The dollar’s latest pullback is a reminder that FX markets are rarely driven by a single narrative. When weaker U.S. data meets improving risk appetite, the result is a classic rotation out of the safety of the greenback and into higher‑yielding, higher‑beta currencies. For traders, this is less about a one‑day move and more about how sentiment around the Federal Reserve and global risk trends is evolving.

WHAT’S HAPPENING WITH THE DOLLAR INDEX?

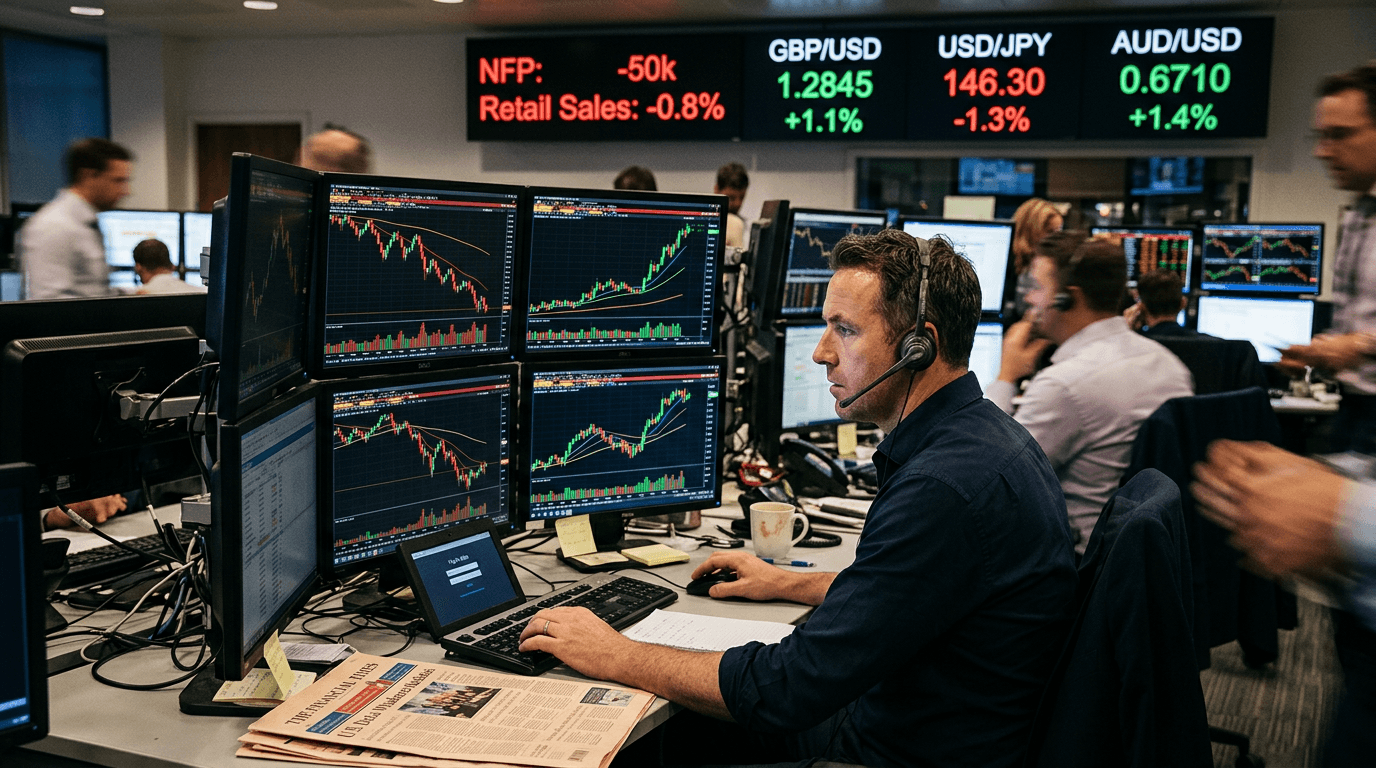

The U.S. Dollar Index (DXY) measures the dollar’s value against a basket of major currencies, with the euro, yen, and pound making up the bulk of the index.[3] When DXY falls, it signals that, on balance, the dollar is losing ground versus its main peers.

In the latest move, the index has slipped as softer U.S. producer price data and weaker consumer sentiment reinforced expectations that the Federal Reserve may take a more dovish tone. At the same time, risk assets have found better support, encouraging investors to rotate away from safe‑haven exposure and toward currencies and assets that tend to benefit when risk appetite is strong.[1][3]

This combination of factors has weighed on USD/JPY – traditionally a key barometer of risk sentiment – while providing a tailwind to pairs like GBP/USD and AUD/USD, which typically benefit when the dollar softens and global risk appetite improves.

For traders, the key takeaway is that the move is not just “dollar weakness”; it is a repricing of interest rate expectations and risk sentiment happening simultaneously.

WEAKER U.S. DATA AND DOVISH FED EXPECTATIONS

FX markets are forward‑looking. When incoming data suggests a slower economy or cooling inflation pressures, traders immediately reassess the likely path of monetary policy.

