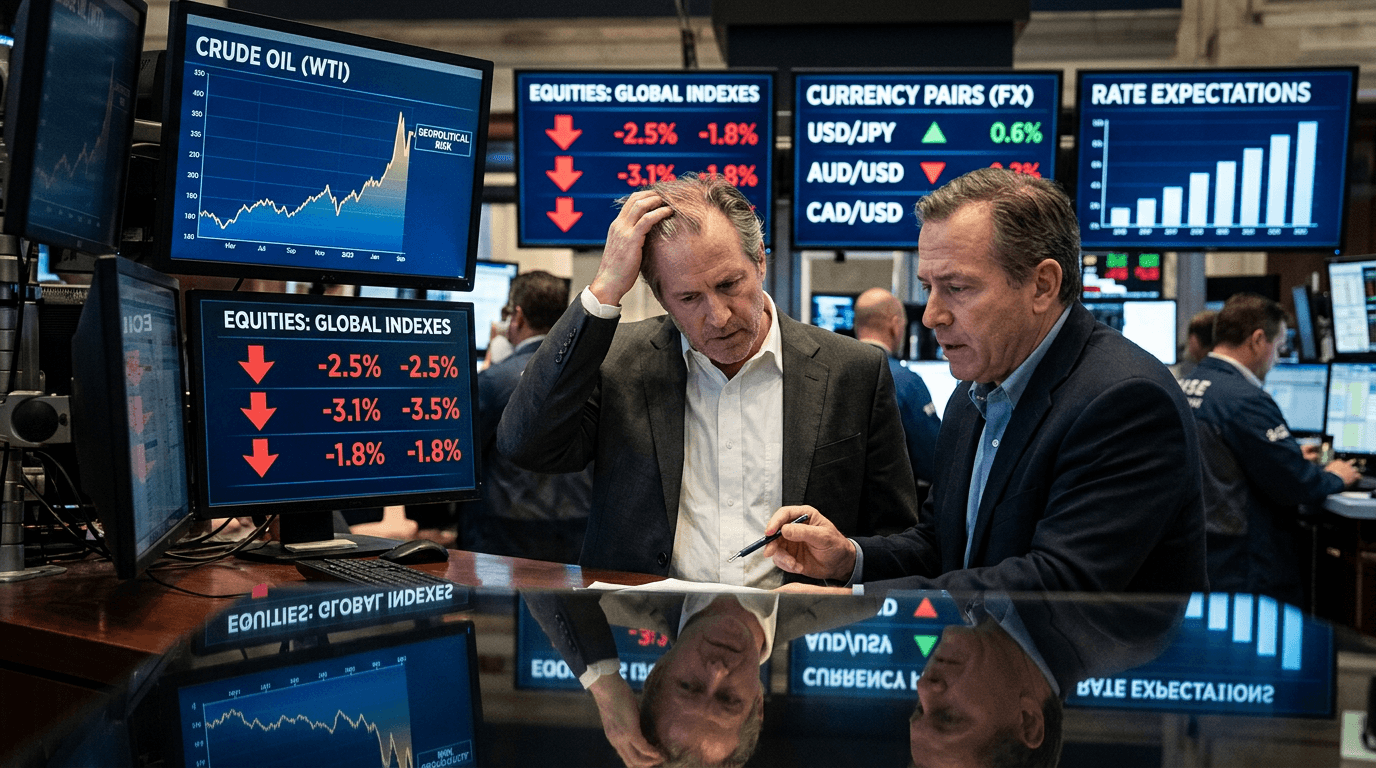

Oil prices and Middle East tensions are once again at the center of market narratives, pressuring risk assets and reshaping expectations for inflation and interest rates. Earlier spikes in crude and renewed geopolitical risk have kept inflation fears alive, undermining hopes for rapid central-bank easing and pushing investors back toward safe havens. For traders across FX, futures, equities, and commodity-linked currencies, this is a classic macro environment where cross-asset relationships matter more than ever.

Markets At The Crossroads: Oil, Geopolitics And Inflation

Geopolitical tensions in the Middle East matter for markets because they intersect with one of the most critical chokepoints in global trade: the Strait of Hormuz. Roughly a quarter of global seaborne oil passes through this narrow waterway, along with significant volumes of liquefied natural gas and fertilizers[3]. Any disruption or perceived threat to shipping immediately feeds into energy prices, freight rates, and insurance costs.

At the same time, countries surrounding the Persian Gulf account for around 30% of global oil production[1]. When tensions flare, markets must price not only near-term supply risks but also the possibility of longer-lasting disruptions, sanctions, or production cuts. This uncertainty has helped push Brent crude above the psychologically important $90 per barrel level at times[3], reigniting debate about the inflation outlook just as many investors were counting on disinflation to continue.

Key takeaway: When a region that controls a large share of global oil flows becomes unstable, it is not just a political story—it is an inflation and interest-rate story, and therefore a broad market story.

Why Oil Shocks Hit Inflation So Quickly

Oil-driven inflation operates through both direct and indirect channels. Directly, higher crude prices translate into more expensive gasoline, diesel, and jet fuel. One estimate suggests that if oil holds around $90 per barrel, the petrol component of consumer price indices could jump around 15%, adding roughly 0.5 percentage points to headline inflation in the first month alone[1]. Once second-round effects—like higher transportation and production costs—are included, the total impact can approach 0.75 percentage points[1].

