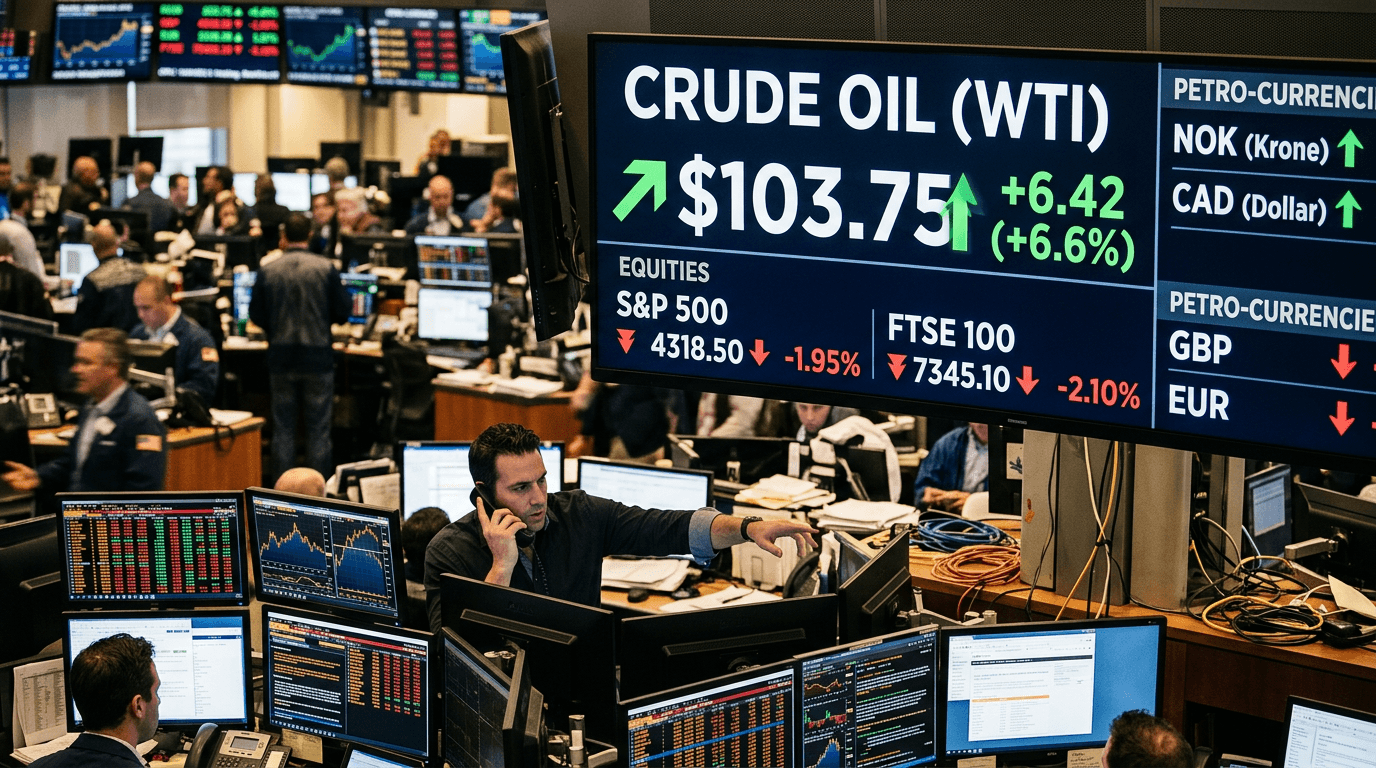

Crude oil’s latest surge is a textbook example of how geopolitics can reprice risk across markets in a matter of hours. As headlines pointed to an intensifying conflict involving Iran, WTI crude jumped roughly 9% intraday to recent highs above $81, with Brent trading above $85.[1][7] The move hit US equities, pressured global risk sentiment, and simultaneously lent support to commodity‑linked currencies such as the Canadian dollar (CAD) and Norwegian krone (NOK) as traders scrambled to adjust to a higher geopolitical risk premium.[1][7]

Geopolitics, Oil And The Risk Premium

When tensions flare in the Middle East, oil markets react first and fastest. The region sits atop a large share of global reserves and includes critical chokepoints such as the Strait of Hormuz, through which around a quarter of global seaborne oil trade passes.[4] Any threat—real or perceived—to those flows immediately shows up in futures prices as a higher risk premium.

That premium is not about today’s barrels alone; it reflects the market’s reassessment of tail risks. Traders quickly ask: Could exports be disrupted? Will shipping lanes be restricted? How might insurance costs and freight rates evolve if the conflict broadens?[4] Even before physical flows are affected, futures curves often steepen, volatility jumps, and hedging demand increases as refiners, producers, and speculators all look to protect themselves.

International institutions have highlighted how war in the Middle East transmits through three main channels: energy prices, supply chains, and financial markets.[7] Higher crude prices can feed into natural gas, fertilizer, and transport costs, with knock‑on effects for global inflation, trade balances, and ultimately growth.[4][7] This is why a “regional” conflict rapidly becomes a global macro story.