Softer producer prices (PPI) point to easing pipeline inflation. Combined with deteriorating consumer sentiment, this raises doubts about the strength and durability of U.S. demand. If inflation pressures are easing and consumer confidence is slipping, the Fed has less incentive to maintain an aggressive policy stance.

That is why weaker data often translates into

- Lower expectations for future rate hikes, or even higher probability of rate cuts

- Reduced yield advantage for the dollar versus other currencies

- A softer DXY as investors rebalance portfolios away from USD‑denominated assets

Previous episodes have shown the opposite dynamic: when data surprises on the upside and Fed speakers lean hawkish, the dollar tends to catch a strong bid while risk assets struggle.[2] The current environment reflects the mirror image: data that leans soft and a market that is increasingly willing to price in a more patient or dovish Fed.

Practical takeaway: keep an eye on how each major U.S. data print (inflation, jobs, consumer, manufacturing) shifts implied Fed rate expectations in futures and swaps markets. The dollar often follows.

Risk Appetite, Safe Havens, And Currency Rotation

The dollar is more than a domestic currency; it is a global reserve and a core safe haven. In periods of stress, capital typically flows into the dollar as investors seek liquidity and perceived safety. When conditions calm and risk appetite improves, those same flows can reverse.

An improvement in global risk sentiment usually involves:

- Stronger equity markets and tighter credit spreads

- Reduced demand for classic safe havens such as the dollar, yen, and U.S. Treasuries

- Increased demand for higher‑yielding or “risk‑sensitive” currencies, such as AUD, NZD, some emerging‑market FX, and to a degree, GBP

When DXY is under pressure due to rising risk appetite, as seen in prior episodes where a sustained “risk‑on” mood depressed the index,[1] it often reflects:

- Reduced hedging demand in USD

- Reallocation into carry trades (borrowing in low‑yield currencies, investing in higher‑yield ones)

- A more constructive outlook on global growth and trade

For traders, this means that understanding “risk‑on vs. risk‑off” is just as important as understanding the data itself. The same economic print can have a different market impact depending on whether investors are already nervous or optimistic.

HOW MAJOR PAIRS ARE REACTING: USD/JPY, GBP/USD, AUD/USD

The current move has not been uniform across FX pairs. Instead, we see the typical pattern that emerges when the dollar softens and risk appetite improves:

USD/JPY: The yen is both a safe haven and a low‑yielding funding currency. In a pure risk‑off shock, USD/JPY can fall sharply as investors unwind carry trades and buy back yen. In the latest move, USD/JPY has been pressured primarily by the softer dollar side: lower U.S. yields and dovish Fed expectations reduce the interest rate differential that had been supporting the pair.

GBP/USD: The pound tends to benefit when the dollar weakens, especially if the Bank of England is seen as relatively more hawkish or if UK data is stable. A softer dollar combined with improved risk appetite has supported GBP/USD, allowing the pair to climb as DXY retreats. For traders, this environment can favor buy‑the‑dip strategies in cable, provided UK fundamentals do not deteriorate sharply.

AUD/USD: The Australian dollar is a classic “risk‑sensitive” currency, heavily influenced by global growth expectations, commodity prices, and China‑related sentiment. When risk appetite improves and the dollar eases, AUD/USD often outperforms. This is exactly the kind of environment where AUD can benefit from both sides: better risk sentiment and a weaker USD.

Across these pairs, FX volatility has tended to increase around key U.S. data releases, reflecting uncertainty over how each print will reshape the Fed outlook and risk sentiment. For active traders, this volatility can be an opportunity—but only with disciplined risk management.

How Traders Can Position Around A Softer Dollar

For both live and simulated trading, a softer dollar driven by weaker data and stronger risk appetite offers several actionable lessons:

1. Trade the narrative, not just the number Do not look at data in isolation. Ask: what does this mean for Fed policy, and how does that feed into risk appetite? If softer data reinforces a dovish narrative, dollar rallies into key resistance zones may be selling opportunities.

2. Use DXY as a macro barometer Monitoring the Dollar Index alongside major pairs helps you distinguish between broad USD moves and currency‑specific themes.[3] A falling DXY with rising GBP/USD and AUD/USD suggests a generalized dollar story, not just idiosyncratic UK or Australian news.

3. Align timeframes and instruments Short‑term traders may focus on intraday volatility around data releases, using tight stops and defined risk. Swing traders can look for confirmation that DXY is forming lower highs or breaking key support before leaning more aggressively into dollar‑short ideas.

4. Respect volatility and liquidity Data releases can cause sharp spreads and rapid price gaps. In both real and SimFi environments, it is critical to size positions conservatively, avoid over‑leverage, and be prepared for slippage around major announcements.

5. Think in scenarios Map out “what if” paths: - If upcoming data continues to soften and Fed rhetoric turns more dovish, the dollar could stay on the back foot, favoring pro‑risk currency trades. - If data stabilizes or rebounds, the market may quickly pare back aggressive easing bets, supporting a dollar recovery.

Ultimately, the current slide in the Dollar Index is a live case study in how macro data, central bank expectations, and risk sentiment intersect in FX. For traders willing to step back from the noise and focus on those bigger drivers, it is an opportunity not just to trade, but to sharpen their entire macro framework.