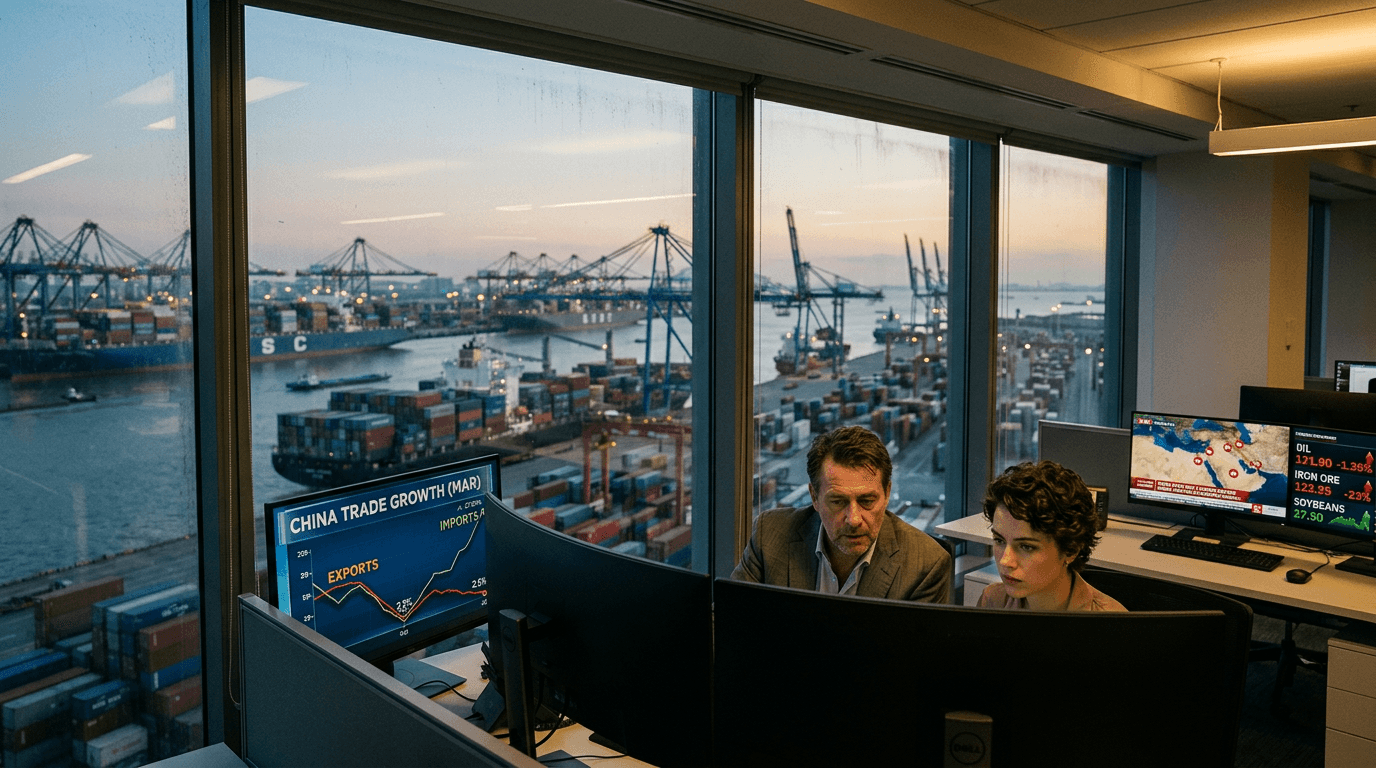

China's export engine is experiencing a significant slowdown. In March 2026, as the world's second-largest economy, it reported an export growth of just 2.5% year-on-year—a sharp decrease from the robust 21.8% surge seen in January and February. Meanwhile, imports tell a different story with a 27.8% surge in the same period. This divergence signals troubling headwinds for global trade and poses immediate implications for SimFi traders focused on commodity and currency futures. The contrasting import and export dynamics reveal a complex economic landscape shaped by geopolitical disruptions, elevated energy prices, and changing global demand patterns that traders must navigate.

