Oil Market Turmoil: A New Era of Energy Uncertainty

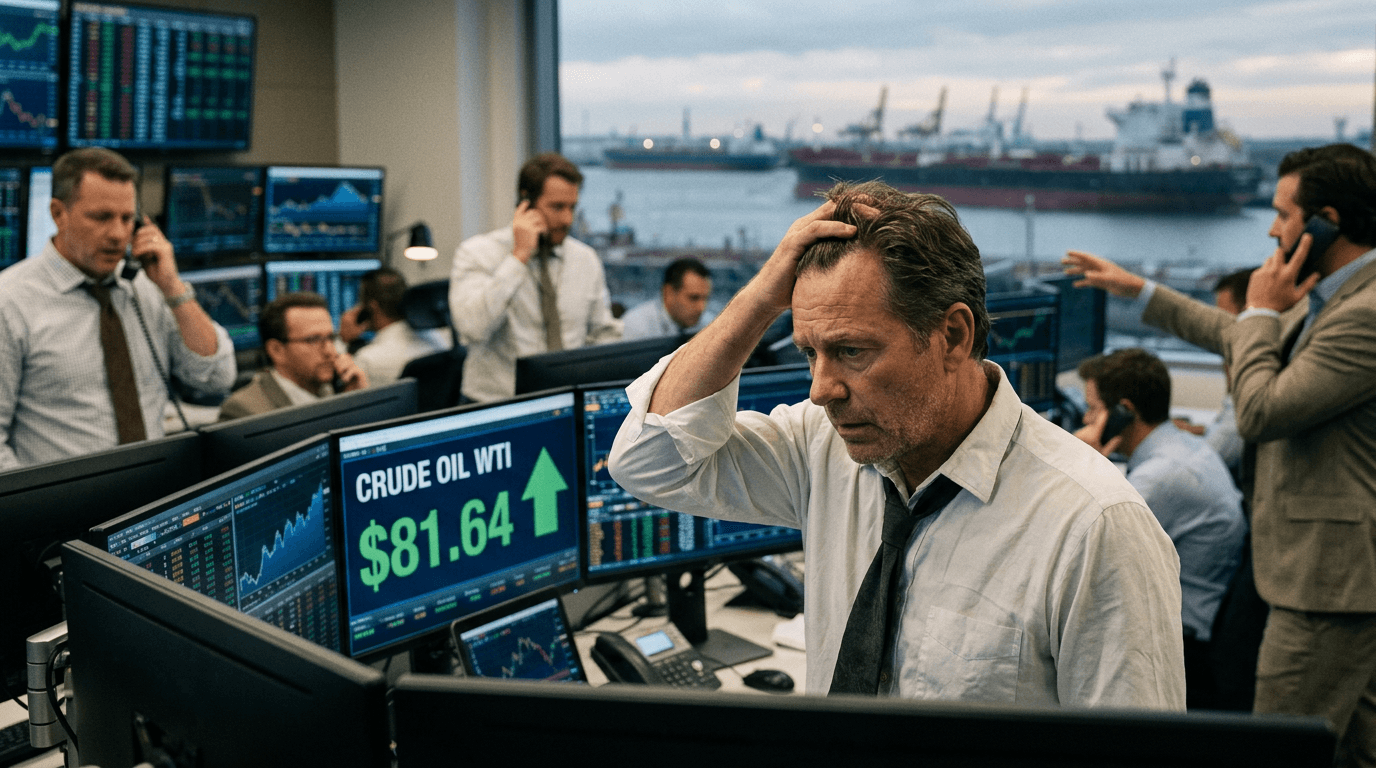

The global oil market is undergoing a profound transformation, drawing the keen attention of traders, investors, and market participants alike. Crude oil has surged nearly 9%, reaching $81.64 per barrel—its highest point since the summer of 2024—while Brent crude has climbed to $85.85 per barrel. This is not just a fleeting market anomaly; it is a genuine supply shock, triggered by the escalating military conflict between the United States and Iran, which is fundamentally reshaping energy markets and sending waves through the broader financial system.

