The Indian rupee’s slide to successive record lows near 96.20 per dollar is more than a headline-grabbing move in foreign exchange markets. It is the nexus of three powerful forces: an oil price shock tied to geopolitical conflict, a global bond selloff pushing yields sharply higher, and persistent capital outflows from emerging markets. Together, they are rewriting India’s macro narrative and offering a live case study in how external shocks can ripple through currencies, inflation, and central bank policy.

What's Driving The Rupee's Slide

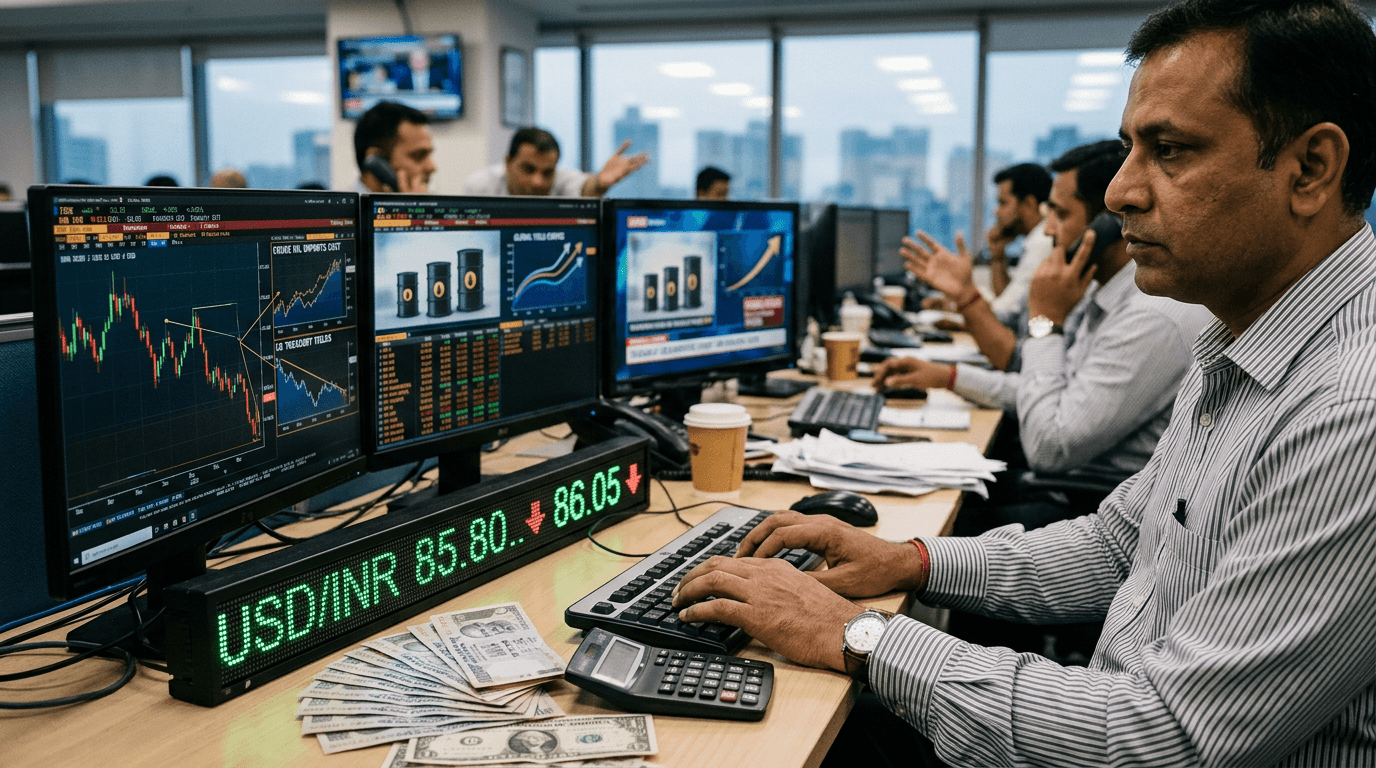

The rupee has fallen roughly 5% since the Iran conflict escalated and tensions in the Strait of Hormuz disrupted global energy flows, pushing Brent crude well above the $100 per barrel mark. Recent prints near 96.20 per dollar mark fresh all‑time lows, cementing the rupee’s status as Asia’s worst-performing major currency so far this year.

Three intertwined drivers stand out

1) Oil shock: India imports more than 90% of its crude needs. Higher oil prices directly widen the trade deficit and worsen the current account.

2) Global yield spike: A synchronized bond selloff has pushed US 10‑year yields toward the mid‑4% region and long-end yields above 5%. Higher risk-free rates in developed markets pull capital away from emerging markets.

3) Risk-off sentiment: Elevated geopolitical risk, inflation concerns, and tighter global financial conditions reduce appetite for EM assets, amplifying outflows from Indian bonds and equities.

This combination puts sustained downward pressure on the rupee even as the Reserve Bank of India (RBI) steps in periodically to smooth volatility.

Key takeaway: The rupee’s weakness is not an isolated event; it is the visible symptom of deeper global and domestic macro pressures.

Oil Shock And India's Macro Balance

For an energy‑importing economy, oil is the swing factor that can rapidly change the macro picture.

When crude prices surge

- Trade deficit widens: India pays more dollars for the same volume of oil. That increases the current account deficit, all else equal.

