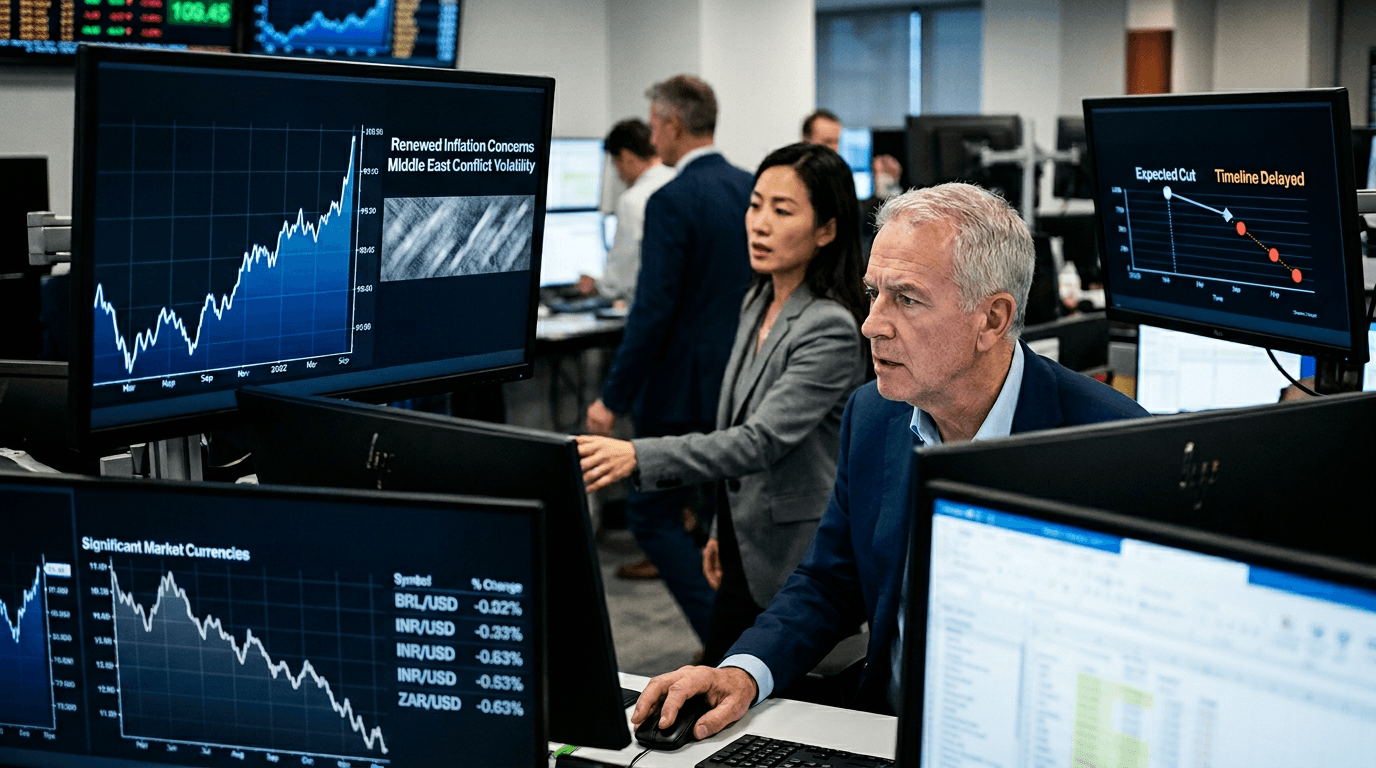

The US dollar is experiencing renewed strength as markets grapple with conflicting signals from geopolitical tensions and economic data. On Wednesday afternoon, a New York Times report about potential negotiations between the US and Iran sent the dollar temporarily lower, but this reprieve was short-lived. Within hours of Iran's denial of the talks, the greenback resumed its upward trajectory, reflecting the complex forces currently reshaping currency markets. The underlying driver of this strength isn't safe-haven demand in the traditional sense—it's the resurgence of inflation concerns tied to Middle East volatility and the Federal Reserve's constrained ability to cut rates.

