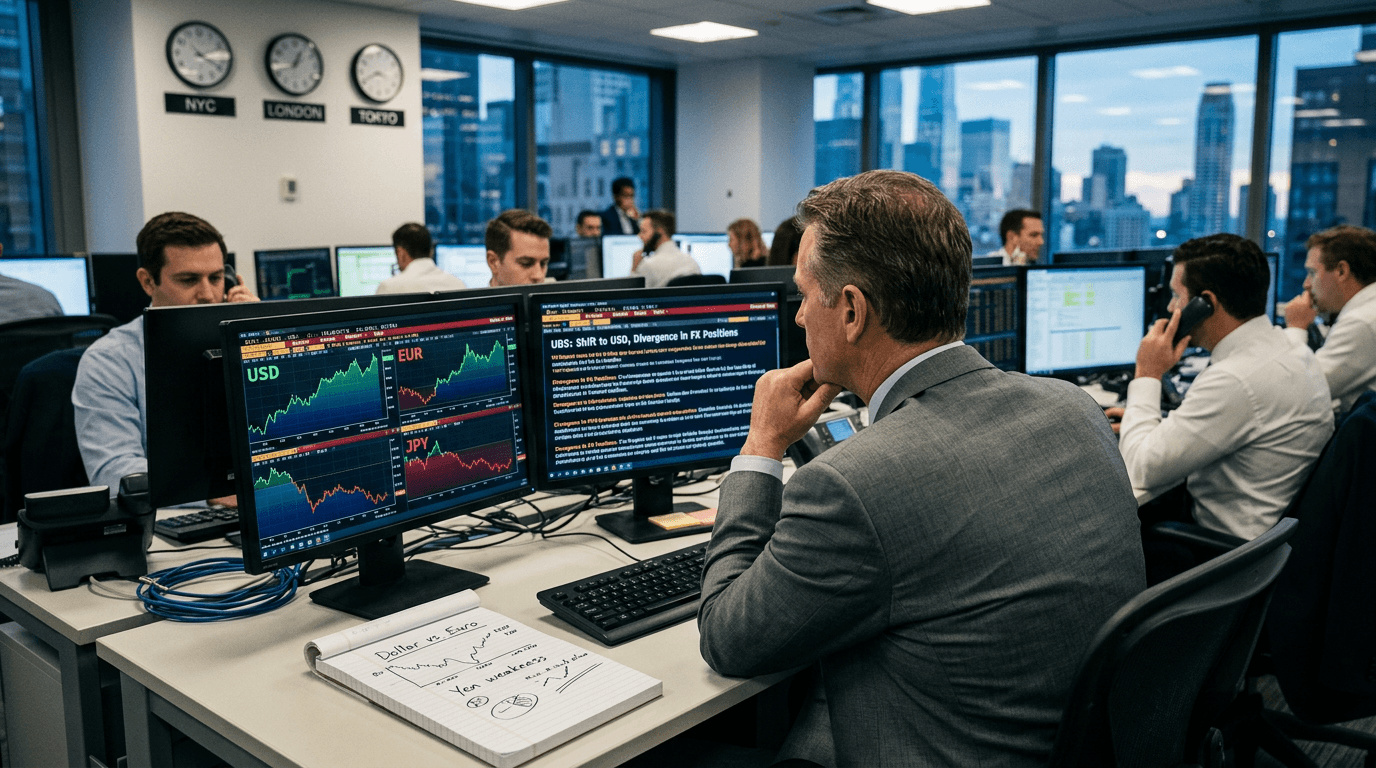

The latest shift in UBS’s currency outlook has put the US dollar back in the spotlight, with the bank turning more constructive on the greenback and expecting the euro and Japanese yen to weaken further. This is not just a headline for macro strategists—it’s a practical cue for traders recalibrating exposure in EUR/USD, USD/JPY and related futures as monetary policy and growth paths diverge across major economies.[4][8]

Why Ubs Is More Bullish On The Us Dollar

UBS’s Chief Investment Office has recently stressed that the near-term outlook for the US dollar is one of strength, helped by factors such as elevated energy prices and relative economic resilience in the US.[4][8] This view has supported a “stronger for longer” narrative, as the DXY dollar index has pushed to its highest levels since late 2022 in previous episodes of dollar strength.[8]

The core of this constructive stance lies in policy and growth divergence. While the Federal Reserve may be approaching a plateau or a cautious easing cycle, US rates remain relatively high versus much of the developed world, preserving the dollar’s yield advantage against low- or negative-rate currencies like the yen.[6][8] At the same time, US growth has generally outperformed that of the eurozone and Japan, reinforcing demand for dollar assets and supporting capital inflows that underpin the currency.

UBS still flags structural headwinds to the dollar over the longer term—such as twin deficits and the possibility of broader diversification away from USD holdings—but those are secondary to the bank’s near-term call that the dollar can remain firm as current macro conditions persist.[2][4] For traders, the key nuance is time horizon: the short- to medium-term setup currently favors a stronger dollar even if the multi-year picture becomes less supportive.

