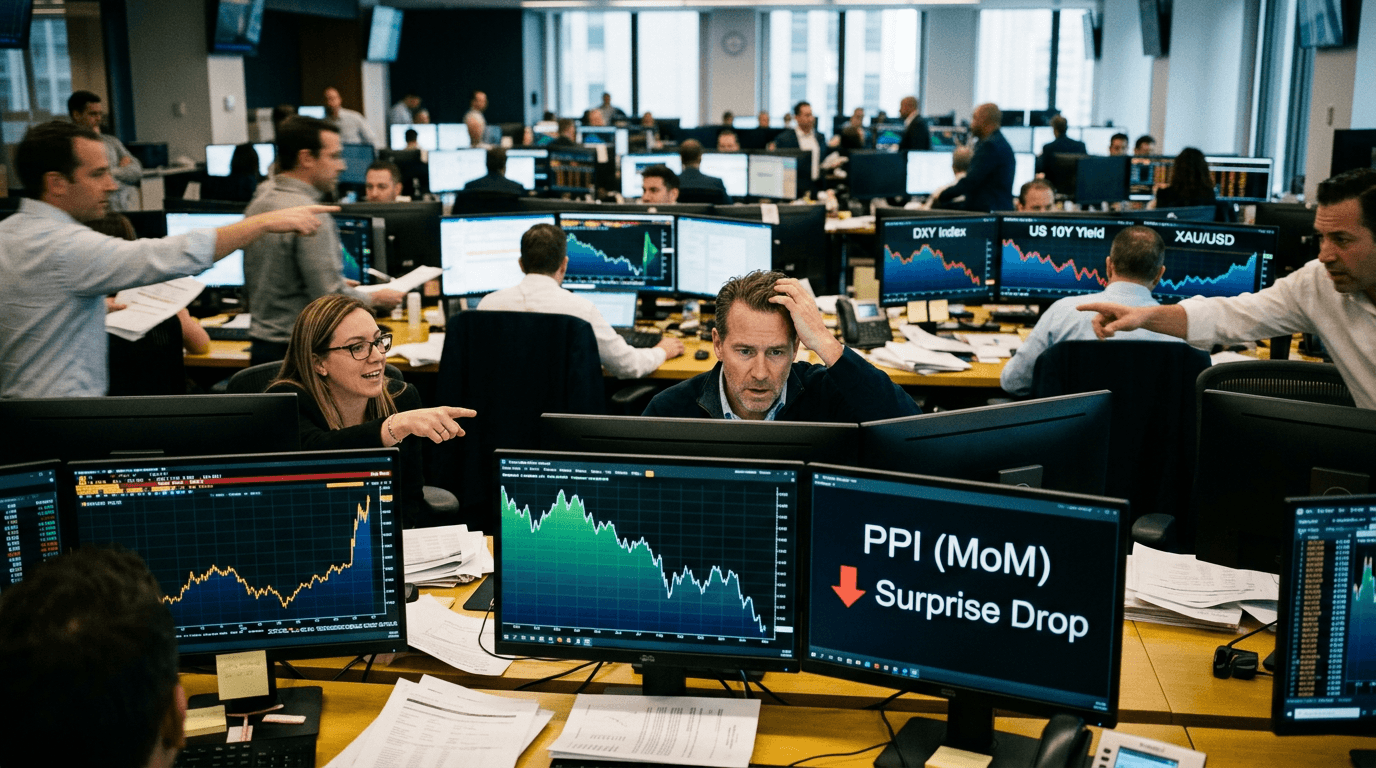

US producer prices delivered a surprise drop, and markets reacted instantly. Instead of the modest increase economists expected, both headline and core Producer Price Index (PPI) readings turned negative on the month, signaling a sharper-than-forecast cooling in pipeline inflation.[1][5] That single data point was enough to send Treasury yields lower, knock the US dollar back, and turbocharge expectations that the Federal Reserve could start cutting rates sooner rather than later.[1][2]

What The Ppi Data Just Told The Market

PPI tracks how much businesses receive for the goods and services they sell, effectively measuring “factory-gate” inflation before it hits consumers.[5] When both headline PPI (including food and energy) and core PPI (excluding them) fall in the same month, it suggests underlying price pressures are easing across a broad front, not just in volatile components.[1][5]

Consensus had looked for a small month-on-month increase, consistent with the idea that inflation was moderating but still sticky. Instead, the negative surprise flipped that narrative: not only did overall wholesale prices decline, but the core measure also slipped into contraction territory.[1] That combination signals disinflation deeper in the production pipeline than markets had priced in.

