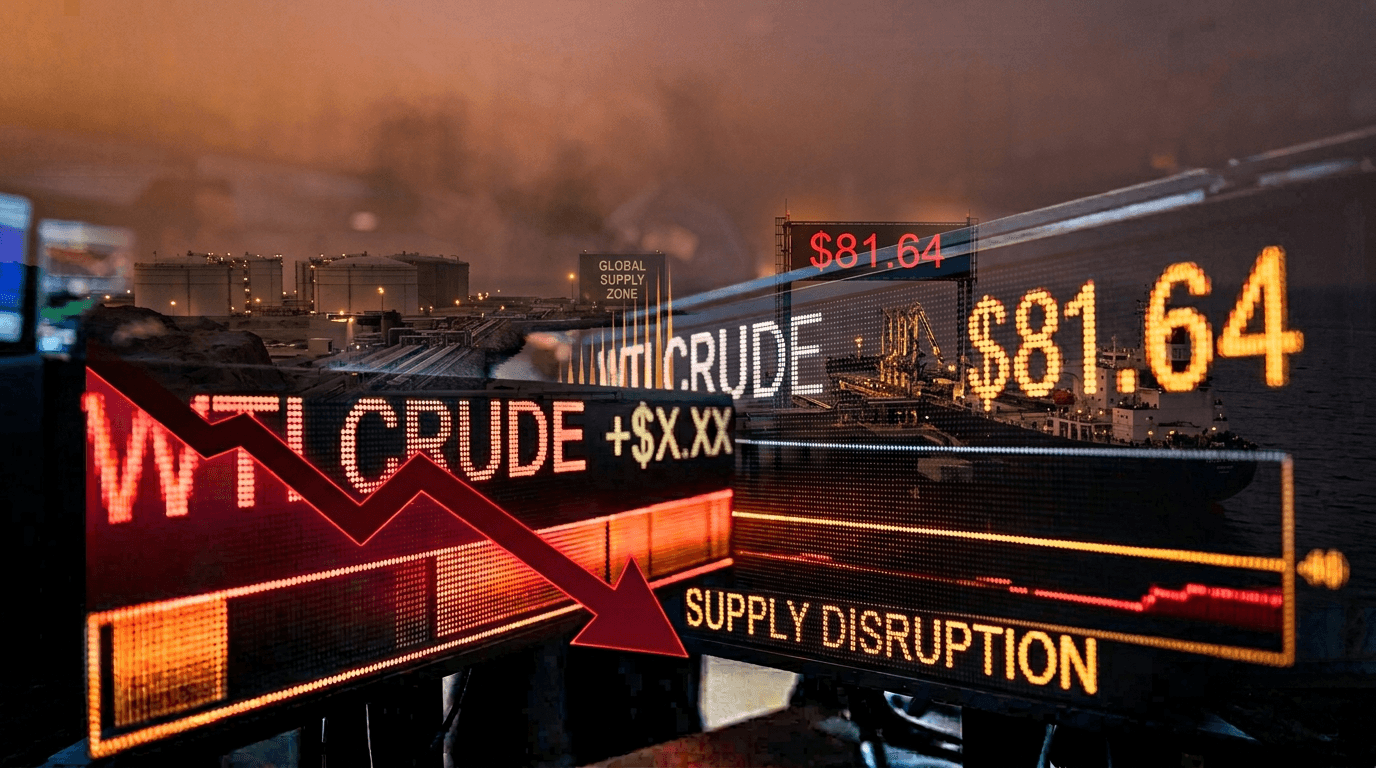

Oil prices have surged nearly 9% to $81.64 per barrel, marking their highest levels since summer 2024. This surge is driven by escalating military tensions between the United States and Iran, which have transformed geopolitical tensions into a significant economic crisis. Unlike typical market speculation, this is a real supply disruption impacting equity markets, consumer spending, and inflation expectations globally. For traders and investors navigating the market landscape in 2026, understanding the intricacies of this energy crisis and its ripple effects on financial markets is crucial for effective portfolio management and risk assessment.

