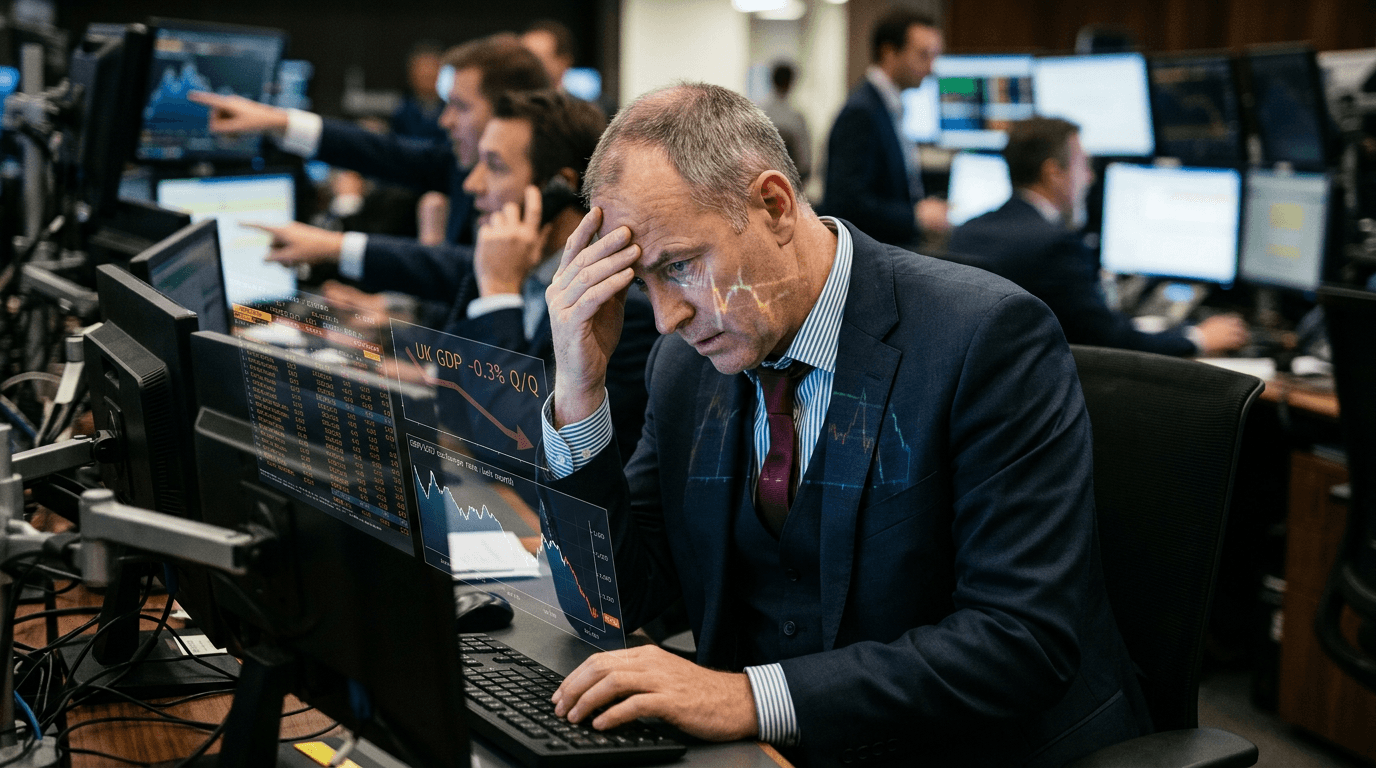

Sterling’s latest slide is a reminder that currencies are ultimately stories about growth, inflation, and interest rates – and right now, the UK’s growth story is going the wrong way. Fresh data showing that the UK economy contracted has knocked the pound lower against the dollar, reinforcing recession concerns and limiting upside for GBP even as other majors attempt to stabilise.[3] At the same time, a firm US dollar backdrop is amplifying the move, leaving FX traders firmly focused on UK data and Bank of England expectations.[3][5]

Market Reaction: Sterling Under Pressure

The immediate market takeaway from the weak UK growth print was straightforward: sell sterling, buy dollars.[3] The pound underperformed its peers, slipping against the greenback as traders priced in a softer domestic outlook and the prospect of earlier or deeper rate cuts from the Bank of England.[3][2]

The context matters. The dollar remains supported by relatively resilient US data and a perception that the Federal Reserve can keep policy restrictive for longer, maintaining a yield advantage over many of its G10 counterparts.[5] When a currency like sterling is hit by negative domestic news at the same time the dollar is underpinned by steady macro momentum, the path of least resistance for GBP/USD is usually lower.[3][5]

For short-term traders, this type of move is classic “data-driven price action”: a clear macro surprise, a clean directional reaction, and then a shift in focus toward the next set of releases that can challenge or confirm the new narrative.[3]

What The Uk Growth Data Is Signaling

A contraction in monthly GDP is more than just a headline; it is a signal that the post-pandemic and post-inflation recovery remains fragile.[3] Even a modest decline can reignite worries that the UK may be flirting with, or re-entering, a recessionary environment if weakness persists over several months.