Why Higher Oil Pressures Equities

Equity markets dislike sharp, unanticipated jumps in input costs—especially when they come attached to geopolitical uncertainty. As oil breaks higher, investors immediately reassess corporate earnings, inflation trajectories, and central bank paths. Historically, sudden oil spikes have coincided with equity drawdowns, particularly in energy‑intensive sectors.[1]

For corporates, higher energy prices squeeze margins in multiple ways. Manufacturing, transportation, airlines, and consumer goods companies face increased operating costs. If they cannot pass those costs on to customers, profits suffer; if they do, households feel the pinch, dampening discretionary spending. Either way, the earnings outlook looks less favorable.

At the macro level, more expensive energy can re‑ignite inflation concerns just as many central banks are trying to pivot from tightening to easing. If policymakers worry that the oil shock could become entrenched in broader prices and wages, they may delay rate cuts or even hint at renewed tightening. That combination of weaker growth prospects and potentially higher-for-longer interest rates typically weighs on equity valuations.

The impact is not uniform across the stock market. Energy producers, oilfield services, and some commodity‑linked infrastructure assets may benefit from higher prices and stronger cash flows. In contrast, cyclical sectors sensitive to consumer demand and capital spending—such as autos, industrials, and small caps—tend to underperform. For index traders, this makes sector rotation just as important as directional index views.

HOW COMMODITY‑LINKED FX BENEFITS

While risk‑off episodes usually support classic safe havens like the US dollar, the Swiss franc, and the Japanese yen, this particular shock has also boosted select commodity‑linked currencies. The CAD and NOK, for example, tend to strengthen when oil rallies because their economies are major energy exporters and their terms of trade improve.[1][7]

The logic is straightforward. Higher export prices increase national income, improve current account balances, and can attract foreign capital into local bond and equity markets. Investors anticipating stronger fiscal revenues and potentially more resilient growth in these economies often reward their currencies. In some cases, central banks in commodity exporters may even lean less dovishly if higher resource revenues support activity.

However, the story is nuanced. If the geopolitical shock morphs into a full‑blown global risk‑off event—triggering severe equity selling and credit stress—high‑beta commodity currencies can still underperform the US dollar, which remains the world’s primary safe haven. In that scenario, relative performance among commodity FX often depends on:

- The scale of each country’s net energy exports

- External vulnerabilities (current account deficits, FX reserves)

- Domestic inflation and central bank credibility

Meanwhile, large energy importers such as Japan, India, and much of Europe face a deteriorating terms‑of‑trade backdrop when oil spikes, which can weaken their currencies and widen trade deficits. This divergence is precisely why FX markets move so sharply in response to commodity shocks.

Trading A Geopolitical Oil Shock

For traders, a move like this is not simply an “oil trade”—it is a cross‑asset volatility event. Understanding the transmission chain is crucial: geopolitics → oil → inflation and growth expectations → central bank pricing → equities, bonds, and FX.[1][7] Each link in that chain offers potential opportunities and risks.

In practice, this means monitoring:

- Futures curves and volatility in WTI and Brent for signs of whether the move is priced as temporary or structural.

- Equity sector dispersion, especially the gap between energy and energy‑intensive industries.

- Rate expectations and bond yields as markets reassess the path of monetary policy.

- Relative FX performance, focusing on petro‑currencies versus energy importers.

Risk management becomes paramount during such episodes. Gaps, slippage, and headline‑driven spikes can challenge tight stops and high leverage. Diversification across asset classes, disciplined position sizing, and scenario planning all help traders avoid turning a macro shock into a portfolio‑level crisis.

Simulated trading environments are particularly useful for stress‑testing strategies against these kinds of shocks. By replaying past periods of geopolitical stress and experimenting with different hedging approaches, traders can build intuition around how their systems behave when correlations break down and volatility clusters.

Key Takeaways For Active Traders

Oil’s spike on Middle East escalation is a reminder that markets are not driven by economic data alone; geopolitics can rewrite the script in a single session. The key is to think in terms of linkages rather than isolated moves. When a headline hits crude, it is simultaneously sending signals about inflation risks, central bank flexibility, corporate earnings, and currency realignments.

For equity traders, that means looking beyond the index level to sector dynamics and considering whether the shock is likely to be short‑lived or persistent. For FX traders, it means differentiating between exporters and importers, and between fundamentally strong and vulnerable commodity currencies. For macro and cross‑asset traders, it means using oil as a barometer for broader risk sentiment and being ready to adjust exposure quickly.

Above all, events like this underscore the value of preparation. Having predefined playbooks for geopolitical shocks—what to watch, how to adjust, and where your portfolio is most exposed—can turn a chaotic tape into a more structured set of opportunities. Whether in live or simulated markets, the traders who navigate these episodes best are usually those who understand not just that oil is up, but why that move matters for every other asset they trade.