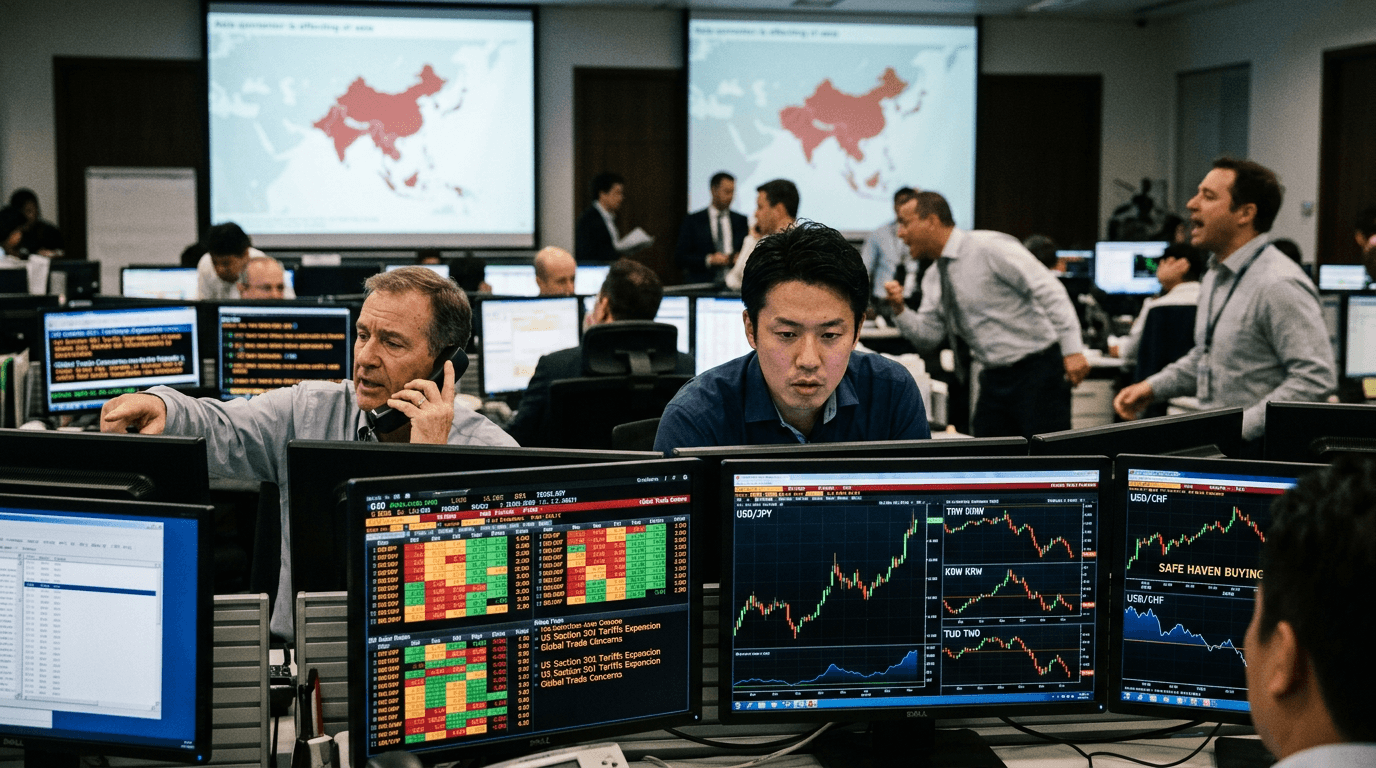

The latest US announcement of broad new Section 301 tariffs marks a clear escalation in trade frictions – not only with China, but with a wider group of major Asian exporters. Markets are treating it as a risk-off shock: higher policy uncertainty, potential supply chain disruption, and another nudge toward fragmentation of global trade. For traders, this is exactly the kind of structural policy shift that can reshape FX, equities, and commodities over the coming months, not just over the next few sessions.

What Section 301 Tariffs Actually Are

Section 301 is a provision of the US Trade Act of 1974 that gives the US administration authority to investigate and respond to what it views as unfair foreign trade practices, including discrimination against US companies, intellectual property violations, or market access barriers.[7] In practice, its most high-profile use has been against China.

Beginning in 2018, the US used Section 301 to levy additional tariffs of generally 7.5%–25% on hundreds of billions of dollars of Chinese imports across multiple product “lists,” ultimately covering roughly two-thirds of US imports from China.[3][6] These measures targeted a wide range of goods from intermediate components to finished consumer products, and they remain largely in place today.[3][6]

More recently, the US Trade Representative (USTR) has shifted from broad-based lists to more targeted hikes in strategic sectors. In 2024, the USTR finalized significant Section 301 increases on selected Chinese imports such as electric vehicles, batteries, solar cells, critical minerals, steel and aluminum, and key medical products, with tariff rates on some of these items jumping to 25%–100% over 2024–2026.[1] This shows a clear pattern: Section 301 has evolved into a tool for industrial and national security policy as much as pure trade enforcement.

