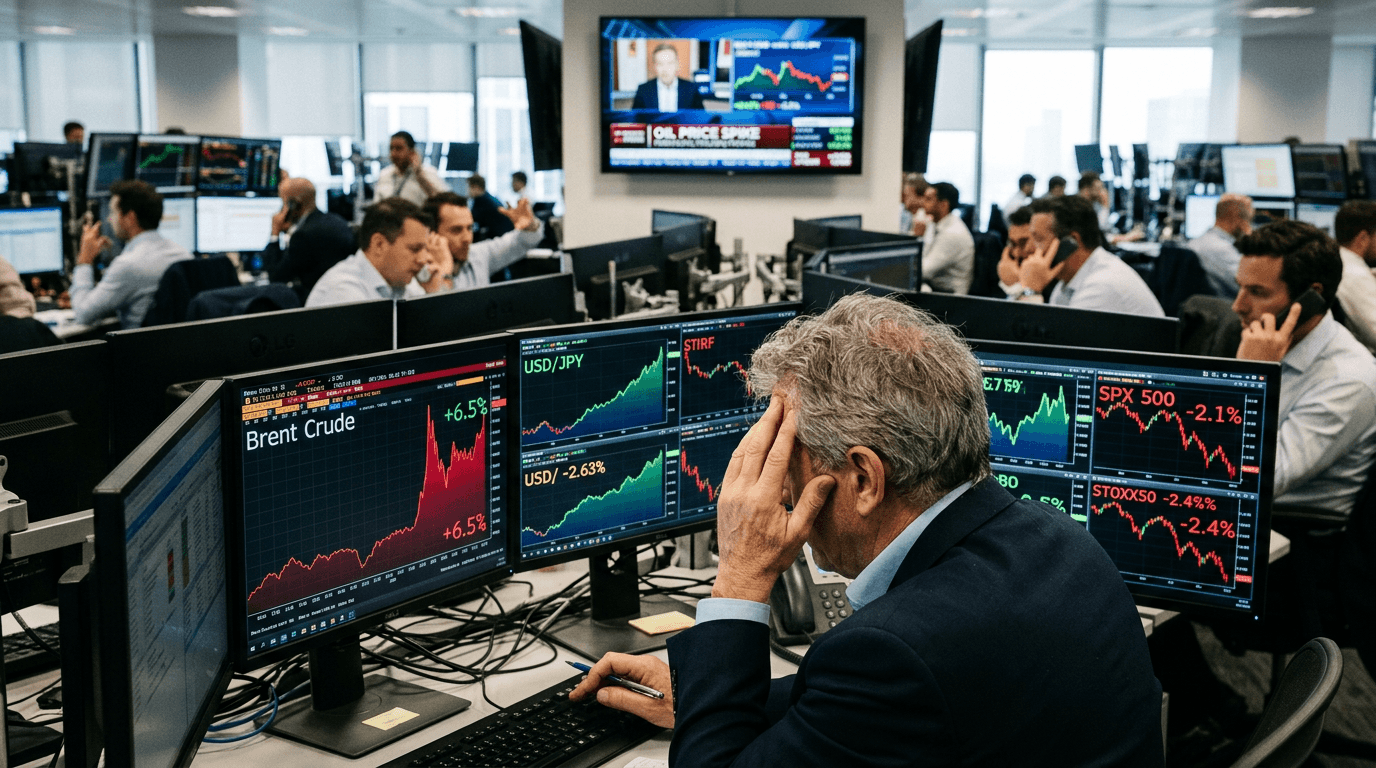

A fresh wave of risk aversion has swept through global markets as escalating tensions between the US and Iran push crude oil sharply higher. West Texas Intermediate (WTI) surged as much as 9%, briefly tagging multi‑month highs, while Brent crude pushed toward the mid‑$80s. The move has reignited inflation concerns, hit equities and futures, and driven a classic safe‑haven bid into the US dollar and Japanese yen, at the expense of higher‑beta currencies and risk assets.

WHAT’S DRIVING THE RISK-OFF MOVE

At the core of the market reaction is the fear of supply disruption in key Middle Eastern shipping routes. Even when barrels are still flowing, the mere threat to chokepoints like the Strait of Hormuz forces traders to reprice the risk premium in oil.

Higher energy prices quickly filter into inflation expectations, freight and input costs, and ultimately corporate margins. Equities, particularly in energy‑intensive sectors such as airlines, transport, and manufacturing, tend to struggle when an oil spike appears more structural than transient.

In FX, investors are de‑leveraging carry trades and rotating into perceived safe havens. The dollar index is firmer, the yen has bounced from recent lows, and traditional risk proxies like the Australian dollar, emerging‑market currencies and equity index futures are under pressure.

Why Oil Shocks Tend To Lift The Dollar And Yen

A sustained oil spike usually favors the US dollar for two structural reasons.

