Brazil’s latest inflation projections sent a clear message to markets: price pressures are likely to stay uncomfortably high through 2027, but the central bank still expects inflation to converge close to target by 2028[1][7]. For traders, that nuanced path matters as much as any single rate decision, because it reshapes expectations for the Selic rate, BRL FX, local rates futures, and broader EM carry strategies.

CENTRAL BANK’S NEW INFLATION PATH

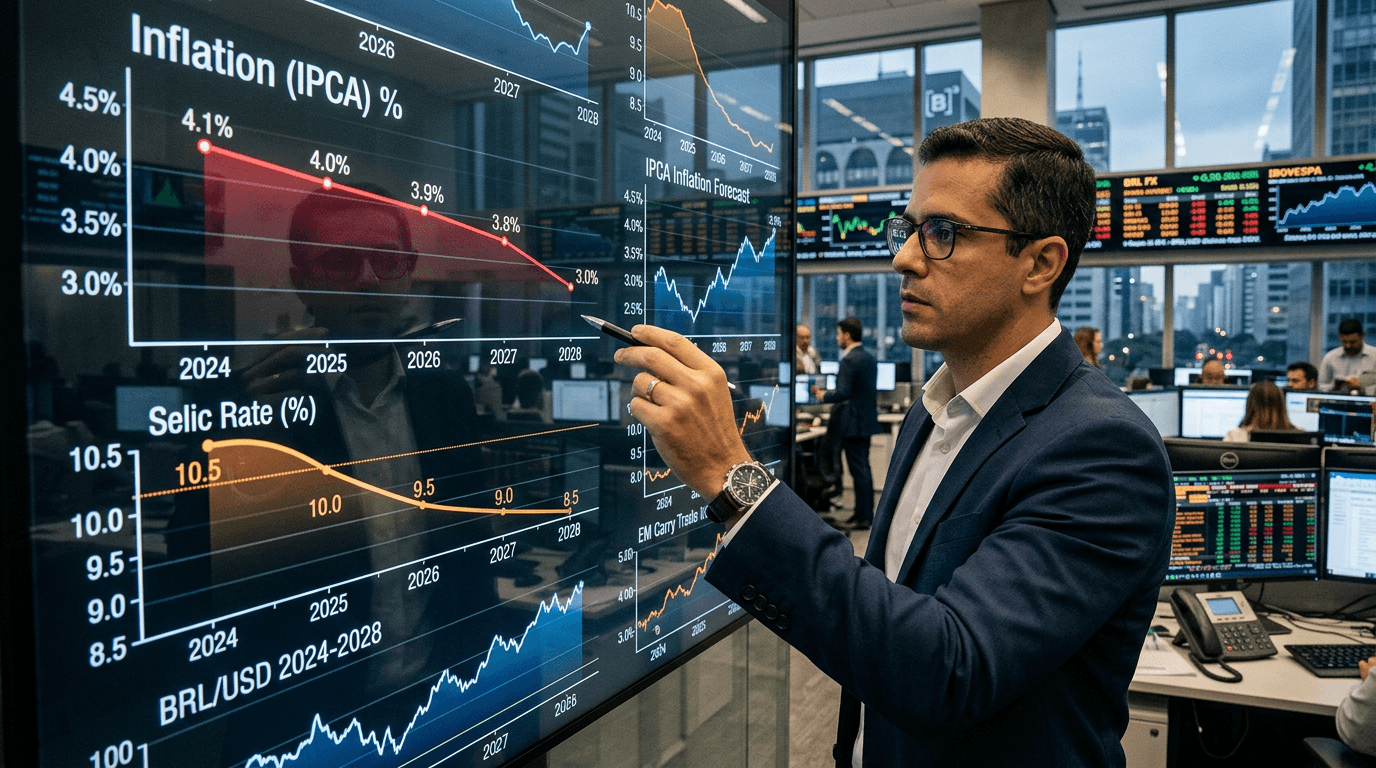

In its latest Monetary Policy Report, Banco Central do Brasil revised inflation forecasts higher for 2026 and 2027, acknowledging that the disinflation process will be slower than previously anticipated[1][7]. The relevant horizon for monetary policy—around the third quarter of 2027—now shows inflation projected at roughly 3.3%, above the 3.0% target but still within the tolerance band[7]. That signals lingering pressures even as headline inflation continues to trend down.

The central bank also raised its 2027 inflation forecast to 4.5% from 4.2% in one of its scenarios, citing weather-related risks that remain skewed to the upside if El Niño conditions persist[5]. This higher year‑end estimate highlights how sensitive Brazil’s inflation outlook is to food and energy shocks, which can quickly filter through to consumer prices. At the same time, projections for all quarters in 2026 and 2027 were revised upward, reflecting more robust economic activity and stronger-than-expected price pressures[1].

