The Japanese yen is once again front and center in global markets, trading near its weakest level against the US dollar in almost 40 years and putting traders on high alert for potential government intervention.[1][3] For anyone following macro trends—or practicing FX strategies on a simulated platform—this is a live case study in how monetary policy, capital flows, and market psychology can collide.

WHAT’S DRIVING THE YEN’S DROP?

At the core of the yen’s weakness is a stark interest rate gap between Japan and the United States.[1][3] While the Federal Reserve has kept rates elevated and remains relatively hawkish, markets still expect Japanese rates to stay very low by global standards, even after the Bank of Japan’s gradual shift away from negative rates.[2][3] Higher yields in the US make dollar assets more attractive, encouraging investors to sell yen and buy dollars.

This rate differential powers the classic “carry trade”: borrowing in a low-yielding currency like yen to invest in higher-yielding assets elsewhere.[4][5] As more investors lean into this strategy, it amplifies selling pressure on the yen and reinforces the trend.

Structural flows also matter. Japan remains a major buyer of US Treasuries, and elevated Treasury yields encourage Japanese institutions to hold more dollar assets for longer.[5] Many Japanese multinationals have also been slow to repatriate overseas profits, while domestic investment programs such as tax-advantaged accounts encourage households to invest abroad, often in US markets.[5] Those choices translate into more demand for dollars and less for yen.

On top of that, Japan is heavily dependent on imported energy. Higher oil prices—linked in part to geopolitical tensions—worsen the trade balance and make a weak yen more painful, as every barrel of oil priced in dollars costs more in local currency terms.[3] Together, these factors create a powerful backdrop for sustained yen depreciation.

Why 40-year Lows Matter For Policymakers

The yen’s slide is not purely a problem; it has upside for parts of the Japanese economy. A weaker currency boosts the competitiveness and profits of export-oriented firms, including many of the large manufacturers that dominate Japan’s equity indices.[4][7] That support has been one reason Japanese stocks have attracted renewed global interest.

But there is a flip side. Import costs rise as the yen falls, pushing up prices for energy, food, and raw materials and squeezing households and smaller businesses.[3][7] After decades of battling deflation, Japan has finally seen sustained inflation—partly thanks to a weaker yen—which helps erode the real value of its very large public debt and supports government finances.[7] However, the same inflation is eroding purchasing power and generating political pressure.

Policymakers therefore face a delicate balance. They do not want to choke off inflation prematurely or undermine export strength by forcing the yen much stronger.[7] At the same time, they must resist “excessive” or disorderly moves that risk destabilizing financial markets and hurting consumers. That is why specific levels—like a 40‑year low—become psychological and political thresholds where intervention becomes more likely.[2][3]

INTERVENTION RISK: WHERE IS THE LINE?

