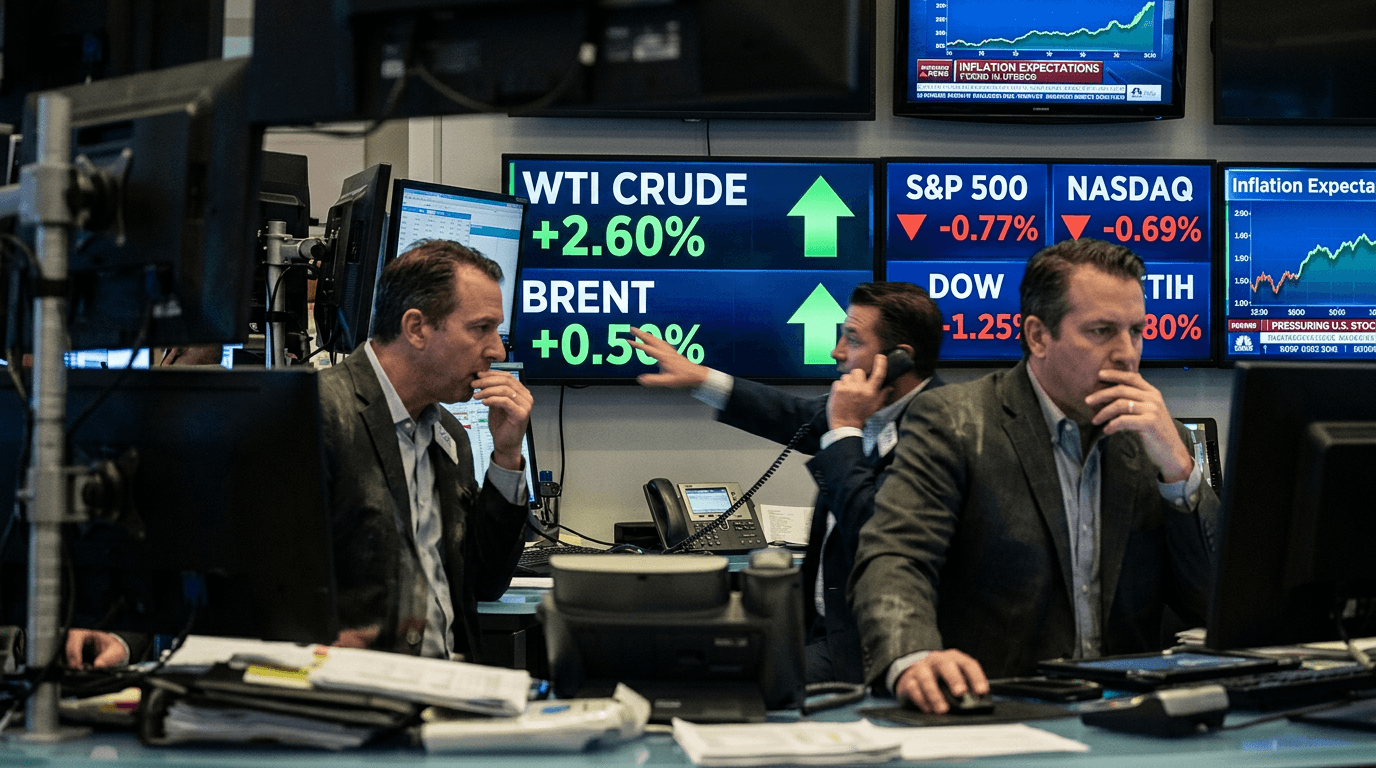

Oil markets have lurched higher again as renewed conflict fears in the Middle East ripple through global assets, knocking U.S. stocks and equity index futures off balance. With U.S. crude jumping to around $81.64 and Brent nearing $86 a barrel on war-related headlines involving Iran, traders are quickly repricing everything from risk appetite to inflation expectations. Higher energy costs are reviving concerns that last year’s inflation battle may not be fully over, even as growth worries remain in the background.[1][4]

Markets React To A Fresh Oil Price Shock

The Middle East remains the world’s most strategically important oil basin, so any sign of escalation there tends to inject a “risk premium” into crude prices.[2][3] Even before supply is actually disrupted, markets price the probability that physical flows could be constrained, particularly through key chokepoints like the Strait of Hormuz.[3][6]

Recent headlines tied to the war with Iran have done exactly that: pushed oil sharply higher and pulled U.S. equities lower as investors reassess the balance of risks.[1][4] Historically, similar episodes of geopolitical tension have triggered a familiar pattern—energy prices spike, global stock indices retreat, bond yields climb on renewed inflation fears, and volatility rises across asset classes.[4][5] This time is no different, but it lands in a market already sensitive to central bank policy, growth data, and earnings quality.

Analysts have long warned that a serious conflict involving Iran could quickly propel oil into the $80–$100 range, even with partial disruptions or temporary transit delays.[3] The latest move into the low 80s for U.S. crude and mid-80s for Brent sits squarely in that risk band and keeps traders focused on whether this is a short-lived shock or the start of a more prolonged energy squeeze.