The Data Breakdown: What The Numbers Reveal

The March export figures released by China's General Administration of Customs fell significantly below market expectations. Analysts had anticipated a 4% growth, making the 2.5% outcome a notable miss that rippled through global markets. Dollar-denominated exports reached $321.03 billion in March, compared to the combined $656.58 billion for January and February, when exports averaged nearly 22% year-on-year growth.

The import figures present an equally compelling narrative. At $269.9 billion, March imports marked the most substantial monthly increase since November 2021, far exceeding economist forecasts of 5.62% growth. This resulted in a trade surplus of $51.1 billion—substantial but smaller than earlier in the year when export growth dominated.

The technology sector, initially the main driver of China's export strength in early 2026, seems to have reached a temporary plateau. Semiconductor exports, propelled by the global artificial intelligence boom, fueled much of the acceleration in January-February. However, the March data suggests this momentum has stalled, possibly due to market saturation concerns and broader economic uncertainties sweeping global markets.

Geopolitical Disruptions And Commodity Shock

The Iran war and associated blockades in the Strait of Hormuz emerge as the primary factors behind March's softer export performance. These geopolitical tensions have disrupted global supply chains and significantly raised transportation costs for goods moving through one of the world's most critical shipping corridors. Elevated logistics costs directly reduce competitiveness for Chinese exporters, particularly in price-sensitive sectors.

This geopolitical stress also explains the dramatic import surge. Commodity and energy prices have skyrocketed due to Middle East tensions, prompting Chinese manufacturers and industries to rush purchases of raw materials before prices climb further. Copper ore imports jumped nearly 67% year-on-year in value terms, although actual volumes rose only 11.5%, clearly indicating price-driven demand. Similarly, fertilizer imports climbed 59% in value despite a modest 27% volume increase. Integrated circuit imports rose 54% in value compared to a 14% volume gain, reflecting both supply chain concerns and cost inflation.

For SimFi traders, these import dynamics present both challenges and opportunities. The flight to raw materials suggests market participants expect sustained inflation and supply chain stress. Energy futures, copper prices, and agricultural commodities are likely to remain elevated as long as Hormuz disruptions persist.

Export Performance Across Markets

The regional breakdown of China's export performance highlights telling market dynamics. Sales to non-US markets showed impressive resilience, with notable increases to Japan (8.9%), Hong Kong (38.7%), South Korea (27.0%), Taiwan (28.7%), Australia (29.4%), ASEAN countries (29.4%), and the EU (27.8%). This regional diversification reflects China's strategic response to US tariff pressures under Trump's 2025 renewed duties.

The US market remains the weak link, with sales declining 11% for the year-to-date period. Though trade negotiations have produced some tariff rollbacks, American import demand from China continues to face structural headwinds. This geographic shift in export patterns has significant implications for global logistics, regional trade flows, and ultimately, the forex and futures markets that traders monitor.

What This Means For Markets And Traders

For SimFi platforms and traders, the divergence between export softness and import strength creates a nuanced market signal. The March data suggests Chinese economic momentum remains domestically intact—the surge in imports indicates ongoing manufacturing activity and domestic demand. However, global demand for Chinese goods is weakening faster than anticipated, particularly given the geopolitical disruptions affecting trade routes and energy markets.

The miss on export expectations could trigger expectations for increased Chinese economic stimulus. Analysts note that despite resilient exports and a lower 2026 GDP growth target, the slowdown may prompt Beijing to accelerate stimulus measures. This prospect could strengthen the Chinese yuan in the medium term, as stimulus typically boosts growth expectations and attracts capital inflows.

Commodity traders should particularly note the import surge as a leading indicator for continued resource demand. The willingness of Chinese importers to absorb higher commodity prices signals confidence in manufacturing output and suggests global demand destruction may be limited even amid geopolitical stress.

Looking Ahead: What To Watch

The trajectory of the Iran conflict will be the primary determinant of China's export outlook in the coming months. A resolution to Hormuz disruptions could see exports reaccelerate substantially. Conversely, further escalation risks an extended period of weak export growth combined with volatile commodity prices—a scenario that would pressure multiple asset classes simultaneously.

Monitor April and May export data closely. If March's 2.5% represents a temporary shock that reverses as Hormuz concerns ease, Chinese export momentum could recover. If the slowdown persists, it signals genuine weakness in global demand that could trigger broader market repricing across equities, currencies, and commodities.