Crucially, the bank left its 2028 projections almost unchanged. Annual inflation is now expected around 3.1% in the final quarter of 2028, just above the 3.0% target[1]. Earlier quarters in 2028 remain near that level as well, reinforcing the narrative that while the near term is bumpy, the medium-term framework is intact. That “near target by 2028” path is what anchors the central bank’s credibility: markets are being told the institution is willing to tolerate a slower return to target, but not to abandon it.

Why Near-term Forecasts Worsened

The upward revisions for 2026–2027 are not just about models; they reflect tangible economic and global drivers. The central bank explicitly cited a more vigorous domestic economy and rising oil prices as key reasons for the higher inflation projections[1]. Stronger demand makes it harder for inflation to fall, particularly in services, while more expensive energy lifts transport, logistics, and production costs across the economy.

Weather is another key risk channel. El Niño can disrupt agricultural output, pushing up food prices—a historically volatile component of Brazil’s inflation basket[5]. Layered on top of this are global uncertainties: elevated commodity prices and geopolitical tensions keep imported inflation risks alive, especially for fuel and fertilizers[1][3]. These factors complicate the disinflation process, demanding a more cautious approach from policymakers.

Market economists have taken note. Brazil’s weekly Focus survey shows inflation forecasts rising for every year through 2028, with estimates now above the 3% target across the horizon[3]. That divergence between the central bank’s “near target by 2028” baseline and the market’s more skeptical view is exactly where trading opportunities—and risks—tend to emerge.

Implications For The Selic Rate And Yield Curve

A slower disinflation path naturally feeds into expectations for the Selic rate trajectory. Before the latest report, many investors hoped for a more aggressive easing cycle. Now, higher inflation forecasts and persistent upside risks suggest the central bank will move more gradually, keeping real rates elevated for longer[1][7]. That supports the idea of a “higher for longer” stance, even if nominal cuts continue at a measured pace.

Economists have already adjusted their rate projections. Surveys compiled by the central bank show expectations for the Selic at around 12% at end‑2027 and roughly 10.25% at end‑2028, up from prior estimates of 11.5% and 10% respectively[2][4]. Higher expected policy rates push the entire yield curve upward, particularly at the intermediate maturities that are most sensitive to inflation and growth revisions.

For local rates futures, this means steeper curves and more volatility around policy meetings, as each new data point either validates or challenges the bank’s inflation narrative. Longer-dated bonds will price in the credibility of the “3.1% by Q4 2028” forecast, while shorter-dated instruments will trade off the near-term overshoot and the pace of actual Selic moves.

Market Reaction: Brl Fx, Local Rates, And Em Carry

For BRL FX, higher real yields can be a double-edged sword. On one hand, elevated interest rates relative to peers support the currency by making Brazil attractive for carry trades. On the other, a perception that inflation is becoming entrenched can weaken confidence, especially if markets start doubting the central bank’s ability to deliver convergence by 2028[1][3][7]. The balance between these forces will depend heavily on incoming data and communication from policymakers.

In the EM carry space, Brazil remains a core destination thanks to its relatively high nominal and real rates. A slower easing cycle and a projected medium‑term return to target create a still-compelling carry story: investors earn attractive yields today with a central bank that, on paper, remains committed to price stability[1][7]. However, the path is less linear than before. Episodes of risk‑off sentiment or negative inflation surprises could trigger abrupt repricing in BRL pairs and local curves.

Local rates futures and inflation-linked bonds are particularly sensitive to the new forecast profile. Traders can express views on the credibility of the 2028 convergence by positioning along the curve—going long or short on specific tenors where they believe the market is mispricing the central bank’s resolve. Meanwhile, breakeven inflation levels will react to each revision in the economic outlook, offering tactical opportunities around data releases and policy reports.

What Traders And Simfi Users Should Watch

For traders using simulated finance (SimFi) platforms, the current Brazilian backdrop is an ideal case study in how forward guidance and forecasts drive markets beyond headline rate decisions. In a SimFi environment, participants can stress‑test scenarios where inflation fails to converge by 2028, forcing the central bank into a more hawkish stance, versus alternatives where global commodity prices ease and El Niño risks fade, allowing a smoother disinflation.

Key variables to monitor include monthly inflation prints, especially core and services measures; updates to the central bank’s Monetary Policy Report; Focus survey revisions; and global oil and food price trends[1][3][7]. Each shift in these inputs can alter the expected path of the Selic, the slope of the yield curve, and BRL’s relative attractiveness in EM carry baskets.

Practically, traders can use simulated strategies such as:

- Testing BRL carry trades versus other high‑yield EM currencies under different inflation paths.

- Exploring curve steepener or flattener positions in Brazilian rates futures based on views of the timing and depth of the easing cycle.

- Hedging BRL exposures with options in scenarios where inflation surprises prompt sharper‑than‑expected policy moves.

By combining the central bank’s baseline—near target by 2028—with their own risk scenarios, traders can build more robust frameworks for decision‑making, both in simulation and in live markets.