The Japanese yen’s slide to a new 40‑year low against the US dollar has turned a long‑running currency story into a live risk event, with Tokyo openly signaling it is ready to step in if markets become “disorderly” and traders ramping up bets on intervention-driven volatility.[1][2][4] For anyone involved in FX, yen futures, or JPY crosses, this is no longer background noise—it’s a regime-defining moment.

MARKET SNAPSHOT: A 40‑YEAR LOW IN THE YEN

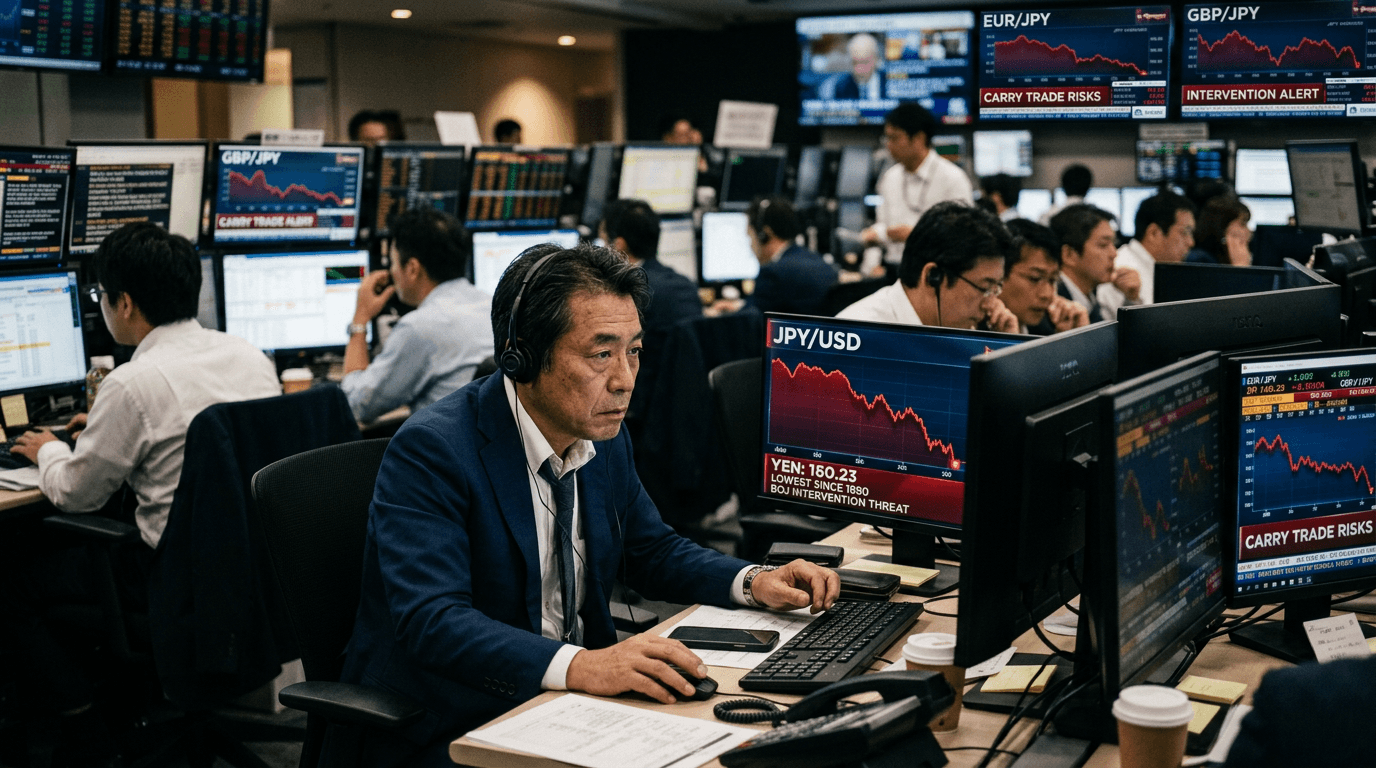

The yen has fallen below 162 per dollar, touching levels not seen since 1986 and marking its weakest point in four decades.[1][2][5] This move extends a multi‑year decline in the currency and underlines that previous efforts to stabilize the yen have not reversed the broader trend.[4][8]

Earlier this year, Japanese authorities intervened when the currency broke past the 160 level, spending a record 11.73 trillion yen—around $72.5 billion—between late April and late May to support the exchange rate.[2][4] Despite the size of that operation, the yen’s relief rally was short‑lived, and the currency is now trading even weaker than before those actions.[4]

Japan’s Finance Minister Satsuki Katayama has reiterated that the government stands ready to take “bold action” against excessive speculative moves, emphasizing that Tokyo is in close contact with US counterparts and that both sides are “aligned” on potential steps in foreign exchange markets.[2][3] This combination of public signaling and behind‑the‑scenes coordination is classic pre‑intervention “verbal guidance,” designed to warn speculators that the authorities are watching closely.[3][5]

Adding another twist, the Bank of Japan (BoJ) has already moved away from the zero‑rate environment that defined Japanese policy for decades, raising its benchmark interest rate to 1% in mid‑June—the highest level since 1995.[2] Even with that change, however, the yen continues to struggle, highlighting how dominant other forces have become.

