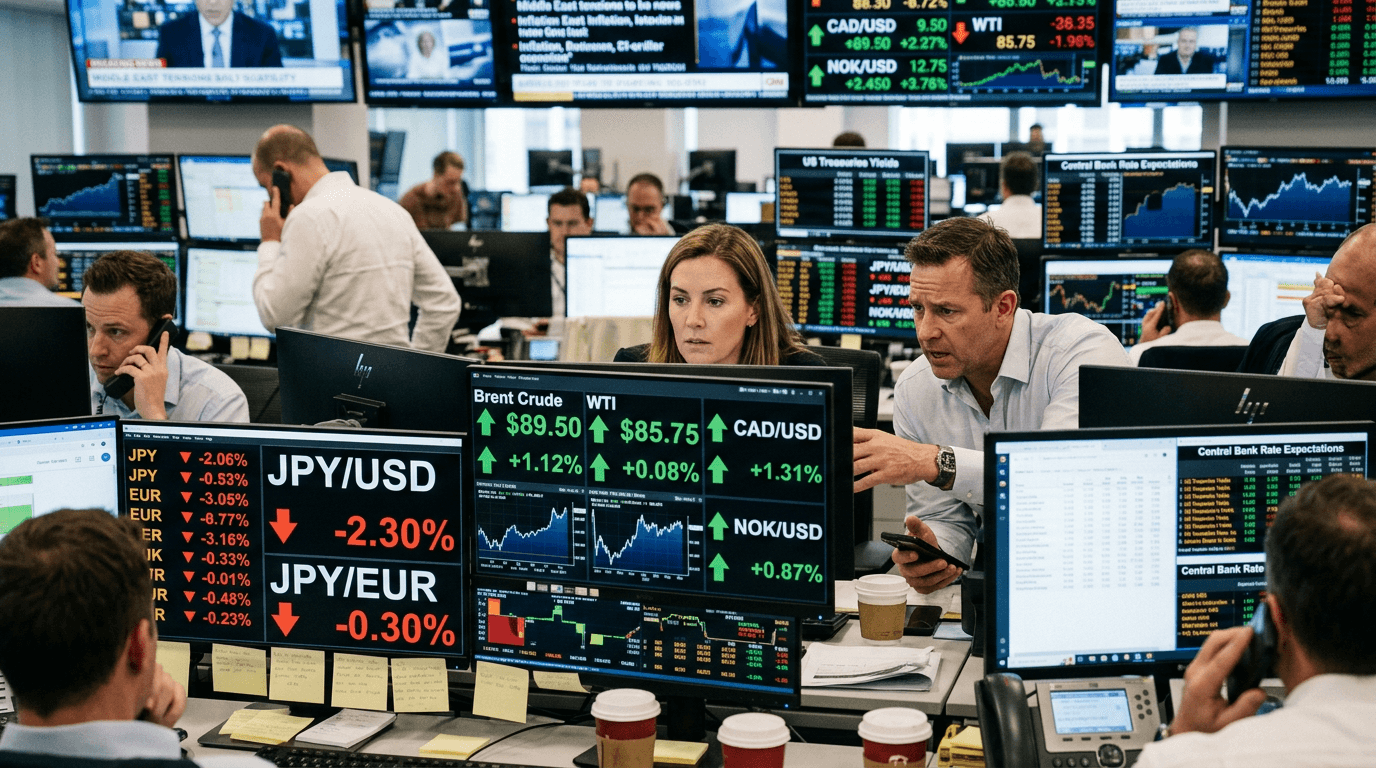

Oil markets are back in focus as renewed tensions in the Middle East push crude futures higher, reviving the familiar link between geopolitics, energy prices, and currency moves.[1][4] Brent and WTI contracts have extended gains after recent headlines raised the risk of a broader regional conflict, with prices rebounding from prior lows as supply worries overshadow concerns about global demand.[1][4] In FX, that shift is supporting oil-linked currencies such as the Canadian dollar (CAD) and Norwegian krone (NOK), while weighing on the Japanese yen (JPY) as traders reassess inflation and interest-rate expectations.[2][4]

Market Snapshot: Oil Spikes On Geopolitical Risk

The latest leg higher in crude has been driven less by fundamental changes in supply and demand and more by a renewed geopolitical risk premium.[1][4] Reports of escalations involving key regional actors have revived fears of disruptions to energy flows from the Middle East, still the world’s most strategically important oil-producing region.[1][4] Futures rebounded after a sharp selloff earlier in the week, with Brent and WTI recovering from multi-month lows as traders moved to reprice tail risks around supply.[1][4] In some recent episodes, front-month WTI crude has even traded near the high-$90s per barrel when geopolitical fears have intensified, underscoring how quickly risk premia can re-enter the market.[2]

For traders, the message is clear: when geopolitical stress touches a major energy corridor, oil often reacts first, and FX and rates follow. Takeaway: Treat Middle East headlines as a cross-asset catalyst, not just an oil-market story.