Indirectly, energy is embedded in almost every good and service. Higher fuel costs raise shipping and logistics expenses, while increased natural gas and fertilizer prices push up food costs, aggravating cost-of-living pressures[3]. This is particularly challenging for developing economies already struggling with high debt burdens and limited fiscal space to absorb new price shocks[3].

Recent experience has shown that inflation can broaden beyond energy. In several economies, price pressures have reaccelerated across multiple sectors, broadening beyond the initial shock from oil and geopolitical tension[2][4]. That raises the risk that inflation expectations become less anchored, forcing central banks to stay hawkish for longer than markets would prefer.

Key takeaway: Oil spikes rarely remain “just” an energy story; they tend to spill over into food, transport, and core prices, complicating the inflation outlook long after the initial shock.

CENTRAL BANKS AND THE “HIGHER FOR LONGER” DILEMMA

Before the latest flare-up in the Middle East and the associated oil moves, markets were increasingly confident that major central banks would pivot to easier policy. Rate futures had priced in multiple cuts over the coming year, reflecting faith that inflation was on a steady path back to target.

Rising geopolitical risk and renewed oil-price volatility have challenged that conviction. Analysts have warned that sustained increases in Brent crude could push inflation higher just as central banks were preparing to ease[5]. If energy-driven price pressures feed into broader inflation, policymakers may be forced to pause or slow rate cuts, or in some cases signal a willingness to keep rates restrictive for longer.

This shift in expectations has meaningful consequences for risk assets. Higher real yields increase the discount rate applied to future cash flows, which tends to weigh on growth and technology stocks with long-duration earnings. Credit markets may see wider spreads as investors demand more compensation for risk when policy looks less supportive. Derivatives and futures markets adjust rapidly, with implied rate paths repriced in response to every new inflation or geopolitical headline.

Key takeaway: Oil-driven inflation fears reduce the probability of rapid rate cuts, raising discount rates and creating a tougher backdrop for risk assets that rely on easy money and low volatility.

How Risk Assets And Currencies Are Responding

The combination of persistent inflation concerns and geopolitical uncertainty generally produces a familiar market pattern: risk-off in equities and credit, risk-on in safe havens. Equity indices may struggle, even if headline moves look modest, as leadership rotates below the surface. Energy and certain commodity producers can benefit from higher prices, while rate-sensitive growth names face pressure.

Safe-haven demand typically supports assets like US Treasuries, the US dollar, the Japanese yen, and the Swiss franc when geopolitical stress rises. At the same time, risk-sensitive or “high-beta” currencies—such as those of emerging markets with large external financing needs—often come under pressure. Many developing economies already face high debt service costs and limited ability to cushion their populations from higher energy and food prices[3], making them particularly vulnerable to prolonged oil shocks.

Commodity-linked currencies like the Canadian dollar and Norwegian krone sit at the intersection of these forces. On the one hand, higher oil prices improve their terms of trade, which can support the currency and local energy sectors. On the other, global risk aversion and a stronger US dollar can offset or even overwhelm that benefit. The net result depends on the balance between commodity fundamentals and broader risk sentiment at any given time.

In futures markets, traders adjust positioning in oil, interest-rate, equity, and FX contracts to reflect both the new inflation narrative and evolving geopolitical scenarios. Volatility tends to rise as uncertainty about growth, policy, and earnings increases, which can amplify moves in both directions.

Key takeaway: The same oil and geopolitical shock can boost some assets (energy, safe havens) while hurting others (growth equities, EM FX), creating a landscape of relative winners and losers.

Practical Takeaways For Traders

For traders and investors—whether live or in a simulated environment—the current backdrop underscores the importance of a macro-aware approach. Three pillars are particularly important to monitor:

First, track the oil market itself. Watch not just spot prices for benchmarks like Brent and WTI but also the futures curve shape (contango vs backwardation), inventory data, and implied volatility. These indicators provide clues about whether the market is pricing a short-term scare or a longer-lasting structural shock.

Second, follow geopolitical developments with a focus on their economic channels. Headlines about conflict risk are important, but what really matters for markets is whether shipping lanes, production facilities, or sanctions regimes are directly affected. Disruptions to the Strait of Hormuz, for example, have much larger implications than isolated incidents elsewhere[3].

Third, pay close attention to interest-rate expectations. Observe how many cuts are priced into policy-rate futures, how real yields behave, and how central-bank communication evolves in response to incoming data. The link between oil, inflation, and rate expectations is the core mechanism through which geopolitical shocks spill into broader risk assets.

In a SimFi or practice-trading context, this environment is an opportunity to stress test strategies. Traders can:

- Explore how their portfolios behave under scenarios of sustained $90–$100 oil versus a swift retracement.

- Study past episodes of energy and geopolitical shocks—such as prior Middle East crises—to understand typical cross-asset correlations.

- Experiment with hedging approaches using options, safe-haven FX, or sector rotation (for example, balancing growth exposure with energy and defense names).

Key takeaway: Treat the current episode as a live case study in macro risk management—use it to refine your playbook for linking oil, inflation, policy expectations, and cross-asset price action.