The Indian rupee slipping beyond 96 per US dollar marks a psychological and economic inflection point for Asia’s third-largest economy. A move of this magnitude is not just a headline about currency charts; it is a signal about energy costs, external funding pressures, and the policy choices facing the Reserve Bank of India (RBI). For traders and investors, this is precisely the type of macro environment where risk management, scenario analysis, and an understanding of cross-market linkages become critical.

WHAT IS DRIVING THE RUPEE TO 96 PER DOLLAR?

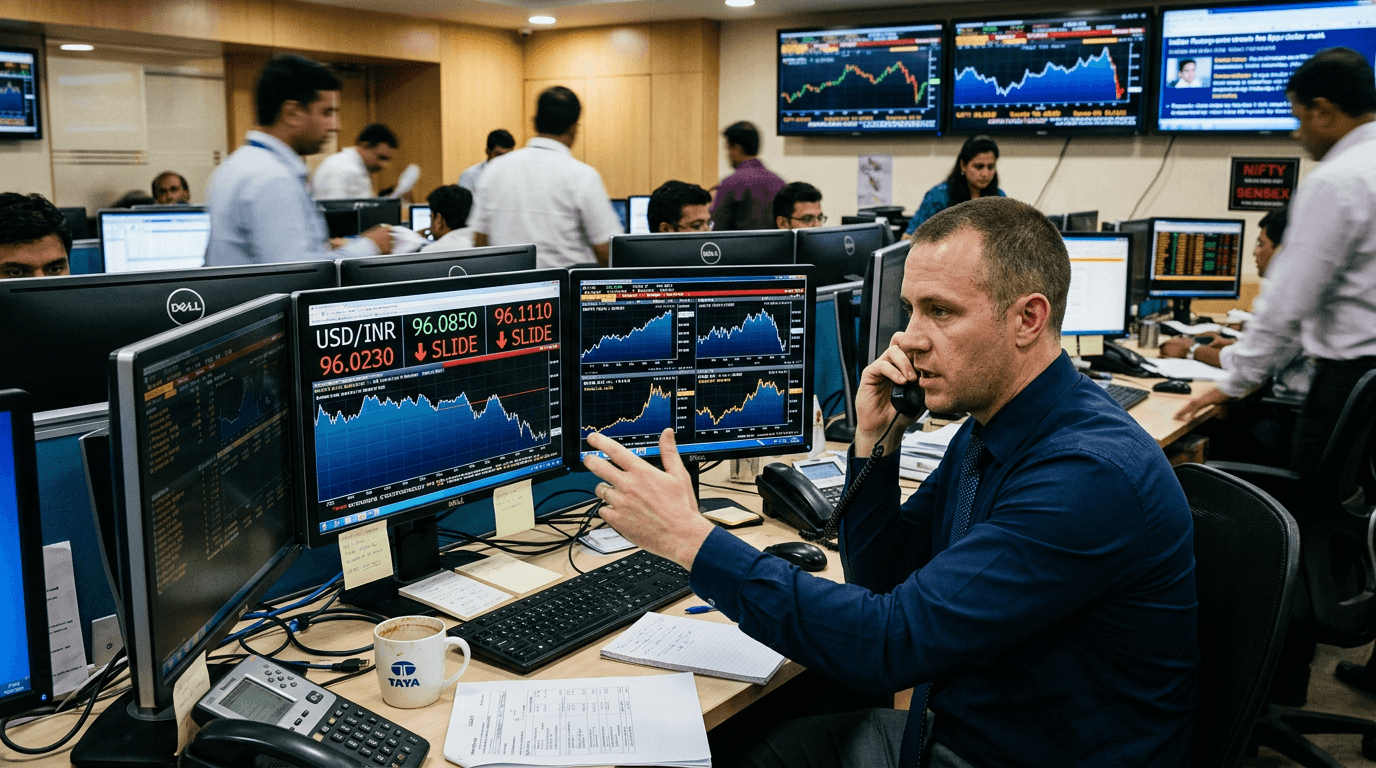

Three forces are converging to push the rupee to fresh record lows: a stronger US dollar, surging crude oil prices, and persistent foreign portfolio outflows.

First, the dollar itself is in a broad uptrend as markets price in a “higher for longer” Federal Reserve stance and seek safe havens amid global uncertainty. When the dollar strengthens broadly—reflected in a firm US Dollar Index (DXY)—most emerging-market currencies come under pressure, and the rupee is no exception.

Second, India is highly dependent on imported energy, with more than four-fifths of its crude oil needs sourced from abroad. When crude prices jump, India’s import bill rises sharply, widening the current account deficit and increasing demand for dollars. Oil marketing companies, airlines, and industrial firms rush to hedge and secure dollars, adding to currency market pressure.

Third, foreign institutional investors have been net sellers of Indian equities and bonds in recent weeks, locking in past gains and reallocating capital to perceived safer or higher-yielding markets. These outflows create a steady supply of rupees and demand for dollars, which, when combined with elevated oil demand, can tip the currency to new lows even if domestic fundamentals remain broadly intact.

Why A Weak Rupee Matters For The Real Economy

A weaker rupee at 96 per dollar quickly translates into higher local prices for imported goods and services. Fuel, fertilizers, cooking gas, and many intermediate inputs become more expensive in rupee terms. Even if the government and oil companies temporarily absorb some of the shock, sustained currency weakness tends to feed into broader consumer price inflation over time.

