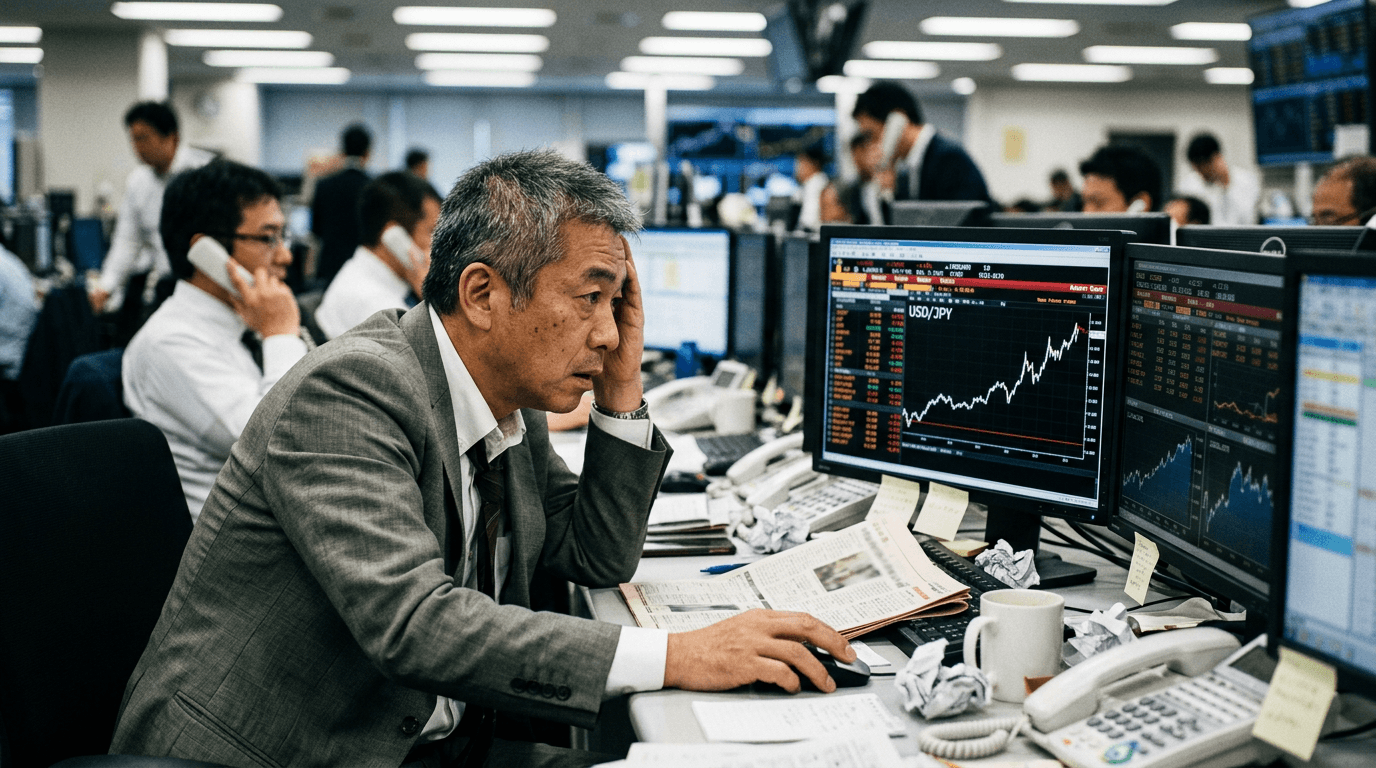

The Japanese yen’s latest slide against the US dollar is more than just another currency headline—it marks a critical moment in global FX markets. USD/JPY has pushed into levels last seen in the mid‑1980s, with spot trading around 162 per dollar, the weakest yen in roughly 40 years[1][5]. That puts the pair squarely in the zone where traders suspect Japan’s Ministry of Finance (MoF) and the Bank of Japan (BoJ) may step in, elevating both volatility and intervention risk across FX markets[1][2][3].

WHAT’S HAPPENING TO THE YEN?

In recent sessions, the yen has broken decisively through the 160 level and continued weakening toward 162 per dollar, testing prices not seen since 1986[1][5]. Market data show USD/JPY touching around 161.9–162.3, confirming a new multi‑decade low for the currency[1][2][5].

This move is not occurring in isolation. The yen’s decline is contributing to broader dollar strength against Asian currencies, as investors reassess interest rate expectations and relative growth prospects[4]. FX traders are increasingly pricing in larger intraday swings in USD/JPY, with option markets reflecting heightened expectations of either a sharp intervention‑driven reversal or an extended trend move higher[2][3].

For Japanese assets, a structurally weaker currency has been a double‑edged sword. On one hand, a cheap yen has supported export‑oriented companies and helped fuel gains in Japanese equity benchmarks, including the Nikkei, over the past year. On the other, extreme FX moves can destabilize futures markets and risk sentiment if investors begin to fear disorderly currency adjustments rather than gradual depreciation.

