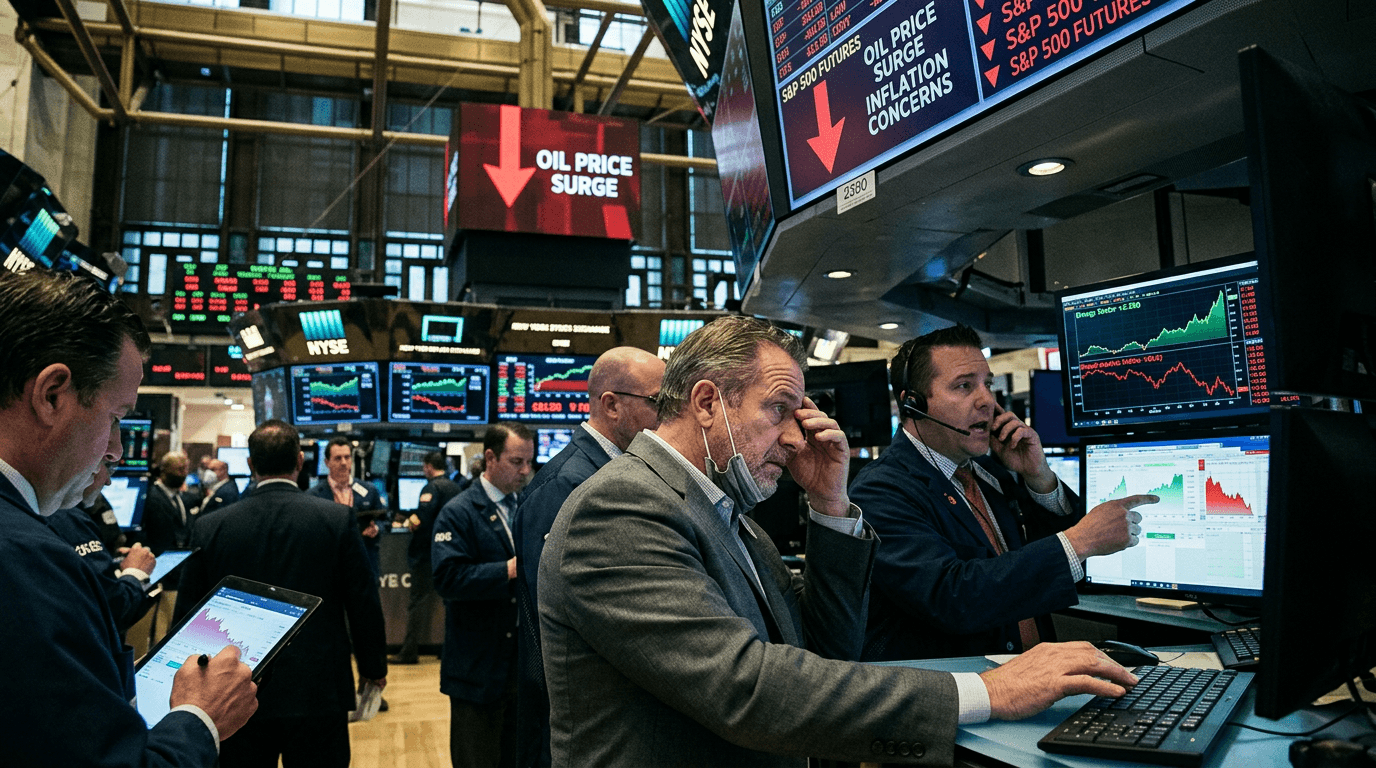

U.S. equity futures pointing lower is a reminder that markets are still uneasy about one thing: inflation that refuses to fade. With oil grinding higher again, traders are reassessing how long central banks might need to keep policy tight, and that shift in expectations is putting renewed pressure on risk assets from growth tech to cyclical stocks.

Market Backdrop: Oil, Inflation, And Futures

Index futures softening before the cash open typically signals a cautious tone rather than outright panic. In this case, the catalyst is a renewed climb in energy prices, which complicates hopes for a smooth disinflation path. When oil pushes higher, it feeds directly into headline inflation and, over time, can seep into core components through transportation, manufacturing, and consumer goods.

For traders, the key link is expectations. If higher oil is seen as temporary, markets can look through it. If it appears persistent—especially against a backdrop of still-firm wage growth—then futures markets start repricing the path of interest rates, and that repricing hits risk assets first.

Why Higher Energy Costs Rattle Risk Assets

Higher oil prices influence assets through multiple channels, and understanding those channels helps traders interpret futures moves more intelligently.