The Geopolitical Catalyst Reshaping Energy Markets

This dramatic price surge is rooted in the intensifying military tensions in the Middle East. Iranian forces have targeted key oil infrastructure and vessels in vital shipping lanes, while U.S. airstrikes against Iran have entered their second week. This situation has shifted the energy landscape in ways that prior oil price spikes, driven solely by speculation, could not.

The most significant development is Iran's effective closure of the Strait of Hormuz, a critical chokepoint accounting for about 20% of the global oil supply. This is not a theoretical risk—real infrastructure damage and port shutdowns are causing authentic supply disruptions that markets cannot ignore. Additionally, Iranian actions have impaired the nation's oil refineries, with facility owners indicating their inability to fulfill existing supply contracts, exacerbating the crisis.

Unlike past oil shocks rooted in market psychology, the current surge is anchored in tangible disruptions to critical energy infrastructure. This distinction is crucial for traders assessing the sustainability and trajectory of elevated energy prices.

Quantifying the Supply Shock

The scale of the disruption is immense. Analysts estimate that U.S. and Iranian military actions have removed approximately 10 to 11 million barrels per day from global markets. In a global context where about 100 million barrels trade daily, this represents a 10% disruption to global oil supply—a shock of monumental magnitude that cannot be easily absorbed by spare capacity or alternative sources.

The physical stress signals emerging from crude markets underscore the severity of this situation. Asian refiners are paying unprecedented premiums for alternative supplies to ensure energy access. Norwegian Johan Sverdrup crude, a key light sweet crude source for Asian markets, is trading at a record premium of $11.80 per barrel over Brent—a clear indicator of buyers' desperation to secure available supply.

Supply constraints facing major producers further amplify current disruptions. Norway, a critical supplier of light sweet crude to Asia, is operating at maximum capacity with no spare production capability. U.S. shale producers, while increasing drilling activity, face capital discipline and supply chain bottlenecks that limit their ability to rapidly boost output. These structural limitations mean supply cannot quickly rebound, establishing a floor beneath oil prices until geopolitical tensions resolve.

The Inflation Transmission Mechanism

Higher energy costs are one of the quickest ways to transmit inflation into broader consumer prices, and this is already happening across the U.S. economy. Average gasoline prices have spiked significantly to $3.25 per gallon, reflecting a 9% increase from $2.98 just one week prior. More concerningly, prices reached $3.58 per gallon by mid-March—a 60-cent surge in a single month—with some regions witnessing prices surpass $4 per gallon, levels not seen since August 2022.

This rapid acceleration in energy prices threatens to reignite inflation concerns that had been gradually moderating, potentially forcing central banks to maintain restrictive monetary policies longer than previously anticipated. For households already navigating elevated cost-of-living pressures, rising gasoline and heating fuel costs directly constrain discretionary spending at a moment when the economy requires sustained consumer demand to support growth.

Government Interventions and Market Outlook

Authorities are actively attempting to stabilize energy markets through strategic interventions. The International Energy Agency has announced that its member countries will release a record 400 million barrels of oil from strategic reserves, with the United States contributing 172 million barrels from its Strategic Petroleum Reserve over a four-month period. This coordinated release represents an extraordinary policy response designed to offset supply disruptions and moderate price increases.

However, these interventions face inherent timing challenges. Strategic petroleum reserve releases operate over months while geopolitical tensions can escalate or deescalate on shorter timeframes. Should oil prices climb toward $100 per barrel and sustain that level, analysts warn the global economy could struggle to absorb the impact. Government officials have expressed optimism that prices will decline, though no definitive timeline exists for how long military conflict may persist.

Key Takeaways for Market Participants

Several critical insights emerge from this market environment. First, genuine supply disruptions—not merely speculation—are driving current oil dynamics, lending credibility to sustained elevation in energy costs. Second, inflation implications challenge recent narratives about economic softness and supportive monetary policy. Third, equity market weakness reflects legitimate stagflation concerns rather than temporary volatility. Finally, government interventions through strategic reserve releases provide meaningful support but cannot resolve underlying geopolitical risks that remain the primary price driver.

Traders navigating this landscape must remain alert to both the supply fundamentals and geopolitical developments shaping energy markets in real time.

NEWSIMPACTSCORE: 8