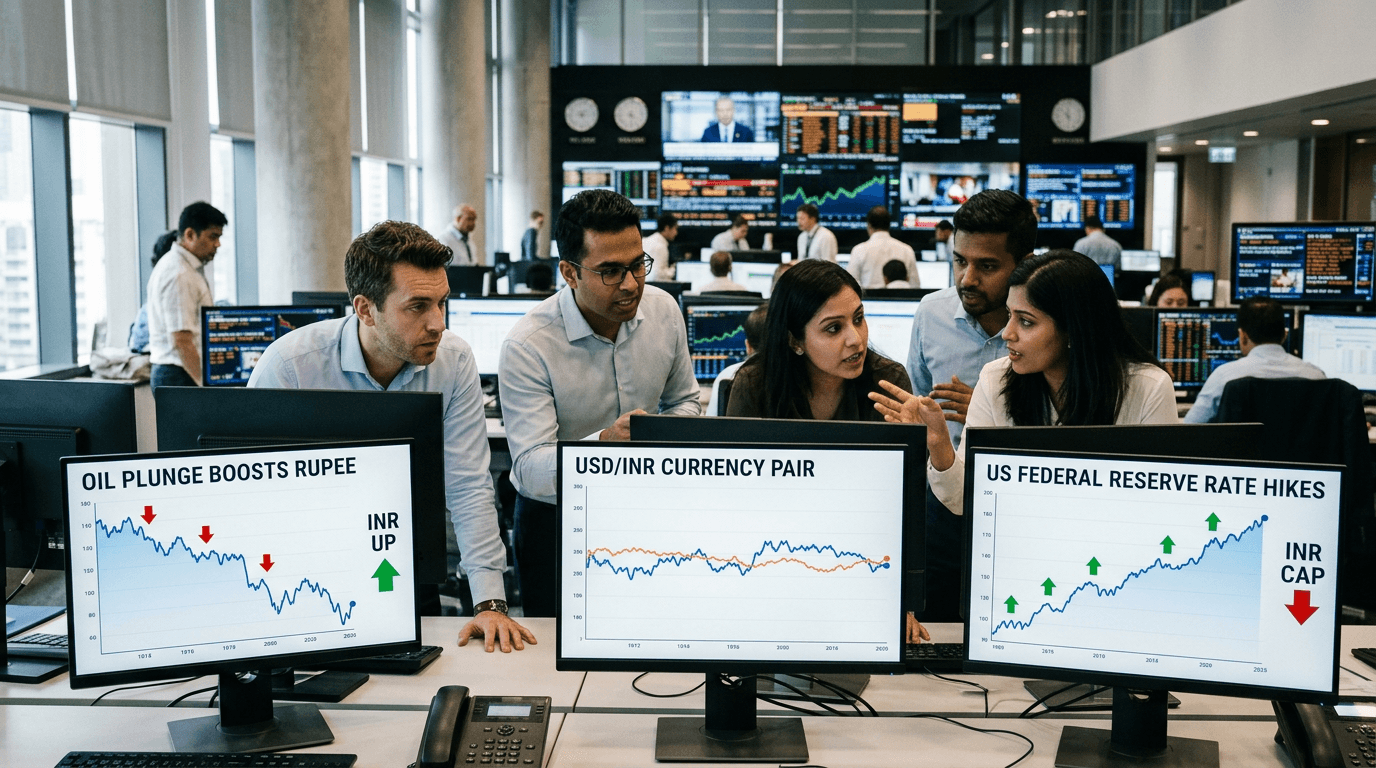

A softer crude oil market is giving the Indian rupee a welcome tailwind, but expectations of a hawkish US Federal Reserve are acting as a firm ceiling on how far that strength can run. Recent price action in USD/INR captures this tug-of-war: lower oil costs are easing India’s external pressures even as strong US yields keep the dollar bid and traders cautious about chasing rupee gains[4][10][14].

WHAT’S DRIVING THE RUPEE TODAY?

The immediate support for the rupee comes from a retreat in global crude prices, which has broadly lifted Asian currencies in recent weeks[4]. When oil slides, India’s oil import bill shrinks, easing demand for dollars from refiners and improving the trade balance, and that typically translates into a stronger rupee[3][9][15]. Recent data show the rupee stabilizing after earlier losses as falling crude prices offset some of the pressure from global risk aversion[10].

At the same time, the macro backdrop is far from straightforward. The US dollar index has stayed firm as markets price fewer Fed rate cuts and even entertain the possibility of additional tightening if inflation proves sticky[2][5][8]. Higher US yields make dollar assets more attractive, encourage capital flows into the US, and raise the hurdle for emerging market currencies like the rupee to outperform[2][14]. This is why, even on days when crude is supportive, upside in the rupee tends to be incremental rather than explosive[10][14].