- Terms of trade deteriorate: India must export more goods and services to pay for the same amount of imports, squeezing national income.

- Imported inflation rises: Higher fuel and transportation costs eventually pass through to prices of food, manufactured goods, and services.

The recent jump in Brent crude prices, driven by conflict‑related supply disruptions and risk premia, has sharply raised India’s energy import bill. Even though domestic retail fuel prices have been partially shielded by administrative controls, that protection cannot last indefinitely if global prices stay high.

Economists have already been cutting growth forecasts and lifting inflation projections. For the rupee, this combination is toxic: weaker growth expectations reduce the currency’s attractiveness, while higher inflation undermines real returns for investors holding rupee assets.

Key takeaway: As long as oil stays elevated, the rupee faces a persistent structural headwind through the trade balance and inflation channel.

Global Bond Selloff And Capital Flows

The oil shock is being compounded by a global bond selloff that has lifted yields across developed markets. Higher US Treasury yields are particularly important for EM FX for three reasons:

1) Wider interest rate differentials: When US yields rise faster than Indian yields, the relative appeal of rupee assets diminishes.

2) Portfolio rebalancing: Global investors rotate toward safer, higher‑yielding developed market bonds, reducing allocations to EM debt and equity.

3) Stronger dollar backdrop: Rising US yields often support a stronger dollar, creating broad pressure on EM currencies.

For India, this has translated into:

- Outflows from bond markets as foreign investors reassess duration and currency risk.

- More volatility in equities, especially in sectors sensitive to global rates and risk appetite.

- Increased hedging demand from corporates, especially those with external commercial borrowings and dollar-linked liabilities.

The result is a feedback loop: outflows weaken the rupee, a weaker rupee raises hedging costs and inflation risks, and those risks can further dampen investor appetite.

Key takeaway: As long as global yields remain elevated and volatile, capital outflows and a strong dollar will keep the rupee under pressure, regardless of domestic fundamentals.

Rbi's Dilemma And Policy Options

The Reserve Bank of India is effectively juggling three objectives: containing inflation, supporting growth, and maintaining financial stability. A sharp FX move complicates all three.

RBI’s current toolkit and approach include:

- FX intervention: Selling dollars from its reserves to slow the pace of rupee depreciation and reduce intraday volatility.

- Macroprudential and regulatory steps: Adjusting capital flow rules, tightening speculative positions, or tweaking import/export norms to ease pressure on the currency and the balance of payments.

- Interest rate policy: Hiking policy rates to defend the currency is generally seen as a last resort. It can stabilize the rupee in the short run but risks choking credit and growth.

Recent commentary suggests the RBI is willing to “look through” temporary supply shocks but could act if inflation pressures become entrenched. With core inflation already elevated and fuel pass‑through looming, that line may be tested.

At the same time, authorities are exploring steps to conserve FX reserves and manage the import bill, including higher tariffs on certain imports and targeted measures aimed at reducing non-essential dollar demand.

Key takeaway: Expect more FX smoothing and targeted regulations first; outright rate hikes purely for currency defense are less likely unless inflation expectations de-anchor.

What Traders And Investors Should Watch

For traders in both live and simulated environments, the rupee’s decline offers a real‑time macro case study and multiple actionable signals.

1) Oil‑FX linkage: Watch Brent crude and USD/INR together. Sustained moves in oil often lead rupee moves, with lags that can create trading opportunities.

2) Yield differentials: Track US-India yield spreads at the 2‑year and 10‑year tenors. Widening differentials in favor of the US typically coincide with rupee weakness.

3) RBI footprints: Spikes in FX turnover, abrupt intraday reversals, or narrowing bid‑ask spreads after disorderly moves often hint at RBI activity. Understanding these patterns can improve timing on directional trades.

4) Volatility and options pricing: Rising implied volatility in USD/INR options can signal stress before spot reaches new levels. For strategy testing, this is fertile ground for exploring hedged positions and event-driven trades.

5) Cross‑asset signals: Indian equity and bond markets, especially bank and energy stocks, often react to currency stress. Correlations can shift quickly during episodes like this, so monitoring cross‑asset moves is critical.

For risk management, this environment underscores the value of:

- Scenario analysis: Stress-testing portfolios for further INR depreciation (e.g., 98 or 100 per dollar scenarios) and higher domestic rates.

- Currency hedging: Evaluating the cost-benefit of hedging exposures versus tolerating FX volatility.

- Time horizon discipline: Distinguishing between short-term overshoots driven by positioning and medium-term structural moves driven by oil and policy.

Key takeaway: The rupee’s move is a live training ground for understanding macro‑FX linkages, policy reactions, and cross‑asset dynamics—valuable for both real and simulated trading.

Conclusion

The rupee’s slide to successive record lows is not a random fluctuation; it is a concentrated expression of the pressures facing energy‑importing emerging markets in a world of high oil prices and rising global yields. For India, the combination of a deteriorating trade balance, stickier inflation risks, and capital outflows will keep the currency in focus and the policy debate intense.

For market participants, the message is clear: watch oil, watch global yields, and watch the RBI. The interplay of these three forces will largely determine whether the rupee stabilizes, grinds weaker, or experiences further bouts of sharp volatility. In the meantime, the current environment offers a rare, high‑signal backdrop for learning, testing, and refining macro and FX trading strategies—whether in live markets or in a simulated finance setting.