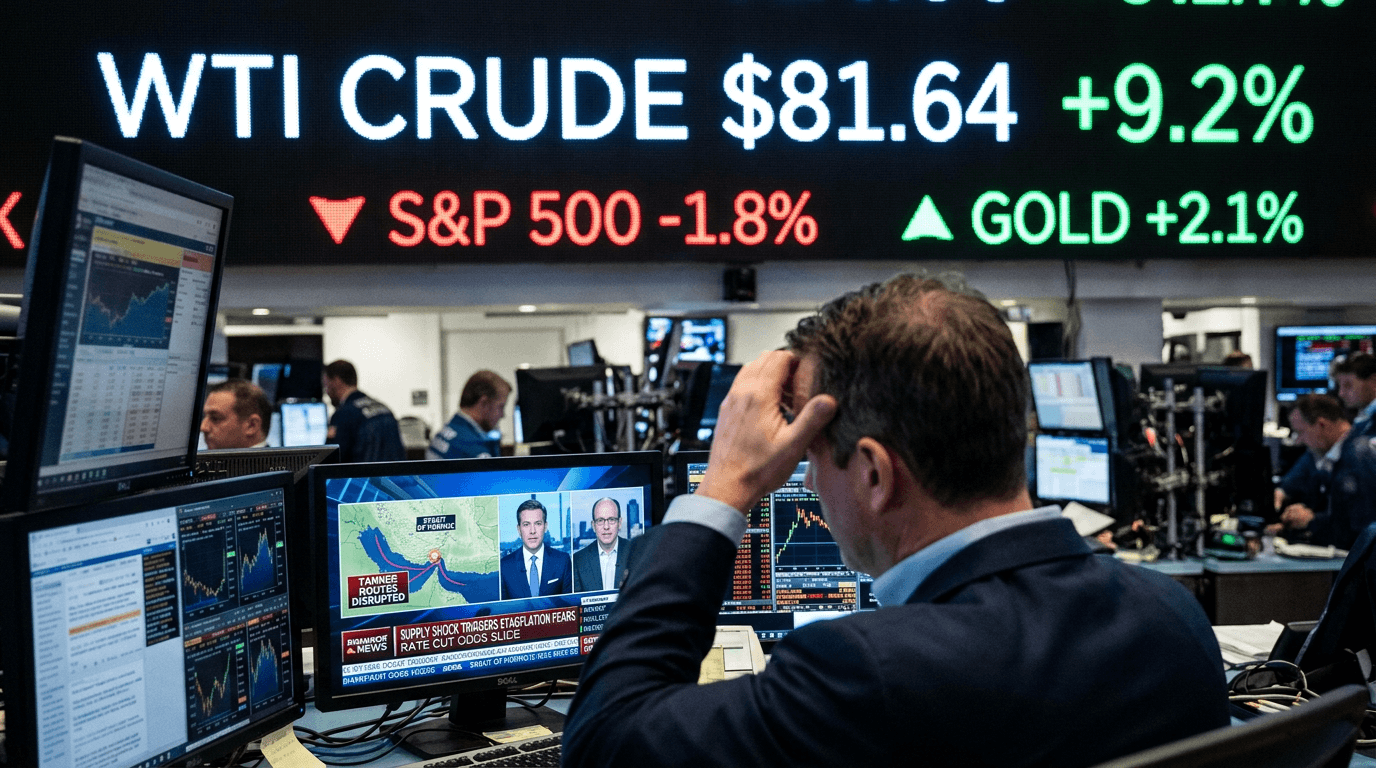

The global oil market is undergoing a seismic shift as crude prices skyrocket to heights not seen since summer 2024. West Texas Intermediate crude has surged nearly 9% to $81.64 per barrel, while Brent crude has risen to $85.85. This sharp rise marks a critical juncture for traders, investors, and market participants who now face an energy landscape fundamentally altered by geopolitical tensions. This surge is not driven by speculative trading but by an authentic supply crisis caused by escalating military tensions between the United States and Iran. Understanding the implications of this situation is crucial for anyone involved in financial markets today.