Pressure On The Euro And Yen

In contrast, UBS sees the euro and yen as more vulnerable, with further weakening likely as monetary policy and growth trajectories diverge from the US.[4] The euro area continues to wrestle with uneven growth and a more cautious European Central Bank, while inflation and output trends limit the scope for aggressive tightening that could meaningfully lift the currency’s carry appeal.[2]

Japan’s situation is even more extreme. The Bank of Japan’s long-standing ultra-easy stance has anchored yields near zero for years, leaving the yen as one of the lowest-yielding currencies in the G10.[6] Even gradual normalization, if and when it comes, may be too slow to offset the yield gap with US assets, especially if US rates stay elevated relative to historical norms. This makes the yen particularly sensitive to periods of global risk-on sentiment, when investors are willing to fund positions in higher-yielding currencies with cheap yen borrowing.

UBS’s more bullish dollar view therefore translates into a bias for weaker EUR/USD and higher USD/JPY—i.e., euro softness against the dollar and yen depreciation versus the greenback. For traders, that directional skew offers opportunities across spot, forwards and futures, but it also raises the importance of managing currency risk for portfolios with significant euro or yen exposure.[4]

How Traders Are Positioning Around The Call

The UBS shift has already influenced positioning in key FX pairs and related derivatives. Traders are increasing hedges against continued softness in European and Japanese currencies, using instruments such as EUR/USD and USD/JPY futures and options to protect underlying exposures or express directional views.[4][9]

In EUR/USD, a more constructive dollar outlook often leads to:

- Greater use of short euro hedges by investors holding euro-denominated assets but with dollar liabilities.

- Macro portfolios favoring dollar strength trades, such as being long USD against a basket of lower-yielding currencies, with the euro as a core short leg.

In USD/JPY, the logic is similar but amplified by yield differentials:

- Carry strategies that borrow in yen to buy higher-yielding assets can benefit if the yen weakens, but also require careful risk management in case of sudden yen spikes.

- Futures and options on USD/JPY are being used to hedge corporate or investor exposure to Japanese revenues and investments, protecting against currency translation losses if the yen continues to depreciate.

UBS’s broader guidance underscores the importance of currency risk management: aligning portfolio currencies with future liabilities and spending plans and considering hedges to avoid large FX swings undermining financial goals.[3][4] This is particularly relevant when a major house tilts more bullish on the world’s reserve currency, as it can reinforce existing trends and accelerate adjustments across global portfolios.

Implications For Simulated Finance And Active Learning

For traders using SimFi platforms like E8 Markets, a shift in a major institution’s FX outlook is a valuable learning opportunity rather than a binary “buy or sell” signal. UBS’s view provides a blueprint for how professional desks connect macro narratives to actual positioning decisions.[4][8]

In a simulated trading environment, you can:

- Test USD strength scenarios by running strategies that short EUR/USD or go long USD/JPY, with clearly defined risk limits.

- Explore the impact of different monetary policy paths—such as faster Fed easing or a surprise ECB tightening—on your trades and P&L over time.

- Practice hedging strategies by overlaying options or futures positions on top of virtual portfolios dominated by euro or yen assets.

Because there is no real capital at risk, you can experiment with both consensus trades (long USD vs EUR and JPY) and contrarian expressions (for example, fading the dollar at technical extremes) to understand how positioning, volatility and macro data interact. The goal is not merely to follow UBS’s call, but to learn how such calls are made, challenged and implemented in the real market.

Practical Takeaways For Traders

A few practical lessons emerge from UBS’s more bullish stance on the dollar:

1. Time horizon matters UBS sees near-term strength in the US dollar even while acknowledging structural headwinds over the longer term.[2][4] Traders should distinguish between tactical trades (weeks to months) and strategic currency allocations (years), and avoid mixing the two.

2. Diverging policy and growth drive FX trends Differences in interest rates, inflation and economic performance among the US, eurozone and Japan are central to the current outlook.[2][6][8] Keeping a close eye on central bank communication and data releases is essential for anticipating shifts in these divergences.

3. Hedging is not optional UBS repeatedly emphasizes managing currency risk by aligning exposures with liabilities and using hedging instruments where appropriate.[3][4] Whether in live or simulated markets, building the habit of measuring and hedging FX risk is critical to long-term success.

4. Scenario testing is a powerful tool SimFi platforms allow traders to run “what if” scenarios around policy surprises or growth shocks. This can clarify how sensitive positions in EUR/USD, USD/JPY and other pairs are to changes in the macro narrative, and help refine stop-loss and take-profit levels.

Conclusion: Navigating A Stronger Dollar Landscape

UBS’s turn toward a more bullish view on the US dollar, paired with expectations of further euro and yen weakness, highlights how quickly the FX landscape can shift when macro and policy signals align.[4][8] For traders and investors, the message is twofold: recognize the current dollar-friendly environment and its implications for EUR and JPY, but also respect the longer-term structural forces that may eventually challenge the greenback’s dominance.[2][4]

In practice, that means using the present trend as an opportunity to refine your approach to currency risk, test strategies in both live and simulated settings, and stay agile as new information emerges. A disciplined framework—anchored in macro analysis, clear risk management and continuous learning—will be far more valuable than any single directional call, even when it comes from a heavyweight like UBS.