Today’s announcement of new tariffs of at least 10% on imports from around 60 countries, with 12.5% rates for China, India, Japan and others, extends that logic beyond China alone. Instead of being a bilateral US–China issue, Section 301 is now being used as a broad lever on global supply chains and major Asian exporters.

Why This Round Is Different

Traders should focus on three features of this announcement.

First, the geographic scope is much wider. Previous Section 301 actions were heavily China-centric.[3][6] While China is still in the crosshairs, the inclusion of other large Asian exporters broadens the impact to regional supply chains in electronics, autos, and industrial machinery, where production is often spread across multiple countries.

Second, the breadth of coverage means the tariffs function more like a generalized tax on imported inputs, not just a targeted penalty. Even a “modest” 10–12.5% rate can meaningfully alter cost structures and pricing when applied across a wide swath of trade partners. For firms operating on thin margins, that can be enough to trigger price increases, margin compression, or re-sourcing decisions.

Third, these tariffs sit on top of an existing structure that is already tight. Chinese imports are already subject to substantial additional duties from earlier Section 301 rounds and the more recent hikes in strategic sectors.[1][3][6] Adding extra layers raises the risk that some supply chains – particularly in EVs, semiconductors, and clean energy technology – become more fragmented and regionally siloed over time.[1]

For markets, this is less about immediate trade volumes and more about signaling: the US is willing to accept higher trade costs and friction to pursue strategic and political objectives. That tends to increase risk premia and volatility.

Fx And Market Reaction: Why Usd And Jpy Benefit

The initial reaction has followed a classic risk-off template: investors move out of risk-sensitive assets and into perceived safe havens.

Policy uncertainty and the risk of retaliatory measures – especially from China, which has previously responded quickly to US tariff actions[8] – typically drive a rotation into the US dollar. The USD benefits both from its safe-haven status and from the idea that US assets may be somewhat more insulated by the size and diversity of the domestic economy.

The Japanese yen also tends to gain in episodes where global trade tensions rise. Japan is an export-oriented economy, but the JPY historically trades as a funding and safe-haven currency: when risk sentiment deteriorates, investors often unwind carry trades funded in JPY, pushing the currency higher.

On the other side, risk-sensitive currencies like the Australian and New Zealand dollars, as well as Asian export-oriented FX such as the Korean won and Taiwan dollar, can come under pressure. Their economies are deeply integrated into the electronics, autos, and commodity supply chains that stand to be affected by higher tariffs and slower trade growth.

Equity markets, especially futures, have reacted negatively, with particular vulnerability in sectors linked to global manufacturing, semiconductors, autos, and industrials. These sectors face both potential margin pressure (from higher input costs) and demand uncertainty (if retaliatory tariffs or slower global growth materialize).

An important nuance for macro traders: tariffs are both inflationary and growth-negative. They can raise import prices and production costs, while simultaneously weighing on trade volumes and confidence. That mix can complicate the path for central banks. In the US, if tariffs meaningfully lift import prices, they could slow the pace of disinflation, potentially affecting expectations for rate cuts – even as growth headwinds strengthen.

How Traders Can Navigate This Tariff Shock

For traders in both live and simulated environments, this announcement is a chance to practice navigating complex, multi-asset macro events.

First, map the channels of impact. Identify which economies are most exposed to US demand and global manufacturing trade, especially in sectors targeted historically under Section 301 like electronics, machinery, autos, EVs, batteries, and solar.[1][3][6] Currencies and indices tied to these themes are more likely to show sustained sensitivity.

Second, distinguish between knee-jerk and structural moves. Initial price action is often dominated by positioning and headline algorithms. Over the following days and weeks, markets tend to re-price based on more careful assessments of sector-level exposure, corporate guidance, and any sign of retaliation. Simulated trading is a good environment to test scenarios: a quick fade of the initial move versus a more persistent repricing of risk premia.

Third, monitor policy follow-through. Section 301 actions go through defined processes, including announcements, comment periods, and implementation dates, with opportunities for exclusions and adjustments.[1][3][4] Traders who track the official timeline and any carve-outs for specific products or countries can anticipate when the narrative might soften or harden.

Fourth, consider hedging and relative-value strategies. For example, traders might explore:

- Long USD or JPY versus a basket of trade-sensitive currencies during periods of escalating rhetoric and uncertainty.

- Relative trades within equities, favoring domestically focused sectors over export-heavy, cyclical industrials when tariff risks are front and center.

- Event-driven volatility strategies around key dates such as USTR hearings, implementation deadlines, or expected Chinese policy responses.[1][2][4][8]

Finally, keep an eye on the broader macro backdrop. Tariffs are one piece of a larger puzzle that includes central bank policy, fiscal dynamics, and the evolving architecture of global trade. Section 301 has already driven a multiyear reshaping of US–China economic ties.[1][3][6] A broader expansion to other Asian exporters could amplify trends toward “friend-shoring” and regional blocs.

For traders, that means this news is not just about the next week’s FX or equity moves. It is about understanding a structural shift in how the world’s largest economy engages with its trading partners – and positioning portfolios for a world where trade policy shocks may become more frequent, more targeted, and more consequential for cross-asset pricing.