The Perfect Storm: What's Driving Oil Prices

The rapid increase in oil prices is a direct consequence of heightened military conflict in the Middle East. Iranian forces have targeted vital oil infrastructure and vessels in strategic shipping lanes, while U.S. airstrikes against Iran have continued for a second week. This sustained uncertainty keeps energy markets in a state of heightened tension. The closure of the Strait of Hormuz by Iran, a chokepoint responsible for about 20% of the world's daily oil supply, is the most significant development. This is not a speculative risk—it represents a real disruption to essential trade routes at a time when the global energy system is ill-prepared to handle such shocks.

The scale of this disruption is immense. Analysts estimate that military actions by the U.S. and Iran have removed approximately 10 to 11 million barrels per day from global markets. In a world where around 100 million barrels trade daily, this equates to a disruption of roughly 10% of global oil supply—an enormous shock that cannot be easily mitigated by spare capacity or alternative sources.

The Real Supply Shock: Not Speculation

What sets this oil price surge apart from previous spikes is the fundamental nature of the disruption. Unlike past events driven by market psychology or speculative trading, the current price increase is due to physical disruptions to critical energy infrastructure. Iranian military actions have compromised the country's oil refineries, leaving facility owners unable to fulfill existing supply contracts, worsening the crisis.

The physical crude market is under significant strain, as evidenced by premium pricing for alternative supplies. Asian refiners are paying unprecedented premiums for non-Iranian crude, with Norwegian Johan Sverdrup crude trading at a record premium of $11.80 per barrel over Brent. This stark indicator of buyer desperation reflects genuine scarcity concerns, not speculative positioning, suggesting that energy markets are pricing in sustained supply constraints rather than temporary volatility.

Inflation And Broader Market Ripple Effects

The ramifications extend far beyond oil markets. Higher energy costs are one of the quickest ways for inflation to infiltrate broader consumer prices, and this is already happening across the U.S. economy. Average gasoline prices have surged to $3.25 per gallon, a 9% increase from $2.98 just a week earlier. More alarmingly, prices hit $3.58 per gallon by mid-March—a 60-cent jump in a single month—with some regions seeing prices exceed $4 per gallon, levels not observed since August 2022.

These increased energy costs pose a significant challenge to recent narratives of economic softness and supportive monetary policy. Should oil prices approach $100 per barrel and maintain that level, analysts caution that the global economy could struggle to cope. This scenario—where inflation pressures persist amid economic uncertainty—might compel central banks to keep rates higher for longer, contradicting market expectations for near-term rate cuts.

Navigating Uncertainty: Key Takeaways For Traders

Several crucial insights can be drawn from this environment. First, genuine supply disruptions are driving current oil dynamics, supporting sustained elevation in energy costs rather than positioning this as a temporary anomaly. Second, the inflation implications challenge recent narratives of economic softness, potentially reshaping expectations around monetary policy trajectories. Third, equity market weakness reflects legitimate stagflation concerns rather than temporary volatility.

Government interventions through strategic petroleum reserve releases provide meaningful support but face inherent timing challenges. These releases operate over months while geopolitical tensions can escalate or deescalate on shorter timeframes, creating a mismatch between policy response speed and market reality. Government officials have expressed optimism that prices will decline, though no definitive timeline exists for how long the military conflict may persist.

Looking Ahead

Market participants must acknowledge that this energy shock carries genuine consequences for portfolio construction, inflation expectations, and central bank policy trajectories. Differentiating between speculative volatility and real supply disruption is crucial for assessing how long elevated energy prices will persist. Traders should monitor both the geopolitical situation and government interventions as dual drivers of near-term oil price direction, while recognizing that the primary price driver remains the unresolved geopolitical conflict itself.

---