The Dollar's Conflicting Signals

The dollar's recent movements reveal something important about modern currency markets: they respond not just to what happens, but to what it means for the entire global economy. The brief dip on Iran-US talks rumors illustrated trader optimism about a potential near-term resolution to the Middle East conflict. The Trump administration has guided markets toward a 4-5 week timeline for the conflict's duration. However, the quick reversal after Iran's denial demonstrates that markets remain skeptical about a swift resolution.

This skepticism is justified. Iran has become less politically homogeneous following the deaths of key ruling elite representatives, creating contradictory signals about the country's negotiating position. The Strait of Hormuz blockade remains an unpredictable wildcard, adding layers of uncertainty to oil prices and equity markets. These factors have combined to push the US Dollar Index above 99, reaching its highest level since mid-January.

Inflation Fears Trump Geopolitical Optimism

What's driving the dollar's strength isn't what we traditionally call "safe-haven" demand. According to Bundesbank leadership, questions about the dollar's role as a genuine safe haven have resurfaced. In the current environment, investors have been gravitating toward gold, Swiss francs, and US Treasuries instead of traditional dollar positioning. Yet the dollar has strengthened anyway—a phenomenon that reveals the true driver of current market dynamics: inflation expectations.

Rising oil prices create an immediate problem for Federal Reserve policymakers. The central bank has been in a rate-cutting cycle since December, but has paused that easing. That pause becomes increasingly defensible—even necessary—when energy prices spike. Higher oil costs filter through the economy as higher transportation, manufacturing, and consumer goods prices. This inflation pressure makes it much harder for the Fed to justify aggressive rate cuts, even as markets had previously expected relief starting in July. Current futures pricing suggests the next Fed rate cut won't come until September, a two-month delay from earlier expectations.

This reality supports the dollar across multiple timeframes. For currency traders, a Fed that can't cut rates is a Fed that supports higher yields on US Treasuries. The yield differential between US and German bonds remains wide, creating mechanical demand for dollars from yield-seeking investors.

Strong Economic Data Reinforces The Dollar

Beyond geopolitical noise and energy prices, the underlying US economy continues to surprise to the upside. Recent ADP employment data showed private sector job creation of 63,000 workers in February—the strongest result since July and above the consensus forecast of 50,000. More impressively, the ISM Services Purchasing Managers' Index jumped to 56.1, marking its highest level since August 2022.

These data points matter because they validate why the Fed can afford to pause rate cuts. The labor market isn't collapsing, and service sector activity remains robust. This economic resilience directly contradicts the narrative that would justify aggressive monetary easing. From a currency perspective, it reinforces that the dollar's current strength rests on genuine economic fundamentals, not just geopolitical nervousness or relative weakness elsewhere.

Other Currencies Under Pressure

The dollar's ascent has come at the expense of virtually every other major currency. The Australian dollar gained no support from Australia's 2.6 percent GDP growth in 2025—the fastest pace in three years—as markets decided this data was already priced in. Expectations for an RBA rate hike fell from 37 percent to just 20 percent. The British pound remains under pressure from both dollar strength and domestic political concerns following Labour Party defeats in local elections. Even the Japanese yen, boosted by central bank head Kazuo Ueda's hawkish rate-hike rhetoric, faces headwinds from the conflict's negative impact on Japan's energy-dependent economy.

Emerging market currencies have experienced their worst trading session since November 2024, as the stronger dollar and geopolitical risk aversion trigger capital flows away from riskier assets.

Key Takeaways For Traders

The current dollar strength reflects a structural shift in how markets price currency dynamics. Inflation fears have become more important than traditional safe-haven narratives. The Fed's rate-cut timeline is being pushed further into the future. Oil price volatility tied to Middle East tensions may persist for weeks or months. Meanwhile, the US economic data continues to support dollar positioning on its merits, independent of geopolitical factors.

For portfolio managers and traders, this suggests the dollar's strength may have more staying power than typical conflict-driven rallies. The convergence of energy inflation, Fed policy constraints, and solid economic growth creates a powerful dollar headwind against most other currencies.