Producer inflation is cooling, but consumers are feeling more anxious about the future and less confident that inflation will truly fade. That tension between softer wholesale prices and worsening sentiment has kept traders laser-focused on inflation persistence and muddied expectations for how aggressively the Federal Reserve can cut rates in 2026.[2][5]

What The Data Are Telling Us

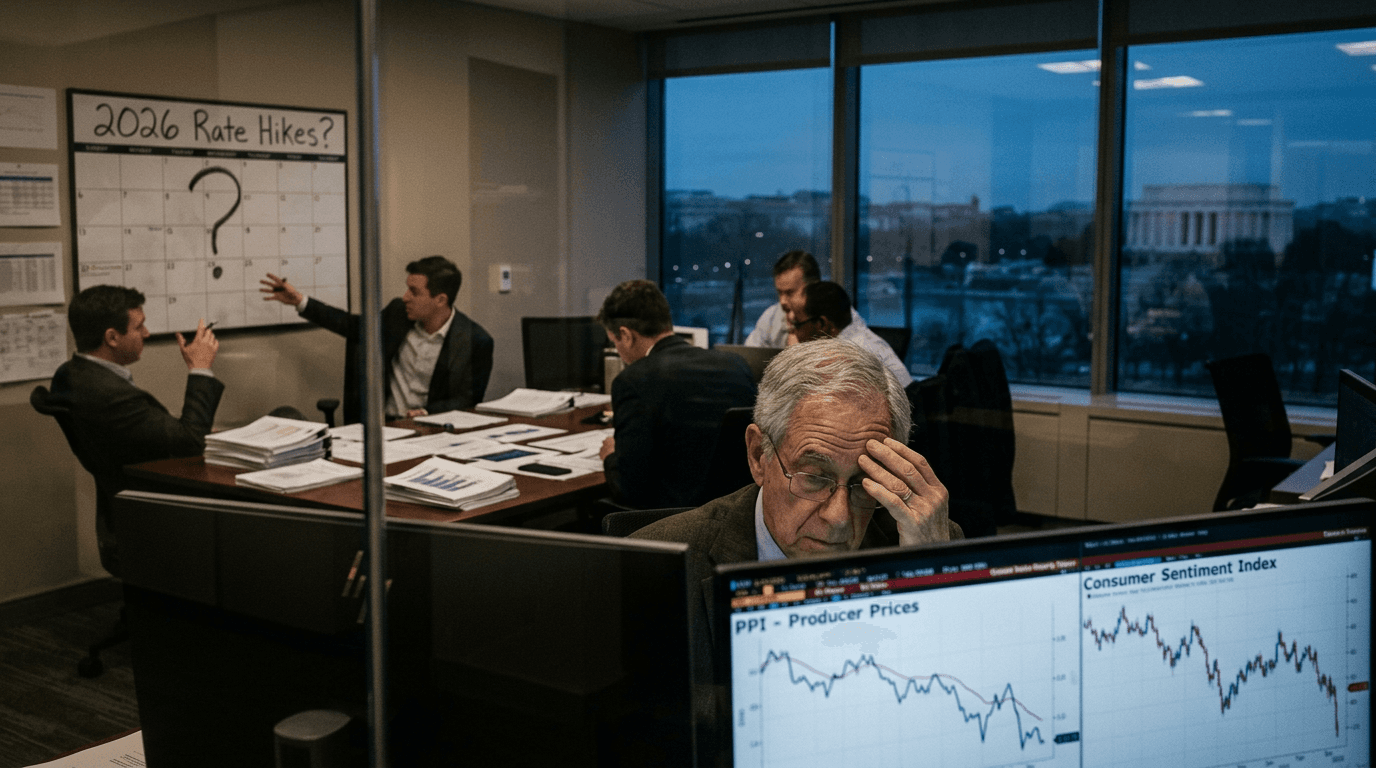

The latest U.S. Producer Price Index (PPI) report showed a weaker‑than‑expected increase in prices faced by businesses. Both headline and core producer inflation — which strips out volatile food and energy components — have been losing momentum, suggesting cost pressures in the production pipeline are easing.[2]

On its own, that is exactly what policymakers want to see. Softer producer prices often foreshadow slower consumer price increases later on, because fewer cost shocks need to be passed along to households.[1][2] For markets, weaker PPI tends to support a “less hawkish” narrative: if upstream inflation is moderating, the Fed can eventually loosen policy without as much risk of reigniting price pressures.[2]

But the consumer side is telling a different story. The University of Michigan’s consumer sentiment survey showed confidence deteriorating more than economists expected, with households reporting more pessimism about their personal finances and the broader economy.[2][3] At the same time, medium‑term inflation expectations in the survey ticked higher, a signal that consumers remain unconvinced inflation will settle back near the Fed’s 2% target.[3][4]

That combination — softer producer inflation, weaker sentiment, and stickier inflation expectations — is what has kept markets focused on inflation persistence rather than declaring victory over price pressures.