The Supply Shock Unravels

The surge in oil prices originates from an unprecedented disruption centered in the Middle East. U.S. airstrikes on Iran, now in their second week, have led to retaliatory attacks targeting essential oil infrastructure and vessels in vital shipping lanes. The most significant disruption is occurring at the Strait of Hormuz, a narrow passage that facilitates the flow of approximately 20% of the world's daily oil supply. With tanker traffic at a complete standstill due to military tensions, this strategic chokepoint has become the focal point of a global energy crisis.

Analysts estimate that these military actions have collectively removed between 10 and 11 million barrels per day from global circulation, accounting for roughly 10% of the daily global supply in a market that typically trades around 100 million barrels daily. To underscore the severity, consider that Asian refiners are paying record premiums for alternative crude sources, with Norwegian Johan Sverdrup crude trading at an $11.80 premium over Brent crude. These extreme spreads reflect genuine scarcity rather than market speculation, highlighting the depth of supply constraints facing the market.

The benchmark shifts in crude contracts further emphasize the extent of the disruption. Brent crude has risen to $85.85 per barrel, while West Texas Intermediate has surged 11% to $111.60. The magnitude of these moves suggests that markets are anticipating a prolonged period of elevated energy costs rather than a temporary spike.

Market Fallout

Financial markets have reacted sharply to this supply shock. The Dow Jones Industrial Average fell 2.25% as investors grappled with the implications of sustained high energy prices, while the S&P 500 and Nasdaq each dropped over 1%. Airlines, already vulnerable due to Middle East tensions, faced particularly harsh sell-offs as rising fuel costs compounded their operational challenges.

This market reaction reflects a fundamental economic principle: rising oil prices increase business input costs across sectors while simultaneously reducing consumer spending power. Energy-intensive industries face margin compression, while consumer discretionary spending contracts as households allocate more of their budgets to transportation and heating costs. The breadth of the selloff indicates that investors recognize this is not an isolated risk but a systemic challenge affecting earnings across multiple sectors.

For traders, this environment demands careful sector rotation and heightened attention to hedging strategies. Companies with strong pricing power may maintain margins, while those dependent on energy-intensive operations face profitability headwinds.

Inflation And Central Bank Implications

Energy costs function as one of the fastest transmission mechanisms for inflation throughout the broader economy. At the pump, this reality is immediate and painful. U.S. gasoline prices have surged to $3.25 per gallon, a 9% increase from $2.98 just one week earlier. In mid-March readings, some areas reached $3.58 per gallon, with particularly affected regions now seeing prices exceeding $4 per gallon, levels not seen since August 2022.

This rapid repricing of energy impacts inflation expectations and central bank policy expectations. Treasury yields have risen sharply as inflation expectations shift upward. The market now anticipates that prolonged high oil prices could hinder central banks' ability to cut interest rates, placing policymakers in the difficult position of balancing inflation control against growth support. This dynamic is reducing expectations for Federal Reserve rate cuts, fundamentally altering the investment landscape for traders and portfolio managers.

Trader Implications And Takeaways

Policymakers are responding with coordinated measures, though their effectiveness remains uncertain. The International Energy Agency announced a record release of 400 million barrels from strategic reserves, with the U.S. releasing 172 million barrels from its Strategic Petroleum Reserve over four months. OPEC has committed to increasing output by over 200,000 barrels per day in April, though doubts remain about the market's ability to absorb these interventions effectively.

The critical question for investors is whether this represents a temporary shock or the onset of a prolonged period of elevated oil prices. If crude approaches and maintains the $100 per barrel level, analysts warn the global economy may struggle under the weight of the impact. For traders and investors, this moment demands vigilant portfolio management and close attention to Middle East developments. Consider adjusting energy exposure, reviewing hedging strategies, and reassessing duration risk in fixed income positions as rate cut expectations compress.