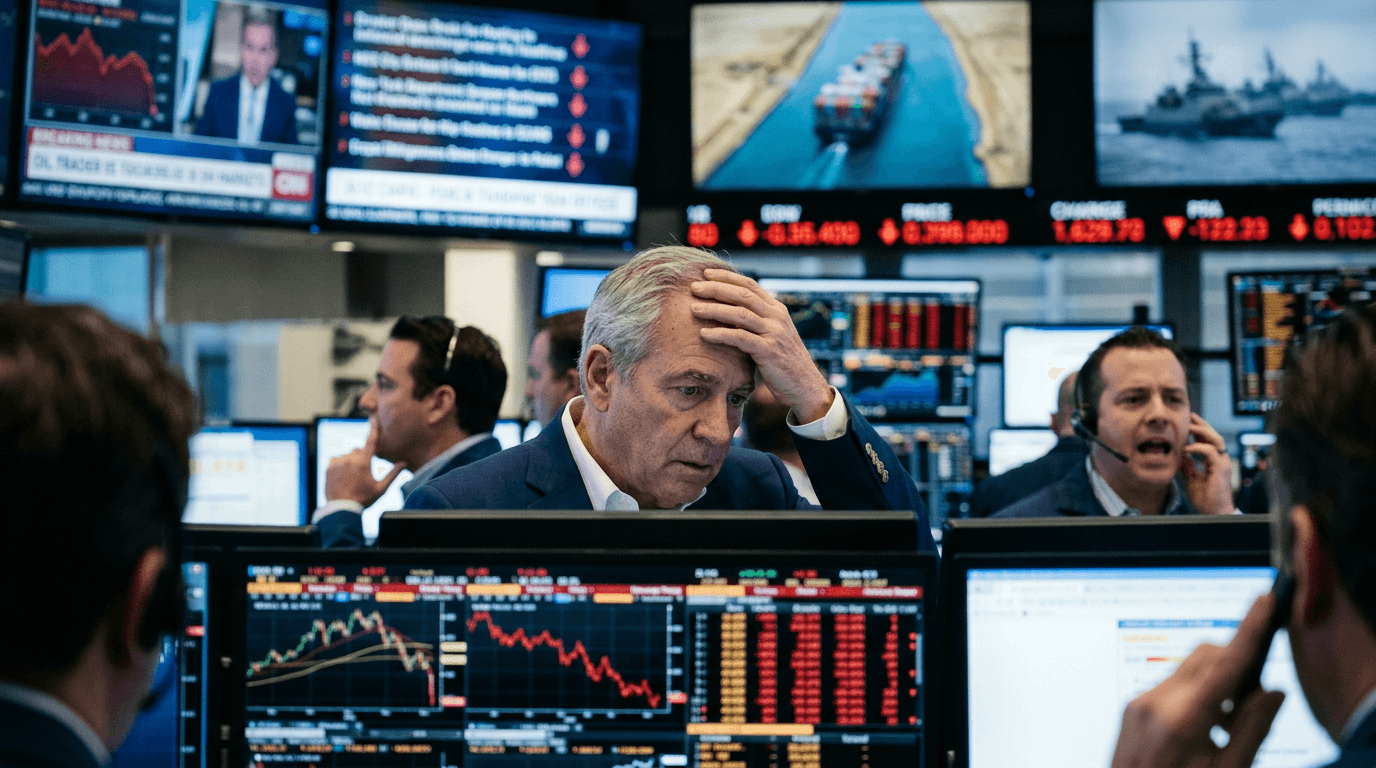

Oil markets have been thrown back into crisis mode as the escalating US‑Iran war and an effective shutdown of the Strait of Hormuz sent crude prices sharply higher and rattled risk assets worldwide. WTI futures jumped as much as 9% intraday to fresh multi‑month highs, with Brent following suit, as traders rushed to reprice the risk of a sustained supply disruption. The move has revived uncomfortable memories of past oil shocks and injected a fresh stagflation scare into already fragile global markets.

What Just Happened In Oil And Risk Assets

The immediate catalyst was the combination of direct military confrontation between the US and Iran and a de facto closure of the Strait of Hormuz, a maritime chokepoint critical for global energy flows. Shipping data showed a steep drop in tanker traffic through the strait, while reports of attacks on vessels and enforcement of blockades reinforced the perception that normal operations have halted.

Energy markets reacted first and fastest

- WTI crude spiked up to 9% on the day, breaking through recent resistance levels and printing new multi‑month highs.

- Brent, the global benchmark, rallied in tandem, widening the Brent‑WTI spread as seaborne supply risk was repriced.

Equities and other “risk assets” quickly followed:

- Major US indices opened sharply lower, with energy names outperforming but broad benchmarks dragged down by financials, consumer stocks, and cyclicals.

- European and Asian indices sold off as traders began to factor in weaker growth and potentially higher input costs.

In FX and rates, the move was classic “risk‑off with a twist”:

- Commodity‑linked currencies such as the Canadian dollar and Norwegian krone initially found support from higher crude prices.

- Safe havens like the US dollar, Japanese yen, and Swiss franc strengthened as the session progressed.

- Bond markets saw a push‑pull dynamic: safe‑haven demand pressured yields lower, while rising inflation expectations from higher energy prices pushed breakevens higher, reviving stagflation fears.

Why The Strait Of Hormuz Matters So Much

The market’s outsized reaction is best understood through the lens of physical energy flows. The Strait of Hormuz is one of the world’s most important commodity corridors:

- Historically, roughly a fifth of global seaborne crude oil exports pass through this narrow waterway.