Recent UK indicators had already suggested that momentum was uneven, with softer business and consumer sentiment pointing to caution in spending and investment.[2] When headline GDP then turns negative, it validates those concerns and encourages markets to question whether the earlier stabilisation in activity was sustainable.

The composition of growth also matters. The UK has relied heavily on services and consumption to keep output afloat. When confidence deteriorates, households tend to pull back, and services activity can slow with a lag.[2] That makes any fresh contraction particularly sensitive: it hints that the engine that had been holding up the economy may finally be losing steam.

None of this guarantees a deep recession, but it does change the probability distribution that traders and investors use. The balance of risks tilts away from “soft landing” and closer toward “stop-start stagnation with recession scares,” which is not an environment that typically supports a strong currency.

Bank Of England Expectations: The Real Driver

In FX, growth data matters largely because of what it implies for central banks. For sterling, that means the Bank of England. Weak activity and softening sentiment push markets to reassess how long the BoE can keep rates restrictive before it risks exacerbating a downturn.[2]

When growth slows and labour market concerns appear in surveys, traders tend to bring forward expectations for rate cuts, or at least remove the prospect of further tightening.[2] Lower expected interest rates reduce the yield that foreign investors can earn on sterling assets, diminishing the currency’s appeal relative to higher-yielding alternatives like the dollar.[2][5]

This is exactly the dynamic now playing out. Recent signs of cooling in the UK economy and confidence indicators have already nudged markets toward expecting earlier easing.[2] The latest contraction data adds weight to that theme, encouraging traders to test lower levels in GBP/USD as they price in a more dovish BoE path versus a still-hawkish Fed stance.[3][5]

For traders, it is crucial to understand that the reaction in sterling is less about one month of GDP and more about the accumulated pressure on the central bank’s policy stance. As each data point pushes growth lower and risk higher, the BoE’s tolerance for tight policy shrinks – and so does the pound’s interest rate support.

Implications For Fx And Simulated Traders

For discretionary FX traders and those operating in simulated trading environments, this episode offers a clear case study in how macro data, central bank expectations, and relative growth narratives interact.

First, it reinforces that FX is a relative game. Sterling’s weakness is not occurring in isolation; it is being measured against a dollar that is still backed by higher rates and solid demand, and against a euro whose own outlook is mixed but currently less under question than the UK’s.[3][5][2] That relative perspective is why cross rates like EUR/GBP and GBP/USD can tell different stories at the same time.

Second, it highlights the importance of a data calendar. Traders who know when key releases are scheduled can prepare scenarios in advance: What if GDP is negative versus consensus? What if it surprises to the upside? This planning allows for more disciplined execution when the numbers hit, instead of reactive trading under stress.

Third, it shows why risk management must adapt to macro volatility. When recession concerns rise, ranges can break, correlations can shift, and leverage that looked manageable in a quiet market can become risky. Simulated environments are valuable precisely because they let traders test strategies under these kinds of macro shocks without real capital at risk.

Practical Takeaways For Traders

There are several concrete lessons traders can draw from sterling’s reaction to the UK contraction:

1. Map the narrative: Tie each major data point back to the bigger story – in this case, “Is the UK sliding toward recession, and how will the BoE respond?” The more your trade idea aligns with that evolving narrative, the more robust it tends to be.

2. Watch rate expectations, not just spot FX: Tracking market-implied BoE and Fed paths can clarify whether a move in GBP/USD is likely to extend or fade. If growth is weakening and cuts are being priced in faster for the BoE than for the Fed, sterling rallies may struggle to sustain.

3. Think in scenarios: Build playbooks for both continuation (more weak data, more GBP downside) and reversal (a surprise rebound in activity that forces markets to reduce rate-cut bets). Testing these scenarios in a simulated setting can help refine entries, exits, and position sizing.

4. Respect the dollar factor: Even strong UK data can fail to lift GBP if the dollar is in a powerful uptrend driven by US yields or risk aversion.[5] Likewise, weak UK data hits harder when it coincides with dollar strength, as it has here.[3][5]

Looking Ahead For Gbp

Where sterling goes from here will depend on whether the latest contraction proves to be a one-off wobble or the start of a more persistent slowdown. Upcoming UK indicators on inflation, labour markets, and business activity will be critical in shaping that view and, by extension, in guiding BoE policy expectations.[2][3]

For now, the message from markets is clear: with growth under pressure and the dollar still supported, the upside for GBP looks capped unless the data turn decisively in the UK’s favour.[3][5] Traders who stay disciplined, data-focused, and attentive to the policy narrative will be best positioned to navigate whatever comes next – whether in live markets or in the safety of a simulated trading environment.