Why The Yen Is Under So Much Pressure

The primary driver of the yen’s weakness is the wide and persistent interest rate gap between Japan and the United States[4]. The Federal Reserve has been lifting rates aggressively since 2022 in response to elevated inflation, keeping US yields high and the dollar supported[4]. In contrast, the BoJ has only recently begun to exit ultra‑loose policy, and even after hiking its benchmark rate to around 1%, Japanese interest rates remain far below US levels[2][4].

This divergence encourages classic carry trades: borrowing in low‑yielding yen and investing in higher‑yielding dollar assets or other currencies. As more investors run these strategies, they sell yen and buy foreign assets, adding sustained downward pressure on the currency[4]. The more entrenched the rate differential appears, the more confident markets become in holding short‑yen positions, which is why the currency can slide steadily for months without a meaningful reversal.

Domestic policy dynamics add another layer. The Japanese government has signaled it prefers “appropriate” monetary management, language many analysts interpret as an attempt to discourage the BoJ from tightening too aggressively and choking off growth[2]. That makes rapid rate hikes less likely, even as inflation and wage dynamics slowly improve, leaving FX markets to conclude that interest rate support for the yen will arrive later and more gradually than in other major economies[2][4].

Intervention Fears: What Traders Are Watching

Japan has already demonstrated a willingness to defend the yen when moves are viewed as excessive or speculative. Authorities previously spent a record 11.73 trillion yen—over $70 billion—intervening in FX markets between late April and late May after USD/JPY broke above 160[2]. That episode reminded traders that while fundamental forces point to a weaker yen, officials are prepared to act to slow the pace of depreciation.

The current move toward the mid‑160s is therefore being read as a direct challenge to policymakers. Market participants broadly assume that the region around 160–162 represents a “suspected intervention zone,” where sudden, large official dollar‑selling operations could be launched[2][3]. Comments from Japanese officials have emphasized their readiness to respond to “excessive” moves, further reinforcing the sense that intervention risk is live whenever USD/JPY grinds higher[1][2].

For active traders, this creates a distinctly asymmetric risk profile. Trend‑following strategies that stay long USD/JPY are fundamentally supported by rate differentials, but they face the constant overhang of a surprise multi‑yen intraday reversal triggered by official action. That is why FX options prices, especially short‑dated USD/JPY volatility, tend to rise as spot approaches these historically sensitive levels[2][3].

How This Shapes Global Markets And Risk Sentiment

A structurally weak yen affects multiple asset classes. In equities, Japanese exporters benefit from currency translation gains, but foreign investors must weigh those earnings tailwinds against FX risk on unhedged positions. In futures markets, sharp yen moves can spill into Nikkei contracts as participants re‑price earnings, hedging costs, and the odds of policy shifts.

Across Asia, dollar strength driven partly by yen weakness can pressure other regional currencies, particularly those with significant external funding needs or large import bills. As the dollar appreciates, local central banks may be forced to decide whether to defend their currencies with reserves, adjust rate policy, or allow gradual depreciation and focus on domestic objectives. That interplay often manifests in higher FX volatility and, at times, a more cautious stance toward risk assets.

Global risk sentiment can turn quickly if traders start to view yen moves as a signal of broader instability rather than a contained carry trade story. A sudden, large‑scale intervention, for example, may trigger sharp position unwinds across leveraged FX and rates strategies, creating short‑term turbulence even if the longer‑term trend remains intact.

Practical Takeaways For Traders And Simulated Finance Users

For traders and those using simulated finance platforms to build skills, the current USD/JPY environment offers several practical lessons:

First, understand that extreme levels in major pairs are often accompanied by elevated policy risk. When a currency hits a 40‑year low, fundamental analysis must be combined with close monitoring of official communication, intervention history, and market microstructure indicators like options pricing and liquidity conditions[1][2][3].

Second, recognize that carry trades are powerful but not risk‑free. Funding positions in a low‑yielding currency such as the yen can be profitable for long stretches, yet they are inherently exposed to sudden policy shocks. Simulated environments are ideal for testing how different position sizes, stop‑loss strategies, and hedging techniques perform under scenarios where authorities step in unexpectedly.

Third, think in terms of scenarios rather than single forecasts. One plausible path is continued yen weakness if rate differentials stay wide and interventions remain sporadic and limited in scale. Another is a sharp, intervention‑driven correction, especially if global conditions shift or domestic pressures grow. Building and stress‑testing strategies across multiple outcomes helps avoid over‑reliance on a single narrative.

Finally, remember that FX moves are deeply interconnected with broader macro themes—inflation, growth, central bank policy, and global risk appetite. Traders who link currency trends to these drivers can better anticipate when a “routine” depreciation story might evolve into a more market‑moving event requiring rapid adjustment of positions and risk limits.