Why Cad And Nok Tend To Rise With Oil

Canada and Norway are among the developed world’s most prominent net oil exporters, so their currencies often behave like leveraged plays on crude prices. Higher oil typically improves their terms of trade, boosts energy-sector revenues, and can support fiscal balances, all of which tend to be positive for CAD and NOK over time.[4] When futures jump on supply fears, markets often anticipate stronger export receipts and potentially firmer growth in these economies, leading to capital inflows into local assets and stronger currencies.

That dynamic has been visible in the latest move, with traders rotating into CAD and NOK as crude rallied on renewed Middle East tensions.[4] Even if the direct volume of exports does not change overnight, the improved pricing power of oil producers can lift earnings expectations and widen interest-rate differentials if local central banks lean more hawkish on inflation risks. Energy equities listed in Toronto and Oslo can also become more attractive, adding another channel through which portfolio flows support the currency.

Of course, the oil–FX link is not perfect. Broader risk sentiment, domestic data, and central bank guidance can all overwhelm the oil signal at times. But during sharp, headline-driven crude rallies, CAD and NOK often sit near the top of the G10 performance table. Takeaway: When oil spikes on supply fears, expect CAD and NOK to be among the primary FX beneficiaries, especially if risk sentiment is stable or improving.

Why Jpy Struggles When Oil And Yields Rise

Japan sits on the other side of the energy spectrum as a major net importer of crude and liquefied natural gas. When oil prices rise, Japan’s import bill increases, worsening the trade balance and putting additional pressure on corporate margins and consumers. That can weigh on the yen, as markets anticipate a deterioration in external balances and potentially more inflation imported via higher energy costs.

At the same time, renewed inflation concerns from higher oil prices can push up global bond yields as investors demand more compensation for inflation risk.[3][4] Higher U.S. and European yields typically widen rate differentials against Japan, where policy has remained much more accommodative, even as the Bank of Japan gradually normalizes.[3] This makes the yen less attractive in carry terms and often encourages renewed JPY-funded carry trades into higher-yielding currencies, especially when risk appetite is not collapsing.

The result is a double headwind: Japan pays more for energy and faces wider interest-rate gaps versus peers, while safe-haven demand for JPY may be limited if risk sentiment remains broadly constructive. Takeaway: In environments where oil and global yields are rising together, JPY often underperforms, particularly against commodity and high-yield currencies.

Inflation Expectations, Central Banks, And Rate-cut Hopes

Higher oil does not automatically translate into persistently higher inflation, but it tends to lift near-term inflation expectations, especially headline CPI measures that include energy.[4] After a year-plus of aggressive tightening cycles, major central banks remain highly sensitive to any sign that price pressures could prove more stubborn than hoped. When crude futures jump on geopolitical tensions, markets often price in fewer or later rate cuts, reflecting the risk that policymakers will stay cautious.

Recent price action has followed this pattern: as oil futures extended gains on Middle East tensions, traders scaled back expectations for imminent easing, particularly in economies already wrestling with sticky services inflation.[4] In North America and Europe, that “higher-for-longer” narrative can support local yields and currencies, especially for oil exporters like Canada and Norway. By contrast, for energy importers such as Japan, higher oil means more imported inflation but not necessarily more BoJ tightening, given the focus on wage dynamics and underlying trend inflation.[3]

This divergence matters for FX. If markets think the Bank of Canada or Norges Bank might lean slightly more hawkish at the margin while the BoJ remains cautious, the policy spread continues to favor CAD and NOK over JPY. Takeaway: Rising oil that lifts inflation expectations tends to delay global rate-cut timelines, reinforcing support for oil-exporter currencies over oil-importer currencies.

Trading Takeaways For Simulated Fx And Oil Strategies

For traders working in a simulated environment, this episode offers a clean case study in cross-asset linkage. One approach is to map a simple framework: geopolitical shock → oil futures higher → inflation expectations up → rate-cut probabilities down → FX rotations into oil-sensitive exporters and away from energy importers. By tracking how each leg of that chain evolves in real time, traders can build scenarios and test how robust their strategies are to sudden shifts in risk sentiment.

On the directional side, simulated traders might explore expressing a bullish oil view via long CAD or NOK versus JPY, reflecting both the commodity and interest-rate narratives. Risk management remains critical: if geopolitical tensions suddenly ease or cease-fire prospects improve, oil’s risk premium can unwind quickly, reversing the FX moves. Combining technical levels on oil and FX pairs with macro triggers—such as central bank speeches or new Middle East headlines—can help refine entries and exits.

Equally important is stress-testing. How would CAD/JPY or NOK/JPY behave if oil moved another 10–15% higher from here versus if it dropped sharply on a de-escalation? How would changing assumptions about future rate cuts in North America, Europe, or Japan alter the picture? Using a simulated framework allows traders to answer these questions without capital at risk, while still learning to connect macro dots under real-world conditions.

Takeaway: Use this oil-driven move as a template to practice linking geopolitics, commodities, inflation expectations, and FX, focusing on how CAD, NOK, and JPY respond across different scenarios.