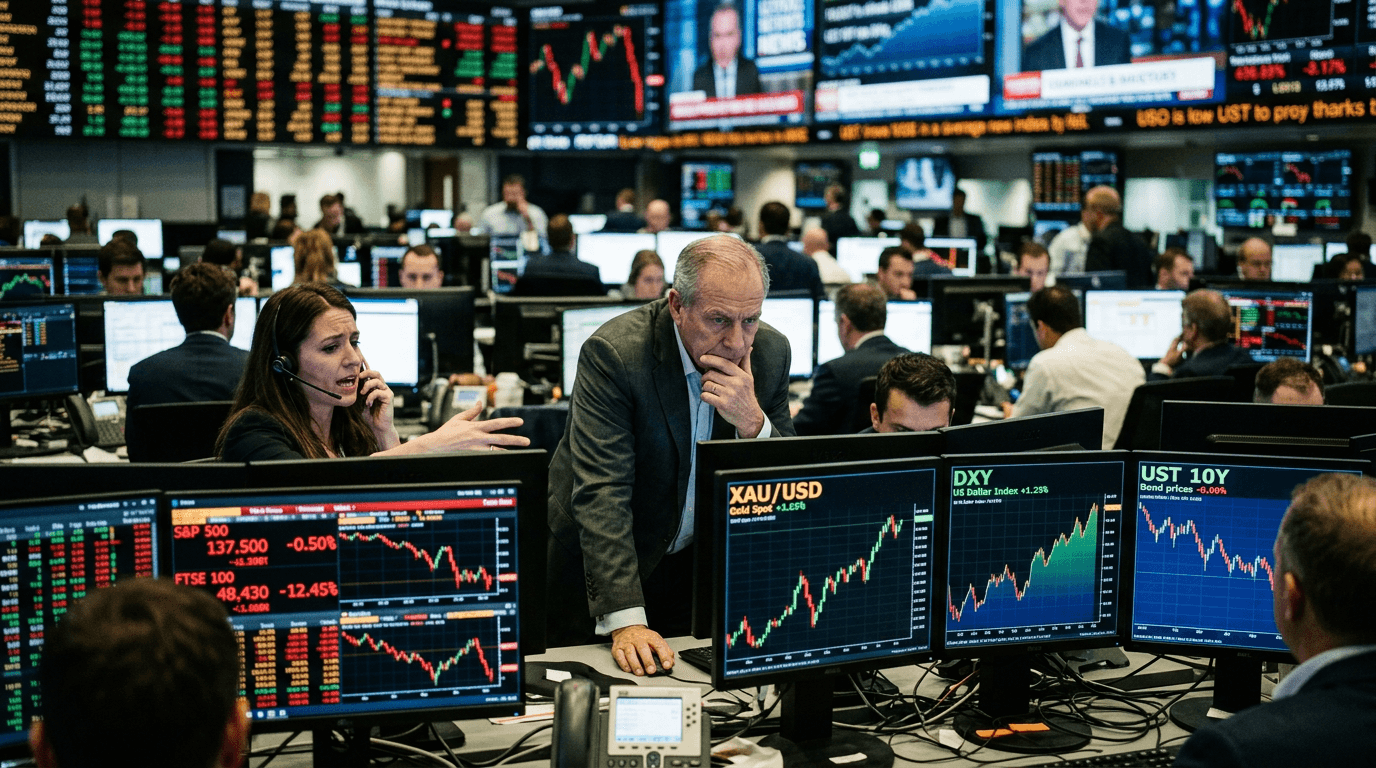

Global equity markets are back under pressure as investors react to headlines about an entrenched Middle East conflict and persistent inflation. The tone has clearly shifted toward risk-off, with major indices and cyclical sectors underperforming while volatility picks up. Yet the pattern of safe-haven flows is less straightforward than in past stress episodes: instead of rushing uniformly into gold, investors are favoring the US dollar and short-duration dollar assets, leaving bullion to trade more like a leveraged macro asset than a pure crisis hedge.

Markets Snap Into Risk-off Mode

The latest leg lower in equities is being driven by a familiar combination: geopolitical escalation, concern that energy prices will stay elevated, and a realization that central banks may not be able to ease as quickly as markets had hoped.

Futures on major indices are showing higher implied volatility and a clear downside skew, signaling strong demand for put protection and tail hedges. This is consistent with traditional risk-off behavior: investors trim equity exposure, rotate out of high-beta sectors such as technology and consumer discretionary, and pay up for downside insurance.

Credit markets are beginning to reflect the stress as well. Spreads on high-yield and lower-tier investment-grade bonds have started to widen from recent tights, even if we are not yet seeing disorderly price action. The picture is one of de-risking rather than outright panic: risk assets are being repriced to reflect a world of slower growth, higher geopolitical risk premia, and “higher for longer” real interest rates.

Why Gold Isn't Behaving Like A Classic Haven

One of the more notable features of this selloff is that gold is not delivering the textbook safe-haven response. Historically, sharp spikes in geopolitical tension and equity volatility have triggered abrupt rallies in bullion as investors sought insurance against both financial and geopolitical shocks.

Today, however, gold is trading in what many analysts describe as a “macro-beta” regime. After reaching a peak near late January, prices have since retreated by several hundred dollars, behaving more like a crowded, liquid risk position being unwound than a shelter of last resort.

A key headwind is the level of real interest rates. The 10-year US Treasury yield is around the mid-4% area, while the 10-year inflation-adjusted (real) yield is hovering near 2%. Those are punitive levels for a non-yielding asset like gold, because holding bullion entails a meaningful opportunity cost versus simply sitting in Treasuries or dollar cash and collecting carry.

