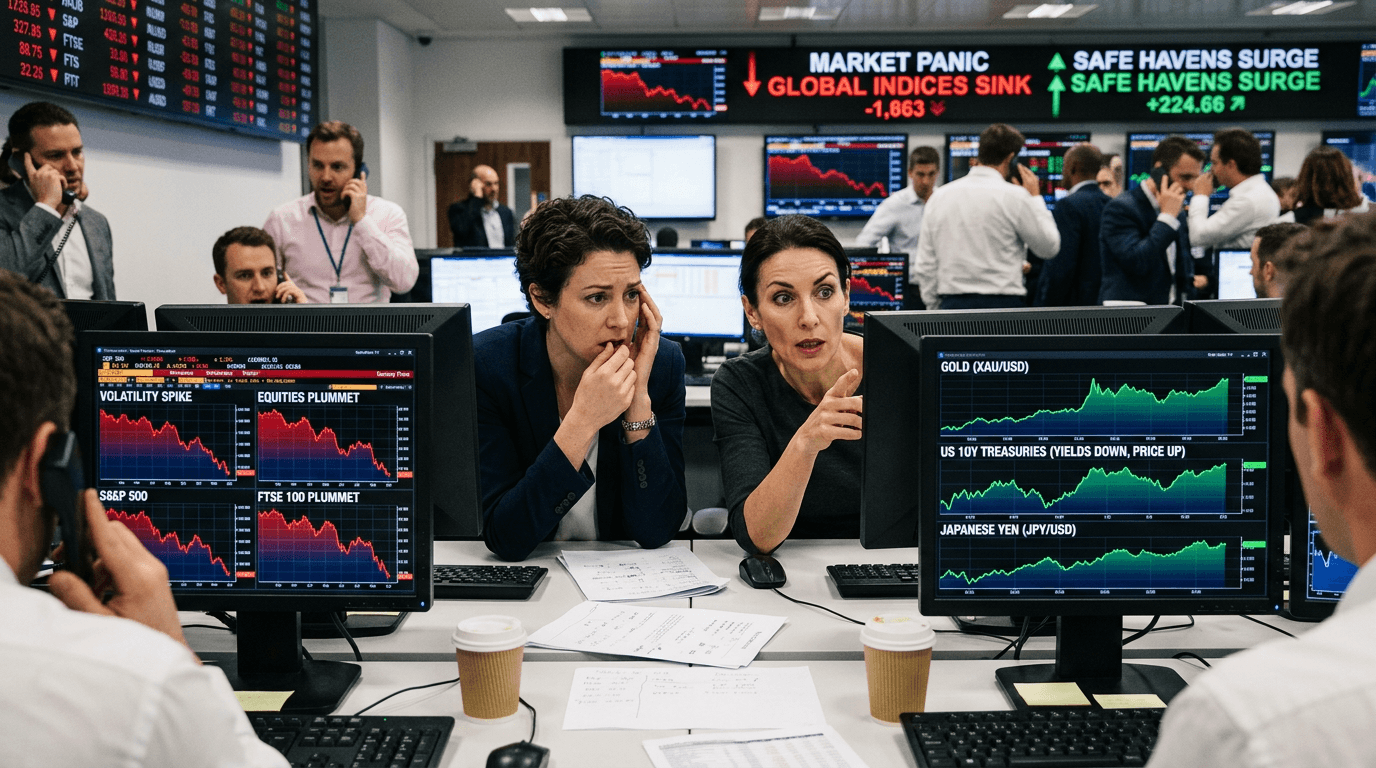

Markets are waking up to the reality that the US–China trade war has entered a new, more dangerous phase. With US tariffs on Chinese goods raised to around 145% and China retaliating with duties up to 125%, the cost of trading between the world’s two largest economies has effectively exploded.[3][8] For traders, that is translating into sharp losses across risk assets and powerful flows into classic safe havens like the Japanese yen, Swiss franc, gold, and government bonds.[1][4]

WHAT JUST HAPPENED – AND WHY IT MATTERS

The latest tariff salvo takes an already tense situation into “prohibitively expensive” territory. Reciprocal tariffs above 100% make many cross-border trades uneconomical, increasing the risk of a meaningful slowdown in global trade.[2] This is not just a headline risk; it directly affects corporate margins, investment plans, and ultimately earnings expectations.

Past research on earlier phases of the US–China trade war shows that “trade war shocks” can explain a significant portion of short-term moves in US stocks and Treasury yields.[1] In those episodes, markets reacted with:

- Immediate drops in equity indices such as the S&P 500

- Lower Treasury yields as investors sought safety

- Wider credit spreads and weaker oil prices

- Stronger US dollar and higher gold prices[1]

The current escalation is even more aggressive in tariff magnitude, so it is no surprise that global equities, commodity futures, and cyclical currencies are under pressure while defensive assets outperform.[3][4]

Safe-haven Flows Vs Risk Assets

When geopolitical or policy risks spike, markets often flip from “risk-on” to “risk-off” behavior. The latest tariff shock is a textbook example.

