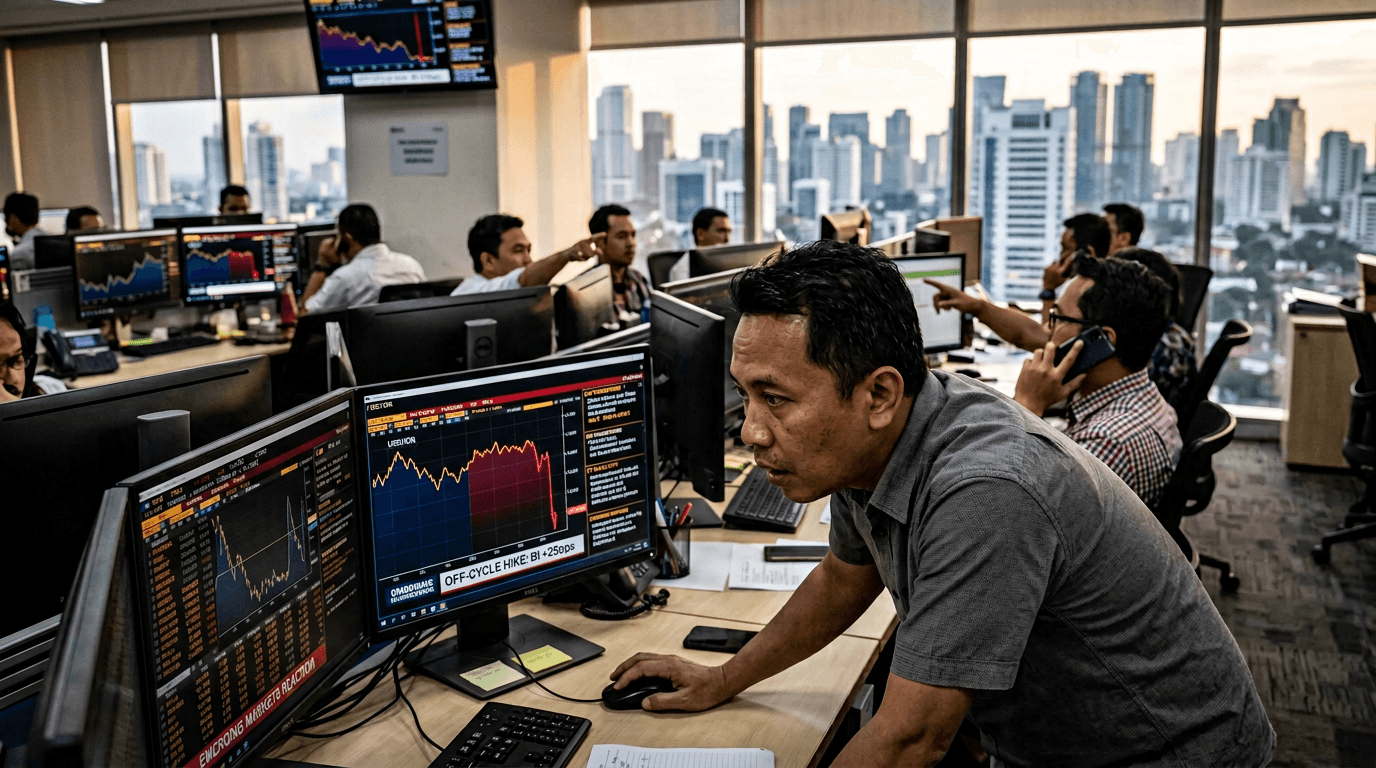

The Indonesian rupiah finally caught a break after weeks of relentless pressure, strengthening in the wake of a surprise, off-cycle 25 basis-point rate hike from Bank Indonesia (BI). The unscheduled move broke a four-day winning streak in USD/IDR, signaling that policymakers are no longer willing to tolerate rapid currency weakness and are prepared to act between regular meetings to restore stability.[1][3] For traders, this is a textbook example of how central bank surprises can reset market narratives in emerging markets.

What Happened: A Surprise Move To Defend The Rupiah

Bank Indonesia raised its benchmark rate by 25 basis points in an off-cycle decision, taking the policy rate to around 5.50%.[1] This was not a scheduled meeting, which is precisely why the move mattered: it sent a strong signal that stabilizing the rupiah has become an urgent priority.

According to official comments, the hike was a “further step” to strengthen rupiah stability amid “high global volatility” linked to geopolitical tensions in the Middle East and to preemptively keep inflation within target in 2026–2027.[1] The central bank also explicitly highlighted the goal of improving returns to attract foreign portfolio inflows into Indonesian assets.[1]

In FX space, the reaction was immediate. The rupiah, which had just touched record lows near 18,190 per US dollar, firmed to roughly 18,085–18,100 after the decision, snapping USD/IDR’s four-day advance.[1][3] While the move in spot was modest, the message was loud: policymakers are willing to tighten policy to defend the currency, even at the cost of higher domestic borrowing costs.

Why The Rupiah Was Under Pressure

To understand why this hike matters, you need to look at the backdrop. The rupiah has been one of the worst-performing major emerging market currencies this year, having fallen around 8% year-to-date and about 7% over the prior twelve months, according to recent reports.[7] It had repeatedly printed fresh record lows against the dollar before this intervention.[1][7]

Several forces have been working against Indonesia’s currency:

- Strong US dollar and higher-for-longer US rates, which tend to drain capital from higher-yielding but riskier emerging markets into safer US assets.

