Market Overview: US CPI Data Takes Center Stage

Hello traders! With a new trading week on the horizon, E8 Funding has prepared a Market Overview for you, designed to keep you informed about the latest and most important events from the economic calendar.

What’s Driving the Markets This Week

Undoubtedly, the most anticipated data release this week is the US Consumer Price Index (CPI) report. The Federal Reserve has recently maintained a hawkish stance on monetary policy due to persistent inflation, signaling an intention to keep interest rates higher for an extended period. However, recent data, particularly the latest Initial Jobless Claims report, suggests that the labor market may not be as tight as the Fed expects. This makes the weekly Initial Jobless Claims report another crucial data point to watch this week.

Beyond the US, the UK and Australia will also release their latest labor market data, while Japan will reveal its GDP activity. Additionally, China will announce its change in industrial production following last month’s disappointing figures. These global economic indicators will collectively shape market sentiment and expectations for the coming week.

Monday, May 13th, 2024

The week began in Australia with the release of the NAB Business Confidence data for April 2024, which remained at 1, unchanged for the second consecutive month, and below its long-run average. Despite this, the Australian dollar has continued to strengthen due to the hawkish stance of the Reserve Bank of Australia (RBA) following the recent CPI data, which has fueled market speculation about the possibility of another interest rate hike.

No other major economic data releases are scheduled for Monday.

Speeches:

- 02:00 pm – ECB Claudia Buch

- 02:00 pm – FED Philip Jefferson

- 02:00 pm – FED Loretta Mester

- 05:45 pm – SNB Chairman Thomas Jordan

Tuesday, May 14th, 2024

Tuesday starts with labor market data from the UK. The Bank of England (BoE) has already confirmed that rate cuts are imminent and expressed a dovish outlook. The Unemployment Rate release, expected to rise to 4.3% from 4.2% last month, could further support this policy direction.

News from the Eurozone follows shortly after, with the Centre for European Economic Research (ZEW) releasing its Economic Sentiment Index. The index is currently at its highest level since early 2022 and is anticipated to continue rising. Half of the analysts surveyed predict an improvement in the German economy over the next six months, driven by factors such as a favorable economic assessment, positive expectations for top export destinations, and the strengthening of the dollar and euro.

A preliminary glimpse into Wednesday’s US inflation data will come in the form of the Producer Price Index (PPI) figures released at 1:30 pm.

Speeches:

- 08:30 am – BoE Huw Pill

- 01:45 pm – ECB Isabel Schnabel

- 02:10 pm – FED Lisa D. Cook

- 03:00 pm – FED Chair Jerome Powell

Wednesday, May 14th, 2024

Wednesday begins with data from the Eurozone: Quarterly Preliminary Employment Change and Estimated GDP Growth Rate. The Eurozone economy expanded by 0.3% in the first quarter of 2024, exceeding market expectations of 0.1% and marking the fastest growth rate since the third quarter of 2022. Despite this positive news, the euro’s value has been influenced by the European Central Bank’s (ECB) dovish monetary policy, which is expected to lead to the first interest rate cut among major central banks. While this policy may further stimulate economic activity and GDP growth, it could also weaken the euro due to the ECB’s dovishness.

The day culminates with the week’s most anticipated economic data release: the US Consumer Price Index (CPI). While the Federal Reserve (FED) tends to prioritize Personal Consumption Expenditures (PCE) data for monetary policy adjustments, the CPI report holds significant weight as an indicator of inflation trends in the United States. The Fed’s recent hawkish stance, prompted by persistent inflation, has bolstered the US dollar. In March 2024, the Consumer Price Index increased by 0.4% month-over-month (Core CPI also 0.4%), exceeding market forecasts of 0.3%. However, recent developments, including last week’s Initial Jobless Claims report, have signaled a weakening US dollar amid signs of easing inflation and a less tight labor market. Market sentiment now leans towards anticipating a slowdown in prices and a more dovish Fed response, potentially including commentaries on a rate cut. While the market has priced in the Fed’s hawkishness, there is greater downside risk for the US dollar than the upside, meaning market momentum will be amplified if inflation surprises consensus by falling short of expectations.

- Higher Inflation: An increase in prices would further support the Fed’s hawkish stance, leading to bullish momentum for the dollar as expectations solidify for a delayed rate cut.

- Lower Inflation: Conversely, a decrease in inflation would trigger strong bearish momentum for the dollar, as markets would speculate about an earlier-than-expected rate cut from the FED.

More crucial than the overall inflation figure will be the details regarding which sectors experience price increases or decreases, along with the underlying factors driving these changes. Throughout the week, several FED members are scheduled to deliver speeches, offering further insights into how the new inflation data will influence the Fed’s policy decisions.

Alongside the inflation data, the U.S. Census Bureau will also release the latest change in the country’s Retail Sales. In March 2024, retail sales rose by 0.7% month-over-month, exceeding forecasts of 0.3%. This data contributed to higher inflation previously, and the new figures will be of significant importance, as stronger sales imply sustained inflationary pressure, while weaker sales often lead to lower demand and eventually slower price growth.

Speeches:

- 05:00 pm – FED Neel Kashkari

- 08:20 pm – FED Michelle Bowman

Thursday, May 16th, 2024

Thursday commences early with the release of Japan’s Preliminary GDP Growth Rate. As Japan grapples with defending its weak currency, economic activity is also expected to suffer. Current market expectations point to a contraction of 0.4% in Japan’s economy for the first quarter of this year, following 0.1% growth in Q4 2023. After the Bank of Japan’s (BoJ) unsuccessful intervention to support the yen and another economic slowdown, prospects for Japan appear dim, at least for the time being.