For traders, this means USD/INR sits at the intersection of two powerful global narratives: energy prices and US monetary policy. Understanding which of these is in the driver’s seat on a given day is essential to framing your bias and risk levels.

Why Crude Oil Matters So Much For India

India imports around the vast majority of its crude oil needs, making it structurally sensitive to swings in global energy prices[3][9][12][15]. When Brent or WTI spike higher, the impact filters through several channels that usually weaken the rupee:

- The import bill widens, increasing demand for dollars from oil companies and raising the current account deficit[3][9][15].

- Higher fuel costs feed into inflation, potentially forcing the RBI into a more delicate balancing act between growth and price stability[9][11].

- Foreign investors may demand a higher risk premium to hold Indian assets if external balances deteriorate and inflation risks rise[9][15].

The reverse is also true when oil prices fall. A sustained decline in crude:

- Narrows the trade deficit and improves the current account outlook[3][9][15].

- Reduces imported inflation pressures, giving policymakers a bit more room to support growth[9][11].

- Typically provides a tailwind to Indian equities and bonds, which can attract foreign flows and further support the rupee[9][15].

Recent episodes have illustrated this clearly. When crude has slid sharply, the rupee has often strengthened intraday by 0.3–0.5% as dollar demand from oil importers eased and traders unwound defensive positions[4][10]. Conversely, when oil surged towards multi-month highs, the rupee tended to underperform regional peers, reflecting India’s oil-importer status[7][9][13].

In other words, softer crude is not just a “nice to have” for India; it is a core macro positive that directly improves the rupee’s fundamental backdrop.

The Fed Factor: Why Dollar Strength Caps Rupee Gains

The complication is that currencies never trade in isolation. While softer oil helps, the rupee is simultaneously contending with a Federal Reserve that remains wary of declaring victory over inflation[2][5][8]. Statements from Fed officials signalling fewer rate cuts or a willingness to keep policy tight for longer tend to push US yields higher and lift the dollar against a broad basket of currencies[2][5][8].

For the rupee, this manifests in two main ways:

- A stronger dollar environment means global investors are more selective about taking exposure to emerging markets, especially those with external financing needs[2][14][15].

- Higher US yields narrow or even invert the interest rate differential between India and the US, reducing the carry advantage of holding rupee assets[2][5][8].

Market commentary has repeatedly noted that hawkish Fed repricing can drive the rupee weaker, even in the absence of domestic shocks, with levels like 85–87 per dollar being discussed when the Fed sounds “decidedly” hawkish[2][5][14]. In such phases, any support from softer crude tends to cap losses rather than spark a sustained rally.

This is why the current narrative is “rupee stronger on softer crude, but Fed risk caps gains” rather than a straightforward bullish story. Oil is providing a floor under the rupee, but the Fed is effectively drawing a line in the sand on the upside.

Implications For Traders And Simulated Strategies

For both live traders and those using simulated finance platforms, this environment rewards nuance rather than one-way bets. Instead of treating USD/INR as a simple directional play, it can be more effective to think in terms of regimes and scenarios.

Here are some practical ways to translate this macro story into trading and SimFi practice:

- Build scenarios combining oil and Fed paths. For example, “soft oil + dovish Fed”, “soft oil + hawkish Fed”, “spiking oil + hawkish Fed”. Map out how you expect USD/INR and Indian assets to behave in each case.

- Watch correlations, not just levels. Track how closely USD/INR is moving with Brent prices and the US 10-year yield over rolling windows. High correlation with yields signals Fed dominance; high correlation with oil highlights commodity-driven moves.

- Focus on ranges and mean reversion. With supportive oil but a strong dollar cap, USD/INR may trade in well-defined ranges rather than trending relentlessly. Range-trading and options strategies that benefit from contained volatility can be attractive in simulation.

- Stress-test risk management. In SimFi, model what happens to your portfolio if oil jumps $10–15 in a short period while the Fed doubles down on hawkish messaging. That combination has historically been challenging for the rupee and Indian assets[3][7][9][13][15].

Practising these approaches in a simulated environment helps build intuition for how macro shocks feed into currency pricing, without the emotional pressure of real capital at risk.

Conclusion

The rupee’s current setup is a textbook example of how competing global forces can shape a currency’s path. Softer crude prices are improving India’s external position and giving the rupee room to strengthen, but a still-hawkish Fed and firm US yields are preventing a runaway rally[4][10][14].

For traders, the key is to recognize that both narratives matter. Ignoring oil leaves you blind to a major driver of India’s balance of payments; ignoring the Fed leaves you exposed to abrupt swings in global dollar liquidity and risk appetite[2][3][9][14][15].

By actively tracking both crude and Fed expectations, and by using simulated trading to test scenarios and risk management, you can turn this complex macro backdrop into a structured, actionable framework. In a world where currencies sit at the crossroads of commodities and central banks, the rupee’s story today is a powerful live case study in multi-factor FX trading.