- Global risk aversion driven by geopolitical tensions, particularly the war in the Middle East, amplifying volatility and making investors more cautious about EM exposure.[1]

- Local positioning and sentiment, as markets started to test BI’s tolerance for rupiah weakness, pushing USD/IDR higher in a self-reinforcing move.

Academic research underscores how damaging a weaker rupiah can be for Indonesia’s broader economy. One study finds that a 1% depreciation in the rupiah is associated with a 0.91% decline in aggregate Indonesian stock market returns, and a 10% depreciation is linked to a 4.3% drop in exports.[4] In other words, prolonged currency weakness is not just a market story; it spills over into growth, corporate earnings, and investor confidence.

By acting off-cycle, BI is trying to arrest that negative feedback loop before it becomes entrenched.

Market Reaction: Fx, Bonds, And Flows

The most visible impact was in the FX market, where USD/IDR retreated from record highs, breaking its recent uptrend.[1][3] For traders, that break in the four-day winning streak is a technical confirmation that the policy surprise has at least temporarily altered the balance of risks.

Beyond FX, the move has implications across Indonesian assets:

- Bond yields: A rate hike typically pushes local bond yields higher as markets price in tighter monetary conditions and possibly more hikes to come. That can pressure existing holders of duration but may improve the medium-term appeal of Indonesian bonds for yield-seeking investors.

- Capital flows: By increasing the interest rate differential versus developed markets, BI is explicitly trying to support foreign portfolio inflows.[1] Higher yields can attract fresh capital into government bonds and money-market instruments, which in turn supports the rupiah.

- Inflation expectations: Front-footed tightening helps anchor inflation expectations by signaling that BI is committed to keeping price growth within its target band over the coming years.[1] Well-anchored expectations reduce the risk of a deeper, more painful tightening cycle later.

For now, the reaction is consistent with the idea that the central bank has reasserted its credibility. But the sustainability of rupiah strength will ultimately depend on global conditions, US yields, and whether BI follows through with additional measures if needed.

What This Means For Traders And Investors

This episode is rich with lessons for both discretionary traders and systematic strategies.

First, it highlights the importance of monitoring central bank communication and not assuming policy moves only happen on scheduled dates. Off-cycle actions tend to carry more informational value because they signal urgency. For FX traders, this can mean:

- Sudden repricing in currency pairs such as USD/IDR, with stops and technical levels being hit quickly.

- Expanded volatility, which affects position sizing, margin requirements, and risk management parameters.

- Reassessment of medium-term fair value levels for the rupiah, as higher real yields are factored into models.

Second, it underscores how closely linked FX and local rates markets are in emerging economies. A surprise rate hike aimed at currency stabilization can simultaneously:

- Offer carry opportunities for investors willing to hold higher-yielding local assets.

- Raise funding costs for corporates and governments, with potential knock-on effects on equities and credit spreads.

Research showing the sensitivity of Indonesian equities and exports to FX moves suggests that any sustained stabilization in the rupiah could be supportive for local stocks over time, particularly for sectors that are heavily exposed to import costs or foreign currency debt.[4]

Trading Central Bank Surprises In A Simulated Environment

For traders using simulated finance (SimFi) platforms like E8 Markets, events like this are ideal case studies to practice navigating macro shocks without real capital at risk.

Here are practical ways to turn this BI surprise into a learning opportunity:

- Build trade scenarios: Design multiple USD/IDR scenarios (e.g., continued rupiah recovery, stabilization, renewed weakness) and test how different strategies perform across them. Include both directional trades and options-style payoffs if your simulation tools allow it.

- Stress-test risk management: Use the volatility around the announcement to evaluate whether your stop-loss distances, position sizes, and max drawdown limits are robust to sudden policy shocks.

- Link FX to other assets: Simulate a cross-asset approach by looking at how Indonesian bond yields and equity indices might react to a stronger rupiah and higher rates. Practice building a macro narrative that connects FX, rates, and equities rather than trading each in isolation.

- Backtest response to similar events: Compare this move with past episodes when BI or other EM central banks delivered surprise or off-cycle hikes. Examine how long the currency support typically lasted and what differentiated successful defenses from short-lived bounces.

By repeatedly modeling these situations in a risk-free environment, traders can refine their playbooks so that, when similar real-world surprises hit, their response is disciplined rather than reactive.

Looking Ahead: Key Levels And Questions

The immediate question for markets is whether this off-cycle hike marks a turning point or just a brief pause in rupiah weakness. Key watchpoints include:

- Follow-up communication from BI: Any hints about the possibility of further hikes, FX interventions, or macroprudential measures will shape expectations.

- US dollar and global yields: If US rates remain elevated or rise further, the pressure on EM FX, including the rupiah, may re-emerge.

- Data flow: Inflation, growth, and balance-of-payments data will indicate whether BI’s move is sufficient to stabilize both prices and the external position.

For traders, the main takeaway is that in emerging markets, central bank credibility is often expressed through decisive action during stress. Bank Indonesia has just reminded markets that it is willing to act outside the usual timetable to defend the rupiah. Whether this proves to be the start of a more sustained recovery in the currency will depend on a delicate balance between domestic policy, global conditions, and investor risk appetite.