First, the US is relatively energy‑insulated compared with major importers. Having become a net crude and refined product exporter in recent years, the US still feels the pain of higher gasoline and diesel, but its overall terms of trade can be less damaged than those of regions such as the euro area or Japan, which rely heavily on imported energy. That differential supports capital flows into dollar assets when oil is rising.

Second, higher oil often forces markets to reassess the path of Federal Reserve policy. If energy‑driven inflation shows signs of feeding into core prices, traders scale back expectations for rate cuts, or even flirt with the idea of renewed tightening. That repricing can push US real yields higher, which historically supports the dollar against both low‑yielding and high‑beta currencies.

The yen’s behavior is more nuanced. Japan is a large energy importer, so structurally, expensive oil is a negative. However, during periods of global stress, Japanese institutions often repatriate capital, and leveraged positions funded in yen get unwound. This “short‑yen squeeze” can override fundamentals, giving the currency a safe‑haven profile.

The complication today is that USD/JPY is already trading near levels that have previously invited talk of official intervention. As yields adjust and risk aversion rises, traders must balance the yen’s haven appeal with the non‑trivial risk that authorities step in if the pair revisits or breaks perceived “lines in the sand.”

Winners, Losers And Key Market Themes

In FX, the clear short‑term winners are the dollar and, to a lesser extent, the yen and Swiss franc. Currencies of energy‑importing economies with loose policy stances or fragile external balances tend to lose ground.

The euro and sterling can be pressured by deteriorating terms of trade and growth fears, while the Australian and New Zealand dollars, as classic risk‑sensitive, high‑beta currencies, often underperform when global volatility spikes, regardless of their commodity ties. Emerging‑market FX is typically hit hardest as investors unwind carry trades and retreat to more liquid, defensive positions.

On the equity side, global index futures are pointing lower, with cyclicals, small caps, and growth names at greater risk. The exception is the energy sector, where producers and select service companies can benefit from stronger crude prices, at least initially.

In rates, front‑end yields may drift higher if markets price fewer Fed cuts due to renewed inflation concerns, even as longer‑dated yields are capped by safe‑haven bond buying. The result can be a flatter or even re‑flattening yield curve, a classic sign that growth fears are growing alongside inflation anxieties.

For commodities, oil is the center of gravity, but second‑round effects can appear in natural gas, refined products, and even agricultural commodities via higher transport and fertilizer costs. Volatility tends to spike, widening intraday ranges and increasing the risk of stop‑outs for over‑leveraged traders.

Implications For Simulated Traders

For traders using a Simulated Finance environment, this kind of event‑driven volatility is an opportunity to stress‑test strategies without real‑world capital at risk.

First, review your correlation assumptions. In calmer markets, it is easy to forget that correlations can jump toward one in a genuine risk‑off move. Equity indices, high‑beta FX and commodities can all sell off together, amplifying portfolio swings. Use the current environment to observe how cross‑asset correlations behave during geopolitical shocks.

Second, practice scenario planning. Build simple “if‑then” frameworks: If WTI holds above recent highs for several sessions, do you expect further downside in the euro and yen crosses? If oil quickly retraces the spike, which trades are likely to mean‑revert first? Simulated trading allows you to test these hypotheses in real time, refining your playbook for future events.

Third, tighten your risk management. Wider spreads and bigger intraday ranges mean position sizing and stop placement matter more than ever. In a SimFi account, experiment with scaling into trades rather than entering full size at once, and test how different stop‑loss distances affect your P&L distribution when volatility is elevated.

Finally, pay attention to news timing. Many of the fastest moves around geopolitical headlines happen when liquidity is thinner—early Asia, late US, or into weekend gaps. Track how your simulated orders are filled in those conditions and consider whether you would adjust your approach in live trading, for example by reducing overnight exposure ahead of key risk events.

What To Watch Next

From here, the key questions are whether the oil move proves temporary or evolves into a sustained price shock, and how central banks respond.

If tensions ease and shipping routes stabilize, crude may give back a chunk of its risk premium, taking some pressure off inflation expectations and allowing risk assets to find a footing. In that scenario, the dollar and yen could surrender part of their haven gains as traders rotate back into higher‑yielding and growth‑linked assets.

If, however, supply disruptions deepen or the conflict broadens, energy prices could remain elevated for longer. That would raise the odds of stickier inflation, complicate the path for rate cuts—especially for the Fed—and potentially revive the “stagflation Lite” narrative that weighed on markets during previous energy shocks. Under that backdrop, the dollar could stay supported, while the yen’s trajectory would hinge on both risk sentiment and the stance of Japanese policymakers.

For now, traders—real and simulated—are being reminded that geopolitical risk is not a theoretical chapter in a textbook but a live, market‑moving force. Understanding how oil, FX, equities and rates interact in these moments is critical preparation for navigating the next bout of volatility, whenever it arrives.