Why Oil Spikes Hit Stocks And Futures Sentiment

Oil is not just another commodity; it is a core input into transportation, manufacturing, logistics, and agriculture. When crude prices jump, corporate costs rise and profit margins can compress, particularly for energy-intensive industries.[2] That margin pressure tends to weigh on equity valuations, especially when companies have limited ability to pass higher costs on to consumers.

At the macro level, higher oil prices function like a tax on consumers and oil-importing economies, leaving households with less disposable income and potentially slowing demand.[5] This can feed into weaker growth expectations, which are already a key driver of equity index futures pricing. When traders see both higher inflation risk and softer growth, risk appetite usually falls, pressuring indices like the S&P 500 and Nasdaq.

The policy channel is just as important. A fresh energy-driven inflation pulse may keep central banks wary about cutting rates too quickly.[4][5] ING and the IMF both highlight that conflict-related energy shocks tend to worsen trade balances, lift inflation, and push bond yields higher, all of which can undermine equity valuations and make “risk-free” assets relatively more attractive versus stocks.[4][5]

Sector Winners And Losers In An Oil-driven Sell-off

Geopolitical oil spikes rarely hit all sectors equally. Energy producers and some commodity-linked businesses often benefit from higher realized prices, improved cash flows, and stronger earnings expectations.[2][5] In contrast, fuel-intensive sectors such as airlines, shipping, logistics, and parts of consumer discretionary tend to suffer as costs rise and demand may slow.

Global analysis of past Middle East conflicts shows that economies and companies heavily reliant on imported energy generally face more pressure, while net exporters can see temporary windfalls.[2][5] This dynamic can influence style and regional rotations: investors may tilt toward value and dividend payers in resource-rich markets while scaling back exposure to energy-dependent, import-heavy regions.

Defense and aerospace can also see renewed interest during periods of heightened geopolitical risk, as markets anticipate higher government spending and stronger order books.[1] At the same time, high-growth, long-duration assets—like unprofitable tech names—often come under pressure when bond yields rise on the back of higher inflation expectations.[4][5] For index futures, the net result is typically a negative impulse, since the losers by market cap often outweigh the winners.

What This Means For Inflation, Rates, And The Macro Outlook

The IMF notes that a short conflict can send oil and gas prices sharply higher before markets eventually adjust, while a prolonged one can keep energy costs elevated and strain both growth and financial stability.[4] In either case, the initial impact is stagflationary: higher prices, weaker real incomes, and uncertainty around central bank responses.

ING’s work on prior Middle East shocks underscores that even without direct supply loss, a higher global oil price worsens trade balances for importers and adds to inflation pressure.[5] For central banks that felt they were close to declaring victory over inflation, a renewed energy spike complicates the path: cutting too soon risks re-accelerating prices, but keeping policy tight for longer raises recession risk.

Bond markets often react quickly, pushing yields higher in the front end as inflation risk is repriced, while also pricing in the possibility that growth down the line might slow.[4][5] Equities and futures sit in the crossfire: they must discount both the higher discount rate (negative for valuations) and the potential hit to future earnings from slower growth and higher input costs.

How Traders Can Navigate Geopolitical Oil Shocks

For active traders and SimFi participants, episodes like this are a real-time stress test of risk management discipline. Spikes driven by geopolitics are often headline-heavy, prone to rumors, and characterized by sudden gaps in both directions. That makes position sizing, leverage control, and clear exit rules more important than precise prediction.

Historically, the most robust approaches in these environments share a few traits. First, they separate the near-term volatility from the medium-term macro story, asking whether the conflict is likely to cause sustained supply disruption or mostly a temporary risk premium.[3][4] Second, they pay close attention to cross-asset signals: moves in oil curves (such as steep backwardation), bond yields, and volatility indices can offer clues about whether the shock is deepening or fading.[5][6]

Scenario planning also becomes critical. Traders can map out “what if” paths—such as a quick de-escalation, a contained but prolonged standoff, or a broader regional conflict—and consider how each would affect energy prices, inflation expectations, and equity indices. This framework helps prevent emotional, headline-driven decisions and supports more consistent strategy execution.

Looking Ahead

Oil’s latest surge on Middle East conflict concerns is a reminder that geopolitics can override calm market narratives in a single news cycle. With crude back in the low-to-mid 80s, equity index futures under pressure, and inflation-sensitive assets in focus, the coming sessions will test whether this is a transient risk flare-up or the start of a more persistent repricing.[1][4]

For investors and traders alike, the key is not trying to forecast every twist in the conflict, but understanding the transmission channels—from energy prices to inflation, policy, and corporate earnings—and positioning portfolios and strategies accordingly. Markets have navigated many geopolitical shocks before; those who combine respect for risk with a clear macro framework are best placed to turn heightened volatility from a threat into an opportunity.