Following Japan’s GDP data, the highly anticipated labor market data from Australia takes center stage. The Australian dollar has outperformed other currencies, primarily due to the hawkish stance of the Reserve Bank of Australia (RBA), which has indicated that another rate hike remains possible following the March CPI figures, suggesting that taming inflation in Australia may prove challenging. To justify maintaining high rates or even implementing another hike, the RBA needs to see a tight labor market alongside persistent inflation. If inflation slows down and the unemployment rate rises, the RBA’s stance could shift towards dovishness, potentially ruling out further rate hikes. Currently, the unemployment rate is projected to increase slightly to 3.9% in April from 3.8% in the previous month, indicating the effectiveness of interest rate adjustments.

The afternoon brings more data from the US, including real estate figures and, more importantly, the Initial Jobless Claims report. As mentioned earlier, the US dollar has been depreciating since the last Jobless Claims release, which saw a jump of 22,000 to 231,000 for the week ending May 4th, the highest level since August 2023 and well above market expectations of 210,000. This development contradicts the tight labor market that the Fed needs to justify keeping interest rates high. If Jobless Claims remain elevated, the US dollar could face further pressure, signaling increased dovishness from the Fed.

Following the Initial Jobless Claims report, data on Industrial and Manufacturing Production in the US will be released, along with more speeches from Fed board members throughout the day.

Speeches:

- 12:40 am – RBA Sarah Hunter

- 12:00 pm – BoE Megan Greene

- 03:00 pm – FED Michael Barr

- 03:30 pm – FED Patrick Harker

- 04:30 pm – FED Loretta Mester

- 08:50 pm – FED Raphael Bostic

Friday, May 17th, 2024

Friday delivers crucial data from China: Industrial Production, a key indicator that influences global trade and supply chains, commodity demand, and economic growth forecasts. In March 2024, China’s industrial production grew by 4.5% year-on-year, a significant slowdown compared to the 7% growth in January-February combined and below market expectations of 5.4%. This marked the weakest expansion in industrial output since the previous September, attributed to slower growth across all sectors. However, current projections anticipate a recovery to 5.4% growth, which would partially offset the earlier decline.

Alongside Industrial Production, China will also release Retail Sales and Unemployment Rate data, followed by an NBS Press Conference.

No other major economic data releases are scheduled for Friday, making it a relatively quiet day for economic news, concluding the week’s market events.

Speeches:

- 08:20 am – ECB Luis de Guindos

- 09:00 am – BoE Catherine L Mann

- 03:15 pm – FED Christopher J. Waller

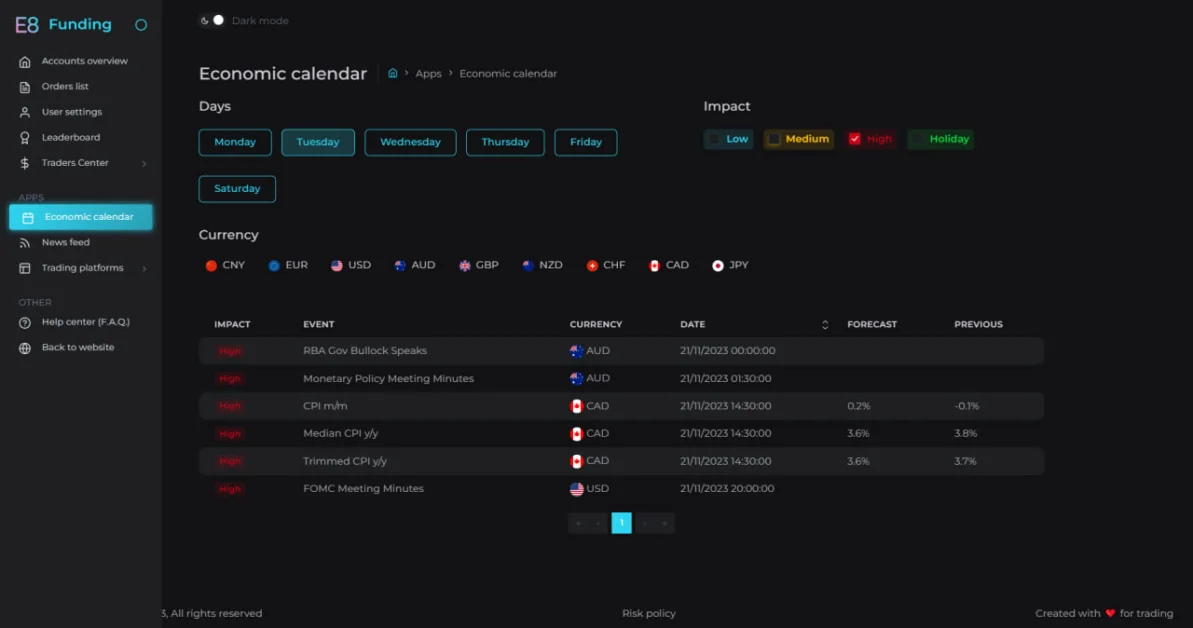

E8X Dashboard

If you’re new to our Economic Calendar, explore our detailed guide to learn more!

The Trader’s Toolbox: Mastering the Economic Calendar

Stay ahead of key economic events and data releases with our E8X Dashboard. It’s all there under the Economic Calendar tab, offering a user-friendly interface for your convenience.

Article topics

Trade with E8 Markets

Start our evaluation and get opportunity to start earning.

Disclaimer

The information provided on this website is for informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. We do not endorse or promote any specific investments, and any decisions you make are at your own risk. This website and its content are not responsible for any financial losses or gains you may experience.

Please consult with a legal professional to ensure this disclaimer complies with any applicable laws and regulations in your jurisdiction.