First, higher energy costs are a tax on consumers and businesses. Households spend more on fuel and utilities, leaving less discretionary income for other goods and services. Companies face higher input and transport costs, which compress margins unless they can pass those costs on—a challenge in a competitive environment.

Second, oil-driven inflation worries can push bond yields higher. If investors think inflation will be stickier, they demand higher compensation to hold longer-dated bonds. Higher yields raise the discount rate applied to future cash flows, which is particularly painful for long-duration assets such as high-growth tech stocks and speculative names with profits far in the future.

Third, lingering inflation uncertainty complicates central bank policy. Even if headline data has been trending lower, a fresh leg up in energy forces policymakers to be more cautious about signaling rate cuts. Futures markets for interest rates then adjust, often pricing fewer or later cuts. Equities, especially riskier segments, tend to reprice quickly in response.

In short, when traders see oil rising and inflation fears rekindling, the default reaction is to scale back risk until the macro picture becomes clearer.

Sector And Style Impact: Winners And Losers

When U.S. futures soften on inflation worries, the reaction under the surface matters as much as the headline index move. Different sectors and styles respond very differently to higher oil and shifting rate expectations.

Cyclicals and growth-sensitive sectors like consumer discretionary, industrials, and small caps often feel the most pressure. These areas rely heavily on robust economic activity and consumer spending. If investors worry that higher energy costs will squeeze households and erode margins, they tend to cut exposure here first.

High-growth technology and richly valued “story” stocks can also struggle. Their cash flows are weighted further into the future, so they are more sensitive to changes in bond yields and discount rates. When inflation worries spark a move higher in real yields, price-to-earnings and price-to-sales multiples can compress quickly.

On the other side, certain pockets of the market may benefit or at least hold up better. Energy producers and oilfield services companies can see improved revenue and profit outlooks when crude prices climb. Traditional value sectors with strong balance sheets and steady cash flows—such as some parts of utilities, healthcare, or consumer staples—often act as relative havens in inflation scares.

For traders, this means that a “soft” futures tape rarely affects everything equally. Rotations between styles (growth vs. value) and sectors (energy vs. consumer) can be as important as the overall index move.

How Active Traders Can Navigate This Backdrop

In a market environment where oil and inflation fears are driving the tone, risk management and scenario planning become central to a trading playbook.

First, recognize that macro headlines can drive short-term volatility beyond what fundamentals alone would suggest. Position sizing should reflect that elevated headline risk. Smaller position sizes and wider, pre-defined stop levels can help traders stay in the game when intraday swings increase.

Second, pay attention to cross-asset signals. Bond yields, breakeven inflation rates, and the U.S. dollar often move in tandem with equity futures when inflation worries resurface. For example, rising yields alongside softer futures typically confirms a “higher-for-longer” rates narrative, reinforcing pressure on long-duration equities. If yields don’t confirm the move, the equity reaction may be more sentiment-driven and potentially short-lived.

Third, use simulated environments or paper trading to test your responses to macro shocks. Practice how your strategy behaves when futures gap lower, volatility spikes, or correlations change—for instance, when stocks and bonds both sell off. This kind of rehearsal can build confidence and discipline when the real market delivers similar conditions.

Fourth, consider diversification beyond a narrow set of risk assets. While chasing the hottest sector can be tempting, a mix that includes defensive names, quality balance sheets, and possibly commodity-exposed plays can reduce portfolio sensitivity to any single macro driver.

Finally, adapt your time frame to the environment. When macro uncertainty is heightened, short-term trades based on intraday levels and clear technical setups may offer better risk-reward than large directional bets on the index over several weeks. Swing traders can still participate, but they should anchor entries and exits to well-defined support and resistance zones, not just headlines.

What To Watch Next

When futures soften on oil and inflation worries, the next phase depends on whether data and policy communications validate those concerns.

Key economic releases such as inflation prints, consumer sentiment, and spending data will show whether higher energy costs are beginning to bite. Corporate earnings calls can reveal if companies are experiencing margin pressure from fuel and transport costs, or if they are successfully passing them through to customers.

Central bank commentary is equally important. Traders will scrutinize any shift in language around inflation risks and the timing of potential rate cuts. A more hawkish tone can reinforce the risk-off mood, while reassurance that policymakers still see progress on inflation can calm markets even if oil remains elevated.

For now, softer U.S. futures signal that investors are unwilling to aggressively add risk until the trade-off between growth and inflation looks more favorable. By understanding how energy prices feed into inflation expectations, interest rates, sector performance, and positioning, traders can move from reacting emotionally to acting strategically.