Safe havens are attracting inflows

- Government bonds: Yields tend to fall as investors move into US Treasuries, Bunds, and other high-quality sovereign debt, seeking capital preservation and liquidity.[1][4]

- Gold: As a non-yielding store of value, gold has historically rallied during trade and geopolitical shocks.[1][4]

- Yen (JPY) and Swiss franc (CHF): These currencies benefit from safe-haven demand, given Japan’s net creditor position and Switzerland’s reputation for stability.[4]

Risk assets and cyclical plays are being hit

- Global equity index futures: Trade-sensitive indices, especially those with heavy tech, industrial, and export exposure, are vulnerable to downgrades in global growth expectations and supply-chain uncertainty.[1][3]

- Commodity futures: Industrial commodities and energy often weaken as traders price in slower trade and manufacturing activity.[1][4]

- Cyclical FX: Currencies tied to global growth and commodities (for example, those of export-oriented or emerging economies) typically underperform when trade fears intensify.[2][5]

The mechanism is straightforward: higher tariffs mean higher costs and lower volumes for global trade, which reduces growth expectations and risk appetite. The International Monetary Fund previously estimated that US–China tariff escalations could shave about 0.3% off global GDP in the short term, with roughly half of that impact coming from confidence and market sentiment rather than direct trade effects.[5] Markets are now repricing that confidence channel aggressively.

How Tariffs Hit Different Asset Classes

Equities

Equity markets are most visibly affected. Firms with significant revenue exposure to China, complex global value chains, or high import content from China tend to be hit hardest.[1][3] Earlier in the trade war, companies that sold heavily into the Chinese market suffered more than those that simply sourced inputs from China.[1]

Key transmission channels include

- Margin pressure as import costs rise

- Demand uncertainty as trade volumes slow

- Capex and hiring delays as businesses wait for clarity

Technology, industrials, autos, and capital goods often sit at the epicenter because of their dependence on cross-border supply chains and sensitive export markets.[3]

Fixed Income

Government bonds typically rally during trade tensions:

- Yields decline as investors seek safety and price in slower growth

- Yield curves may flatten if markets expect future rate cuts or prolonged low rates

Credit markets can show stress through wider spreads, especially in high-yield or companies with heavy trade exposure, as investors reassess default risk in a weaker growth environment.[1]

Currencies

FX markets translate the risk-off shift into:

- Stronger JPY and CHF as safe-haven demand rises[4]

- Potential strength in the US dollar versus EM and cyclical FX, given its reserve status and relatively deep markets[1][5]

- Pressure on export-oriented or commodity-linked currencies as global growth expectations are revised down[2][5]

This can create powerful short- to medium-term trends in FX pairs tied to risk sentiment.

Commodities and Crypto

Industrial commodities such as oil often fall when markets anticipate weaker manufacturing and trade.[1][4] Crypto assets, still viewed primarily as speculative risk assets, tend to trade more like tech/growth stocks than safe havens during major macro shocks, and can suffer alongside equities when volatility spikes.[4]

Trading And Risk Management Implications

For active traders and investors, an escalation of this magnitude has several practical implications:

1. Respect volatility and liquidity

Bid–ask spreads often widen during trade shocks, and intraday ranges can expand dramatically. Position sizing, stop placement, and execution strategies need to adapt to higher volatility regimes.

2. Watch the macro narrative, not just the numbers

Tariffs at 145% and 125% are not just incremental changes; they shift the regime.[3][8] Markets will trade not only on what is implemented but also on:

- Guidance on whether tariffs stay, rise further, or are tied to negotiations

- Exemptions for key sectors (such as specific tech products), which can create sharp sector rotations[3]

- Signs of back-channel diplomacy or, conversely, hard-line rhetoric

3. Think in scenarios

Both discretionary and systematic traders can benefit from scenario planning:

- Further escalation: More tariffs, broader coverage, or new non-tariff barriers would likely deepen risk-off behavior, with further upside in safe havens and pressure on cyclicals.

- Freeze: Tariffs stay high but stabilize; markets may shift from panic to differentiation, rewarding companies and countries that can adapt supply chains.

- De-escalation: Any move toward rollbacks or a framework agreement could trigger a sharp relief rally in risk assets and a reversal of some safe-haven gains.

4. Use simulated environments to test strategies

In a period where policy shocks can move indices, FX, and commodities by several percent in hours, testing ideas in a risk-free, simulated environment can be especially valuable. Traders can:

- Backtest how their strategies behaved in past trade-war episodes

- Stress-test portfolios for further volatility spikes

- Experiment with hedging approaches (for example, using index futures, options, or FX pairs) before deploying capital

Key Takeaways For Traders

- Tariffs of 145% on Chinese goods and 125% on US exports represent an extreme escalation of the trade war, materially raising the cost of cross-border commerce.[3][8]

- The primary market response is a classic risk-off pattern: selling in equities, cyclical FX, and industrial commodities, and buying in government bonds, gold, yen, and Swiss franc.[1][4]

- Beyond immediate price moves, the bigger story is about growth expectations and confidence. If businesses cut back on investment and hiring due to trade uncertainty, the macro drag can be larger than the direct impact of tariffs.[5]

- Trading this environment demands agility: closely monitoring policy headlines, managing risk around volatility spikes, and staying clear on how your positions are exposed to global trade and growth.

For now, the balance of risks remains skewed toward further market turbulence rather than a quick resolution. Until there is a credible path to de-escalation, safe-haven flows are likely to remain a dominant theme – and traders will need to navigate a landscape where politics, not just economics, drives the tape.