- A significant share of global liquefied natural gas (LNG) exports, particularly from Qatar, also transits Hormuz.

- The region is a key supplier of refined products like jet fuel and diesel, as well as industrial feedstocks such as ammonia and sulfur.

When a corridor this central is disrupted, even temporarily, markets do not just price the barrels currently at risk. They price a distribution of scenarios, from a short‑lived scare to a prolonged shutdown that forces a re‑routing of trade, a buildup of military risk premiums, and even demand destruction if prices remain elevated.

Several layers of uncertainty are now being repriced:

- Duration risk: How long will the strait remain effectively closed?

- Escalation risk: Will attacks spread to infrastructure such as pipelines, ports, or refineries?

- Substitution risk: How much can be offset by alternative routes, strategic reserves releases, or increased production elsewhere?

This is why the price impact goes well beyond a simple “X million barrels per day” calculation. The market is discounting the possibility that, even if flows resume, the perceived risk of transit through Hormuz will remain high, keeping a risk premium baked into prices.

Ripple Effects Across Major Asset Classes

For traders, the key is understanding how this oil shock transmits through different markets.

1. Equities

Higher energy prices can have mixed effects on stocks:

- Positive for: Energy producers, oilfield services, and some commodities‑linked infrastructure plays, which may benefit from higher realized prices and increased upstream investment.

- Negative for: Energy‑intensive sectors (airlines, transportation, chemicals), consumer discretionary (as fuel eats into disposable income), and most growth‑sensitive cyclicals.

When the oil move is driven by war and supply risk rather than strong demand, the net effect tends to be negative for broad indices. That is what we are seeing now: pockets of strength in energy, overwhelmed by worries about margins, earnings, and macro growth.

2. Currencies

FX markets are balancing three forces

- Terms‑of‑trade boosts for oil exporters (CAD, NOK, some EMs).

- Safe‑haven inflows into USD, JPY, CHF.

- Pressure on oil‑importing EMs (e.g., India, Turkey) via wider current account deficits and inflation.

Initially, higher oil can see commodity currencies rally. But if global risk sentiment deteriorates sharply, the safe‑haven bid can dominate, leaving high‑beta FX under pressure despite favorable commodity fundamentals.

3. Rates and inflation expectations

Bond markets are wrestling with a stagflation‑type shock:

- Growth outlook: Weaker, as higher energy prices act like a tax on consumers and businesses.

- Inflation outlook: Stronger, at least in the near term, via higher headline CPI.

This mix can create a flattening yield curve, with longer‑term yields caught between lower real growth expectations and higher inflation risk. Inflation‑linked bonds and breakeven measures often move higher as traders price in the energy pass‑through to consumer prices.

4. Commodities beyond crude

Natural gas, refined products, and certain industrial commodities linked to Gulf exports may see their own supply‑risk premia rise. Conversely, if the market starts to price serious demand destruction, some industrial metals could come under pressure despite the geopolitical stress.

Trading Implications: Volatility, Correlations, And Risk Management

For active traders, an oil‑driven geopolitical shock is as much about correlation shifts and volatility as it is about direction.

Key implications

- Volatility spikes: Implied volatility tends to rise in crude, equity indices, and FX pairs linked to safe havens and commodity exporters. Option pricing changes quickly, affecting hedging costs and strategy selection.

- Correlation breakdowns: Relationships that held in calmer regimes (e.g., strong stocks with weak oil, or CAD tightly tracking WTI) can either intensify or invert depending on whether growth or risk aversion dominates.

- Liquidity pockets: During headline‑driven sessions, liquidity can thin around event windows, with wider spreads and more frequent price gaps.

Practical considerations for traders

- Position sizing: Elevated volatility increases the probability of large intraday swings. Reducing size or widening stops to account for higher average true range can keep risk per trade more consistent.

- Scenario planning: Map out at least three scenarios—rapid de‑escalation, prolonged standoff with intermittent attacks, and significant escalation—and consider how each would impact your core markets.

- Cross‑asset confirmation: Use signals across commodities, FX, rates, and equities to distinguish between “oil up on demand” (bullish growth) and “oil up on war” (bearish growth).

Simulated trading environments can be particularly useful in this kind of regime. Testing how your strategy performs under historic oil shocks or custom stress scenarios can highlight vulnerabilities—over‑concentration in a single theme, overreliance on stable correlations, or insufficient volatility filters—before you deploy real capital in a jumpy market.

What To Watch Next

The path from here depends less on current prices and more on event risk:

- Shipping data: Actual tanker movements through Hormuz will be a high‑frequency indicator of whether the shutdown is tightening or easing.

- Policy responses: Strategic petroleum reserve releases, production changes from OPEC+ and non‑OPEC producers, and potential sanctions adjustments will all affect the supply‑demand balance.

- Macro data: Incoming inflation prints, PMIs, and consumer confidence surveys will reveal how quickly the oil shock is feeding into the broader economy.

- Market stress signals: Credit spreads, EM FX, and front‑end funding markets can flag whether the shock is morphing from a commodity story into a broader financial stability issue.

For now, traders are dealing with a classic oil‑shock playbook: higher crude, pressured risk assets, safe‑haven demand, and a renewed debate over stagflation. In this kind of environment, discipline around risk, an eye on cross‑asset signals, and a willingness to adapt to fast‑changing correlations matter as much as getting the directional call on oil itself.