Why The Yen Is So Weak

At the core of the yen’s weakness is the interest rate gap between Japan and the United States.[2][4] US rates are still high as the Federal Reserve focuses on inflation pressures that have been intensified by an oil shock linked to the US‑Israeli war with Iran.[4] Traders expect the Fed to keep rates elevated, or even consider further increases, which supports the dollar and makes yen funding particularly attractive for carry trades.[4]

In contrast, Japan’s rate policy remains relatively cautious. Although the BoJ has lifted its benchmark rate, it is still far below US levels, and the Japanese government is signaling in its basic policy guidelines that it prefers “appropriate” monetary management—a phrase many market participants read as a subtle push against further aggressive tightening.[2] In effect, policymakers want to stabilize the currency without choking off domestic growth and adding stress to Japan’s heavily indebted public sector.

There are also structural elements behind the yen’s long decline. Over the past five years, the yen has lost roughly half its value against the dollar, reflecting not only interest rate differentials but also Japan’s persistent fiscal deficits and aging demographics, which complicate the path to stronger, sustained growth.[8] These deep‑seated factors make it difficult for one‑off interventions to deliver lasting strength in the currency.

When global risk aversion rises, the yen can still behave like a safe haven. But in the current environment—marked by high US yields, geopolitical tensions, and an oil‑driven inflation shock—the traditional “flight to yen” dynamic is being overshadowed by the sheer income advantage of dollar assets.[4] That leaves the yen vulnerable whenever markets are focused on relative yield rather than pure risk sentiment.

TOKYO’S TOOLKIT: FROM VERBAL TO DIRECT INTERVENTION

Japan’s immediate levers are well known to FX traders. The first line of defense is verbal intervention: explicit statements from the finance ministry warning of “excessive” moves, talk of “bold action,” and repeated references to monitoring markets closely.[2][3][5] This is designed to cool speculative activity without committing real capital.

If that fails, authorities can move to direct intervention—selling US dollars or dollar‑denominated assets, such as US Treasuries, and using the proceeds to buy yen.[4] This was exactly the approach taken earlier this year, when Japan sold around $70 billion of assets to prop up the currency.[4] The result was a short‑term spike higher in the yen but no decisive change in the longer‑term trend.[4]

Intervention is more effective when coordinated, which is why Katayama’s emphasis on alignment with US policy matters.[2][3] Japan needs Washington’s tacit approval to avoid diplomatic frictions, and joint signaling can increase the psychological impact on markets even if the flows themselves are one‑sided.

However, direct intervention has limits. Japan’s foreign reserves are large but not infinite, and repeated operations can trigger questions about sustainability and policy credibility. More importantly, intervention does not alter the underlying rate differential or structural drivers; it mainly aims to smooth volatility, prevent disorderly moves, and push back against speculative overshoots.

Market Ripple Effects And Volatility Risk

Any credible threat of intervention—and especially an actual operation—is a volatility event for yen futures and JPY crosses. Short‑yen positioning can be forced to unwind rapidly if authorities step in aggressively, leading to sharp intraday reversals and squeezes in popular trades such as USD/JPY, EUR/JPY, and AUD/JPY.[4][5]

Intervention also has cross‑asset implications. A meaningful jump in the yen would put downward pressure on the dollar and could affect US Treasuries, particularly if Japan sells fewer bonds or even reduces holdings as part of its currency operations.[4] Equity markets are not immune either: a stronger yen tends to be a headwind for Japanese exporters, while a weaker yen supports their overseas earnings but raises import costs.

For global portfolios, the yen’s slide is a reminder that FX risk can be as important as price risk in stocks or bonds. The potential for rapid, policy‑driven moves means traders and investors should be cautious about leverage, stop‑loss placement, and concentration in yen‑funded strategies, especially when official rhetoric turns more forceful.[2][3][5]

Trading And Simulated Markets: Practical Takeaways

For traders in both live and simulated environments, the current yen episode offers several practical lessons.

First, price levels matter. The 160–162 band has clearly become a political threshold, with Japan stepping in after the first break and now signaling readiness to act again as new multi‑decade lows are tested.[2][4] When policy‑sensitive levels are approached, normal technical setups can be overshadowed by headline risk.

Second, policy communication is a trading input, not just background noise. Statements from the finance ministry, BoJ commentary, and reports of contact with US officials are part of the information set, and they can shift probabilities for intervention almost as quickly as economic data releases.[2][3][4] Building a process to track and interpret these signals is essential.

Third, event risk favors flexible positioning. Ahead of potential intervention, reducing leverage in yen‑linked trades, shortening holding periods, or using options to express views on volatility rather than direction can make sense. Strategies like straddles around known policy windows, or mean‑reversion setups that assume intervention will cap extreme moves, are often explored by more advanced traders.

For SimFi participants, this environment is an ideal test bed for scenario analysis: What happens to a carry portfolio if USD/JPY drops 5% in a day on surprise intervention? How do JPY crosses behave when implied volatility spikes? Practicing these situations in a simulated framework can improve readiness for real‑world dislocations without capital at risk.

Conclusion: A Currency At The Center Of Global Flows

The yen’s fall to a 40‑year low is more than a chart milestone—it is a live expression of the global tug‑of‑war between high US rates, Japan’s cautious normalization, geopolitical shocks, and entrenched structural forces.[1][2][4] Tokyo’s growing readiness to intervene adds a layer of policy uncertainty that will keep the currency, and associated futures and crosses, front and center for macro‑driven traders.

Going forward, the key is less about predicting the exact timing of intervention and more about understanding the economic logic behind it, the political thresholds involved, and the way such actions transmit across FX and broader markets. In that sense, the yen is not just a currency pair; it is a barometer of the global financial cycle—and right now, it is flashing that the cycle remains firmly tilted in favor of the dollar.