This imported inflation poses a challenge to the RBI’s inflation-targeting framework. If headline inflation drifts meaningfully above the target band due to currency and commodity shocks, the central bank may be forced to maintain tighter monetary policy for longer, even if growth momentum is softening. That trade-off between controlling inflation and supporting growth becomes more acute as the rupee weakens.

On the external side, a cheaper currency can, in theory, boost exports by making Indian goods more competitive. In practice, the benefit is often diluted because many export sectors—such as electronics, autos, and capital goods—rely on imported components priced in dollars. Meanwhile, a wider current account deficit makes India more reliant on stable capital inflows and raises the cost of dollar borrowing for corporates and financial institutions.

RBI’S TOOLKIT: HOW FAR CAN POLICYMAKERS GO?

The RBI’s immediate priority is typically to ensure “orderly” behavior in the foreign exchange market rather than defend a particular level of the rupee. Its main tool is intervention—selling dollars from its foreign exchange reserves and buying rupees to smooth excessive volatility and prevent disorderly moves.

India’s reserves provide a substantial buffer, but they are not unlimited. Heavy, one-way intervention can quickly deplete reserves, which markets would view as a sign of vulnerability and could even invite speculative pressure. The central bank therefore tends to calibrate its response, leaning against sharp intraday swings and extreme positioning rather than drawing a hard line at any specific level.

Beyond direct intervention, the RBI can deploy interest rate policy and liquidity management. Higher policy rates tend to support the currency by making rupee assets more attractive, but they also raise borrowing costs for households and businesses. The RBI can also adjust macroprudential norms, encourage non-resident deposits, or work with the government to manage the timing of external borrowings, all of which influence dollar flows without overtly targeting the exchange rate.

What This Means For Traders And Investors

For market participants, a rupee at 96 is not just a macro statistic—it reshapes risk-reward profiles across asset classes.

Indian importers with unhedged dollar exposure face higher costs and increased earnings uncertainty. Exporters may see a near-term margin boost, but only if they have sufficient local cost bases and limited imported content. Corporates that actively manage currency risk using forwards and options will have an advantage in navigating this kind of volatility.

Equity investors should reassess sector exposures. Historically, export-oriented IT services, pharmaceuticals, and select manufacturing can benefit from a weaker rupee, while fuel-intensive sectors like airlines, logistics, and certain consumer goods suffer margin compression. Financials must be watched closely: funding costs, asset quality, and market volatility can all shift as the currency slides and interest-rate expectations adjust.

For global FX traders, USD/INR becomes a key macro pair to watch. Liquidity tends to rise during periods of stress, but so does volatility and gap risk around key data releases and policy announcements. Monitoring correlations with Brent crude, the DXY, and broader emerging-market FX can help frame directional and relative-value trades. In a simulated or prop-style environment, these conditions offer rich lessons in position sizing, hedging, and respecting event risk.

SCENARIOS AHEAD: COULD 100 PER DOLLAR BE NEXT?

With the 96-per-dollar level now breached, markets are naturally asking whether the rupee could edge towards 100 in the coming months. The answer depends on how three variables evolve: global risk appetite, crude oil prices, and the policy stance of the Fed and the RBI.

In a benign scenario, oil prices stabilize or ease as supply concerns abate and demand expectations moderate. If US economic data soften and the Fed signals a shift toward neutral or easier policy, the dollar could lose some of its broad strength. Under this backdrop, steady RBI intervention and resilient capital inflows could help the rupee stabilize or even recover some lost ground, keeping it comfortably below triple digits.

In a more adverse scenario, oil prices spike further due to geopolitical disruptions, while the Fed remains firmly hawkish and global risk sentiment weakens. Foreign investors might accelerate outflows from emerging markets, including India, just as the current account deficit widens. In that case, the pressure on the rupee could intensify, and markets would increasingly price the risk of a test of the 100 level, forcing bolder communication and action from the RBI.

Actionable Takeaways For Market Participants

Traders and investors can use a few practical guidelines to navigate this environment:

1) Track the drivers, not just the level: Watch crude oil, the DXY, RBI commentary, FX reserve trends, and foreign portfolio flows. The interplay of these indicators often matters more than the headline USD/INR rate itself.

2) Manage event risk: Key data releases such as inflation, trade balance, and GDP, as well as RBI and Fed meetings, can trigger outsized moves when currencies are at stressed levels. Adjust position sizes and leverage ahead of known catalysts.

3) Hedge strategically: Corporates and sophisticated investors should revisit hedging policies, focusing on tenor, instruments, and hedge ratios. Over-hedging can be as costly as under-hedging if conditions reverse quickly.

4) Think in scenarios: Build base, bullish, and bearish cases for the rupee and stress-test portfolios accordingly. Identify which holdings benefit from a weaker rupee and which are most exposed to currency and rate shocks.

Conclusion

The rupee’s slide beyond 96 per dollar is a clear signal that global forces—stronger dollars, higher oil, and shifting capital flows—are colliding with India’s domestic macro story. While India’s structural growth prospects remain compelling, the currency move raises near-term challenges for inflation management, corporate margins, and external financing. For traders, investors, and risk managers, this is a moment to deepen understanding of macro linkages, tighten discipline around risk, and prepare for a range of possible paths from here, including both stabilization and further stress.