Why The Mixed Signals Matter

To understand why this data mix is so uncomfortable for traders, it helps to break down what each series captures:

- PPI primarily reflects what firms are paying for goods and services used in production.[1][2]

- Consumer sentiment captures how households feel about their financial situation, job prospects, and the overall economy.[3][5]

- Inflation expectations reveal what people think will happen to prices over the next few years.[3][4]

When producer prices cool, it signals that supply‑side pressures — from input costs to wholesale margins — are easing.[1][2] That reduces the risk of another surge in consumer inflation, especially if firms are competing harder on prices.

But when consumer sentiment falls and inflation expectations rise, it paints a different macro picture. Households may cut back discretionary spending as they feel less secure about the economy and more worried about stubbornly high prices.[3][5] Over time, that can weigh on growth, earnings, and hiring, even if the inflation backdrop is slowly improving.

This divergence matters for traders because it complicates the usual “good news vs bad news” framework. Softer PPI is good news for inflation, but worsening sentiment and sticky expectations are bad news for growth and for the Fed’s credibility in anchoring inflation psychology. The net effect is a more nuanced, and often more volatile, reaction across assets.[2]

Implications For The Fed And 2026 Rate-cut Expectations

For the Federal Reserve, the latest data stack up in three important ways:

1) Reduced near‑term pressure to hike Cooling producer inflation lowers the odds of a renewed inflation spike, giving the Fed more flexibility to keep rates on hold rather than pivoting back to tightening.[1][2]

2) Elevated concern about inflation expectations Rising medium‑term inflation expectations in the Michigan survey are a warning sign. If households continue to expect higher inflation, wage demands and pricing behavior can become harder to tame, forcing the Fed to stay restrictive for longer.[3][4]

3) Greater uncertainty around the timing and depth of cuts Weaker sentiment and growing demand risks support the case for rate cuts down the road, but persistent inflation concerns push against quick or aggressive easing.[2][5]

That push‑pull has shown up in choppy price action in Treasury futures, the dollar, and equity index futures. Rates markets have been recalibrating the expected start date and pace of any 2026 rate‑cut cycle, with each new data point nudging probabilities and term‑premium expectations around.[2] As yields and Fed funds futures wobble, knock‑on moves appear in risk assets and FX as traders constantly reassess which narrative — persistent inflation or weakening growth — is in the driver’s seat.

In effect, the data are reinforcing a “higher for longer, but not forever” story: the Fed may ultimately have room to cut in 2026, but only if inflation expectations behave and growth doesn’t weaken too sharply in the meantime.

How Traders Can Navigate Data-driven Volatility

In an environment where single data points can flip the dominant macro narrative, process matters as much as prediction. Three practical habits stand out:

• Focus on interactions, not isolated prints A benign PPI number is not automatically bullish or bearish. Its market impact depends on what is happening with growth (sentiment, labor data), policy expectations (Fed commentary, futures pricing), and risk appetite (equity and credit spreads).[2] The key question is: “What does this release do to both the inflation and the growth narrative?”

• Watch the rates market as the transmission hub Treasury yields and Fed funds futures typically react first to surprises in inflation and expectations data.[2] Moves at the front end of the curve reflect shifts in policy expectations, while the long end captures growth and term‑premium dynamics. Monitoring these changes can provide early clues before the full adjustment shows up in equities, FX, and commodities.

• Think in scenarios rather than single forecasts With conflicting signals, it is more robust to map out scenarios than to bet heavily on one path. For example: – Soft landing: PPI stays subdued, sentiment stabilizes, inflation expectations drift lower — supportive for gradual 2026 cuts and risk assets. – Delayed disinflation: PPI re‑accelerates or expectations stay high — pushing out cuts, supporting the dollar, and pressuring duration‑sensitive assets. – Growth scare: Sentiment and spending weaken faster than inflation — increasing recession odds and favoring high‑quality duration and defensive sectors.[2][5]

Position sizing, diversification, and clear invalidation levels become critical when the macro story can pivot with each release.

Testing Strategies In A Simulated Environment

Conditions like these are demanding not only for trading systems, but also for trader psychology. Data‑driven reversals, intraday whipsaws, and rapidly shifting narratives can tempt over‑trading, revenge trading, or abandoning a plan at the worst possible moment.

A simulated environment is a powerful way to stress‑test strategies against this kind of macro noise. Traders can:

- Rehearse event‑driven playbooks around data releases like PPI, CPI, and sentiment surveys.

- Practice reading the sequence of reactions — from rates to FX to index futures — without financial pressure.

- Experiment with different scenario trees: how does the strategy perform if inflation expectations stay elevated versus quickly re‑anchor?

By the time real capital is on the line, traders who have done this work in a risk‑free setting are better prepared to respond to surprises with discipline instead of emotion.

In the end, softer producer prices and souring consumer sentiment both matter — but in different ways and on different timelines. For now, they keep the spotlight firmly on inflation persistence and leave the exact path of 2026 rate cuts an open question. For traders, the edge lies not in predicting every data point, but in building a robust, scenario‑based process that can adapt as the inflation and growth stories evolve.