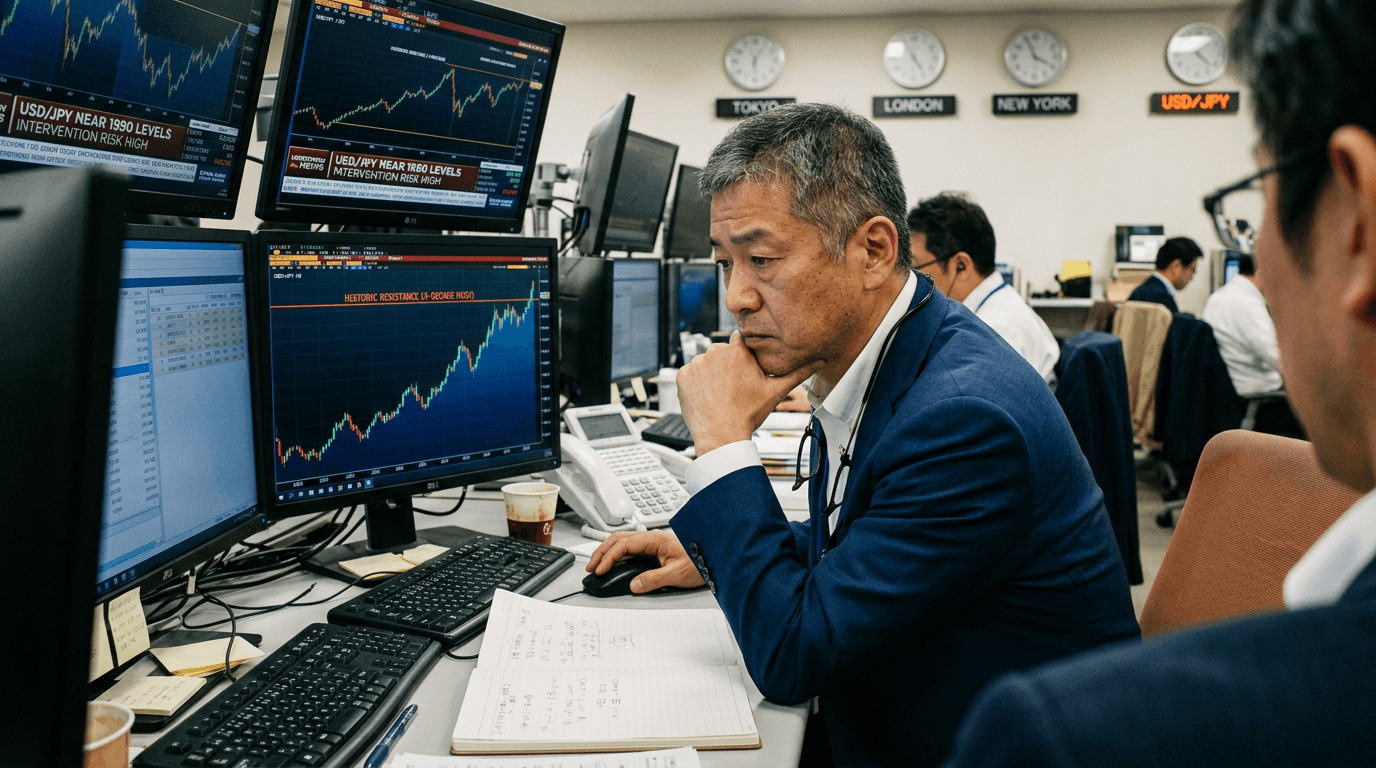

USD/JPY recently traded around 161–162, putting the yen in territory last seen in the mid‑1980s and effectively erasing the impact of earlier intervention efforts.[1][3][6] Market participants widely view a sustained break above the prior high near 161.96 as the point at which the yen would mark its weakest level since 1986, making it a symbolic battleground for policymakers.[2][3]

Japan has already demonstrated it is willing to act. In previous episodes, authorities deployed large-scale FX intervention—selling dollars and buying yen—to counter sharp depreciation, with one campaign totaling around 11.7 trillion yen.[3] Officials, including Finance Minister Satsuki Katayama, have repeatedly signaled readiness to respond decisively to speculative moves and have highlighted G7 language that allows action against excessive volatility.[1][3]

For traders, this sets up a classic “intervention watch.” Liquidity pockets—such as holiday-thinned sessions—can be attractive windows for authorities to act, as their orders have more impact.[3] When intervention comes, it is often abrupt, generating sharp, rapid drops in USD/JPY and spikes in short-term volatility. Anyone trading the pair—or simulating trades—needs to factor this event risk into position sizing, leverage, and stop placement.

Ripple Effects Across Asia Fx, Equities And Carry Trades

The yen’s weakness is not happening in isolation. The US dollar is trading near a more than one‑year high against a basket of currencies, reinforcing pressure on many Asia-Pacific FX pairs.[1][3] As USD/JPY pushes toward extreme levels, volatility in the pair can spill over into other regional currencies, particularly those associated with carry trades or export-driven economies.

Japanese equity futures, including Nikkei-linked contracts, are also sensitive to yen moves.[1][4] A weaker yen can be supportive for large exporters, but if the currency slide looks disorderly or intervention looms, equity volatility can pick up as global investors reassess both FX and rate risk.

The carry trade dimension is crucial. When yen-funded carry positions become crowded, the system is more vulnerable to a sharp unwinding if intervention or a risk-off shock forces traders to quickly reduce leverage.[4][5] That can trigger rapid, correlated moves across FX, rates, and equity markets—exactly the kind of cross-asset dynamics active traders and SimFi participants aim to understand.

Practical Takeaways For Simulated Traders

For traders using simulated environments to build skills, the current yen backdrop offers several valuable lessons:

First, respect key levels. Historical extremes—like a 40‑year low—often act as catalysts for policy action or sharp reversals. Tracking zones such as 161–162 in USD/JPY helps frame scenarios and potential turning points.[2][3]

Second, integrate macro into your strategy. Rate differentials, central bank messaging, and energy prices are not background noise; they are core drivers of FX trends. Incorporating macro data and central bank speeches into your trade planning can improve both timing and conviction.[1][2][3]

Third, plan for event risk. Intervention risk is binary: either it happens or it doesn’t, and when it does, the move is usually fast. Simulated trading is an ideal place to practice managing gap risk, sudden volatility, and slippage, using tools like wider stop buffers, reduced position sizes, and scenario testing around known risk windows.

Fourth, look beyond one market. The yen story is simultaneously an FX, rates, equity, and carry trade story. Experimenting with cross-asset strategies—such as pairing USD/JPY views with Nikkei futures or regional FX—helps build a more holistic understanding of how global markets interact.[1][4][5]

As the yen hovers near levels last seen in the 1980s, Japan’s policymakers face a narrow path between supporting inflation and preserving market stability.[3][7] For traders and investors, this is more than a headline; it is an opportunity to study, simulate, and eventually trade a complex macro regime where policy, psychology, and price action meet. Whether intervention arrives or not, the lessons from this period will resonate well beyond the next big move in USD/JPY.