Market structure matters as well. Gold’s investor base is far more financialized than in previous cycles. The World Gold Council estimates that total gold demand in 2025 exceeded 5,000 tonnes, with investment demand alone rising to more than 2,100 tonnes. Exchange-traded funds (ETFs) contributed heavily to that number, with US-listed gold ETFs adding well over 400 tonnes and pushing their total holdings above 2,000 tonnes.

When such a large share of demand is driven by ETF and speculative flows, gold trades more like a portfolio asset sensitive to macro narratives—real yields, dollar direction, risk sentiment—than a pure fear barometer. In an environment where real yields stay elevated and the dollar is firm, even heightened geopolitical risk is not enough to guarantee a sustained bid for bullion.

THE DOLLAR’S SAFE-HAVEN EDGE

While gold’s response has been muted and choppy, the US dollar has resumed its role as the primary safe-haven of choice. A broad dollar index has risen several percent from pre-conflict levels, reflecting strong demand for dollar liquidity from global investors, corporates, and reserve managers.

There are both cyclical and structural reasons for this. Cyclically, the US economy continues to outperform many developed peers, reinforcing expectations that US policy rates will stay higher for longer. That rate advantage, particularly when adjusted for inflation, makes dollar assets relatively attractive.

Structurally, the dollar remains the world’s dominant funding and reserve currency. During periods of stress, global institutions seek the deepest, most liquid markets they can access. US Treasuries and dollar cash markets provide that depth, which is why stress capital often migrates there before considering alternatives like gold or the Japanese yen.

The result is that some flows that, in earlier crises, might have gone directly into bullion are instead showing up as demand for Treasuries, T-bills, and money-market funds. In other words, the safe-haven bid is real—but it is being intermediated through the dollar system rather than through gold bars and coins.

Diverging Flows Across Safe-havens

This divergence is reshaping the defensive playbook. Instead of a synchronized rally across gold, the dollar, and traditional havens like the Swiss franc, we are seeing a more differentiated picture:

- The dollar is supported by yield, growth, and liquidity.

- Gold is supported by longer-term structural demand—central-bank buying, reserve diversification, and ETF holdings—but capped in the short term by real yields and a strong dollar.

- Sovereign bonds are caught between their role as a defensive asset and the risk that inflation proves sticky, limiting central banks’ ability to cut.

This is consistent with the broader shift observed over the past few years. In a world of high liquidity and momentum, assets like US equities and gold can rise together when markets price in lower real rates and a weaker dollar. When that narrative reverses—because inflation is sticky, or because conflict pressures energy prices and keeps yields elevated—both can sell off together, while the dollar outperforms.

For investors, the key takeaway is that “safe haven” is no longer a one-size-fits-all label. Each defensive asset has a different sensitivity to real rates, growth expectations, and liquidity conditions. Understanding those sensitivities is more important than ever.

Implications For Hedging And Portfolios

The changing pattern of safe-haven flows has practical consequences for risk management.

First, relying on gold alone as a crisis hedge is less effective when the main driver of market stress is higher real yields and a stronger dollar. In that regime, bullion can lag other hedges or even move in the same direction as risk assets.

Second, a more robust defensive toolkit tends to combine several elements: • Dollar exposure, particularly versus more cyclical or higher-inflation currencies. • Duration exposure via high-quality government bonds, while being mindful of inflation and central-bank signals. • Select gold allocation to benefit from structural demand and tail-risk hedging, but with realistic expectations about its behavior when real yields are rising. • Volatility strategies, such as equity index puts or variance exposure, to benefit directly from spikes in implied volatility.

Third, time horizon matters. In the near term, the balance between real yields and the dollar will likely dominate gold’s performance. Over the medium term, ongoing central-bank buying, ETF participation, and geopolitical fragmentation still provide a strong underpinning for the metal as a store of value and diversification tool.

What Traders Should Watch Next

Several indicators will help determine whether this risk-off phase deepens or stabilizes—and how the tug-of-war between gold and the dollar evolves:

- Real yields: A sustained drop in 10-year real yields below the recent 2% area would materially improve gold’s relative appeal versus Treasuries.

- Dollar “fatigue”: If incoming data or policy communication suggests the US rate advantage is peaking, dollar strength could plateau, allowing bullion to regain some crisis premium.

- Volatility term structure: The shape of the VIX futures curve and skew in index options will reveal whether markets are pricing a short, sharp shock or a more prolonged period of stress.

- Energy prices: Persistent elevated oil prices tighten financial conditions and can reinforce the “higher for longer” narrative, which tends to favor the dollar over gold.

- Geopolitical headlines: Any clear path toward de-escalation in the Middle East could relieve some near-term pressure on risk assets, even if the underlying inflation story remains challenging.

Conclusion

The latest bout of risk aversion is a reminder that not all crises look the same—and neither do all safe-haven trades. Equities and other risk assets are clearly adjusting to a more uncertain geopolitical and inflation backdrop, but the traditional hierarchy of defensive assets has been reordered. With real yields elevated and the dollar firmly in demand, gold is acting less like an automatic crisis hedge and more like a macro-sensitive portfolio asset.

For investors and traders, the message is clear: build hedges around the drivers of risk, not just the headlines. That means monitoring real yields, dollar dynamics, and volatility as closely as you track geopolitical developments—and constructing diversified defensive positions that can work across more than one scenario.