It is important to stress that, on a year-over-year basis, PPI is still positive, meaning prices are higher than a year ago, just rising more slowly.[2][3] However, the month-on-month drop is what matters for forward-looking traders: it is a timely signal that the inflation pulse might be fading faster than previously thought.

Why Producer Prices Matter For The Fed

The Federal Reserve does not target PPI directly; its mandate is based on consumer inflation. But producer prices are an important input into the inflation story because they help determine future costs for businesses that eventually get passed on to households.[5] When PPI softens, it increases the odds that CPI and the Fed’s preferred PCE inflation measure will also ease in the coming months.

Heading into this release, the dominant narrative was that the Fed would stay cautious, keeping rates high for longer to ensure inflation stayed on a clear path back toward its 2% target. The downside PPI surprise challenged that stance by suggesting less price pressure building up in the system.[1][2]

Money markets reacted immediately. Short-term interest rate futures shifted to price in earlier and potentially deeper rate cuts, reflecting a view that the Fed might not need to keep policy as restrictive as previously assumed.[1] Lower expected policy rates in the future translate into lower yields today, especially on shorter-dated Treasuries that are most sensitive to Fed expectations.

Market Reaction: Dollar Down, Forex And Gold Up

The market’s reaction followed a familiar pattern for a “dovish” macro surprise: yields down, dollar down, risk assets and gold up.[1]

US Treasury yields fell across the curve, led by the 2-year sector as traders marked down the likely path of Fed policy. Lower yields reduce the interest-rate advantage of US assets versus their global peers, undercutting support for the US dollar.[1] As rate differentials moved against the USD, major forex pairs responded quickly.

EUR/USD and GBP/USD both rebounded, with traders using the weaker dollar as an opportunity to rotate into higher-yielding or relatively less-hawkish currencies.[1] For euro and sterling bulls, the PPI report offered a macro catalyst that aligned with longer-running themes of a peak in US exceptionalism and a gradual convergence in monetary policy stances.

Gold also caught a strong bid. A weaker dollar makes bullion cheaper in non-USD terms, while lower real yields (nominal yields minus inflation expectations) enhance the appeal of holding a non-yielding asset like gold.[1] For traders, the move was a classic example of how a single inflation data point can ripple across currencies, bonds, and commodities in a matter of minutes.

What Traders Should Watch Next

For discretionary and systematic traders alike, this PPI surprise is not the end of the story; it is a new chapter in the ongoing inflation and policy narrative. A few key focus points stand out:

1) Fed communication: Watch speeches, meeting minutes, and press conferences closely. Do policymakers frame the PPI data as validation that disinflation is back on track, or as a single data point not yet enough to shift their stance?

2) Next CPI and PCE prints: If upcoming consumer inflation data confirm the disinflation suggested by PPI, the market’s more dovish rate expectations could solidify. If they rebound, traders may need to quickly re-price toward a “higher for longer” narrative.

3) Market expectations vs. Fed guidance: When futures markets price more aggressive cuts than the Fed’s own projections, the gap can become a source of volatility. The larger that divergence, the more sensitive assets like the dollar and short-dated yields become to any surprise in data or messaging.

4) Cross-asset correlations: Moves in PPI, yields, the dollar, and gold often travel together, but the strength and timing of those relationships can change. Active traders should continuously reassess how sensitive their preferred instruments are to macro surprises.

Using Simulated Trading To Navigate Macro Shocks

Macro data shocks like this PPI release are ideal case studies for traders to practice and refine their playbook in a simulated environment. The chain of events is clear, the timing is precise, and the reactions span multiple asset classes—perfect conditions for structured learning.

In a SimFi setting, traders can:

1) Recreate the event: Mark the time of the PPI release and replay price action in pairs such as EUR/USD, GBP/USD, USD/JPY, as well as gold and major equity indices. Study how spreads, volatility, and liquidity evolved before and after the print.

2) Test trade ideas: For example, design strategies around going long EUR/USD or gold on a downside inflation surprise, or short USD/JPY as US yields drop. Experiment with different stop-losses, profit targets, and position sizes to see which combinations handle volatility best.

3) Build a macro checklist: Before each high-impact release, define scenarios (soft, in-line, hot), likely policy implications, and expected cross-asset reactions. After the event, compare what you planned versus what actually happened and refine your framework.

4) Strengthen risk management: Data releases can produce gaps, slippage, and rapid trend reversals. Using simulated capital to trial approaches such as scaling in, reducing exposure ahead of the event, or using options-like structures can help traders build discipline without financial stress.

For both new and experienced traders, the latest PPI surprise is less about a single number and more about understanding how macro data connects to central-bank expectations, yields, the dollar, and broader risk sentiment. Practicing that sequence repeatedly—especially in a risk-free simulated environment—can transform headline news into structured opportunity rather than emotional noise.