Market Overview: Focus on US, China CPI

Good morning, traders. As we embark on our journey through this week’s Fundamental Analysis, let me first extend my warmest New Year greetings to you all. May 2024 be a year of prosperity and success, both in your personal and in your trading endeavors!

Turning our focus to the upcoming week, we observe a relatively stable market outlook. The primary events likely to influence market volatility are the upcoming Consumer Price Index (CPI) releases from Australia, the United States, and China.

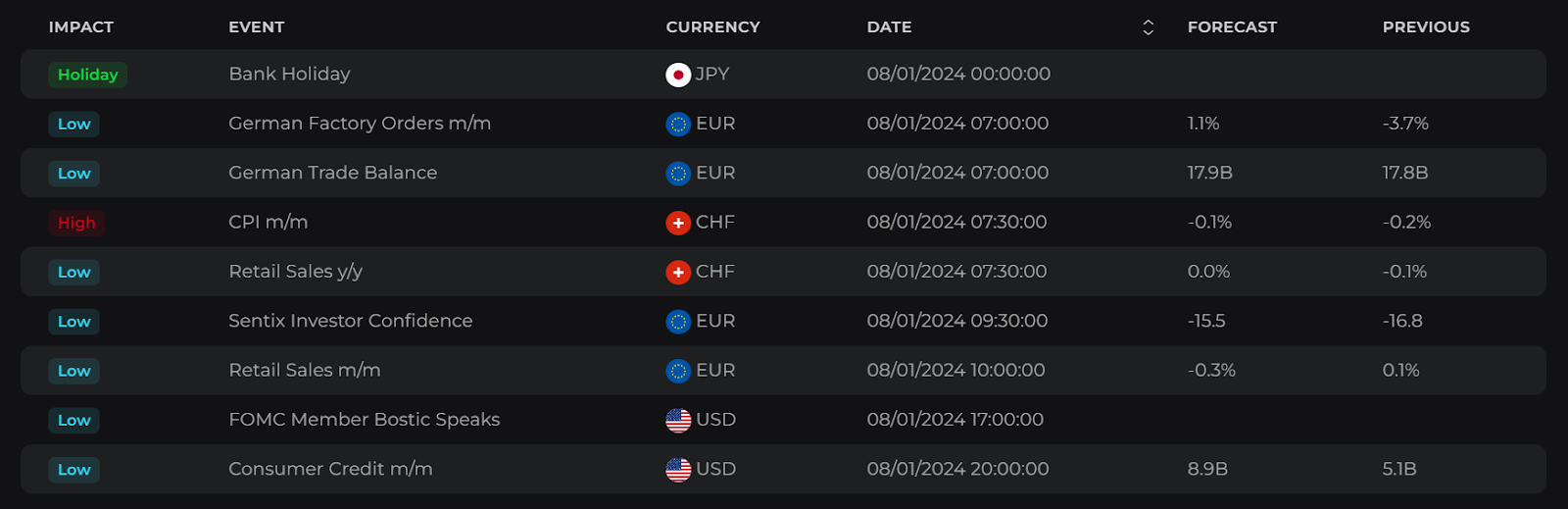

Monday, January 8th, 2024

On Monday, traders’ attention will primarily be on Europe, beginning with Germany. The International Trade data and Factory Orders for Germany have already been released, showing a trade surplus that exceeded market expectations. Additionally, there was a 0.3% increase in factory orders, a significant improvement from the previous month’s 3.8% decline. However, this growth was still below the market forecast of a 1.0% increase.

The Swiss Federal Statistical Office has released the CPI figures for December 2023. The annual inflation rate in Switzerland increased to 1.7%, up from 1.4% in the previous month, surpassing the market expectation of 1.5%. These new numbers are unlikely to have a major impact on the monetary policy of the Swiss National Bank, as the inflation rate remains at a level considered economically healthy, and no further policy tightening is anticipated. Additionally, there’s encouraging news from Switzerland’s retail sector: Retail Sales in November 2023 increased by 0.7% year-on-year, recovering from an upwardly revised 0.3% decrease in October. This marks an end to a four-month trend of declining sales.

The remainder of Monday features the release of Economic Sentiment data from the Eurozone. This indicator is a composite measure assessing confidence levels among various sectors, including manufacturers, service providers, consumers, retailers, and construction firms. Following the release from the European Commission, EuroStat will present the latest Retail Sales figures, both at 10:00am.

In the afternoon, there are no major events scheduled. However, later in the evening, Japan will announce its Household Spending figures. Additionally, Tokyo, a key economic center in Japan, will report the change in its Consumer Price Index (CPI) for December 2023. This will offer a glimpse into what the upcoming inflation figures for Japan might look like.

On Monday, there are no major speeches scheduled, except one by Raphael Bostic, the President and Chief Executive Officer of the Federal Reserve Bank of Atlanta, at 5 pm. This event is not expected to cause high volatility.

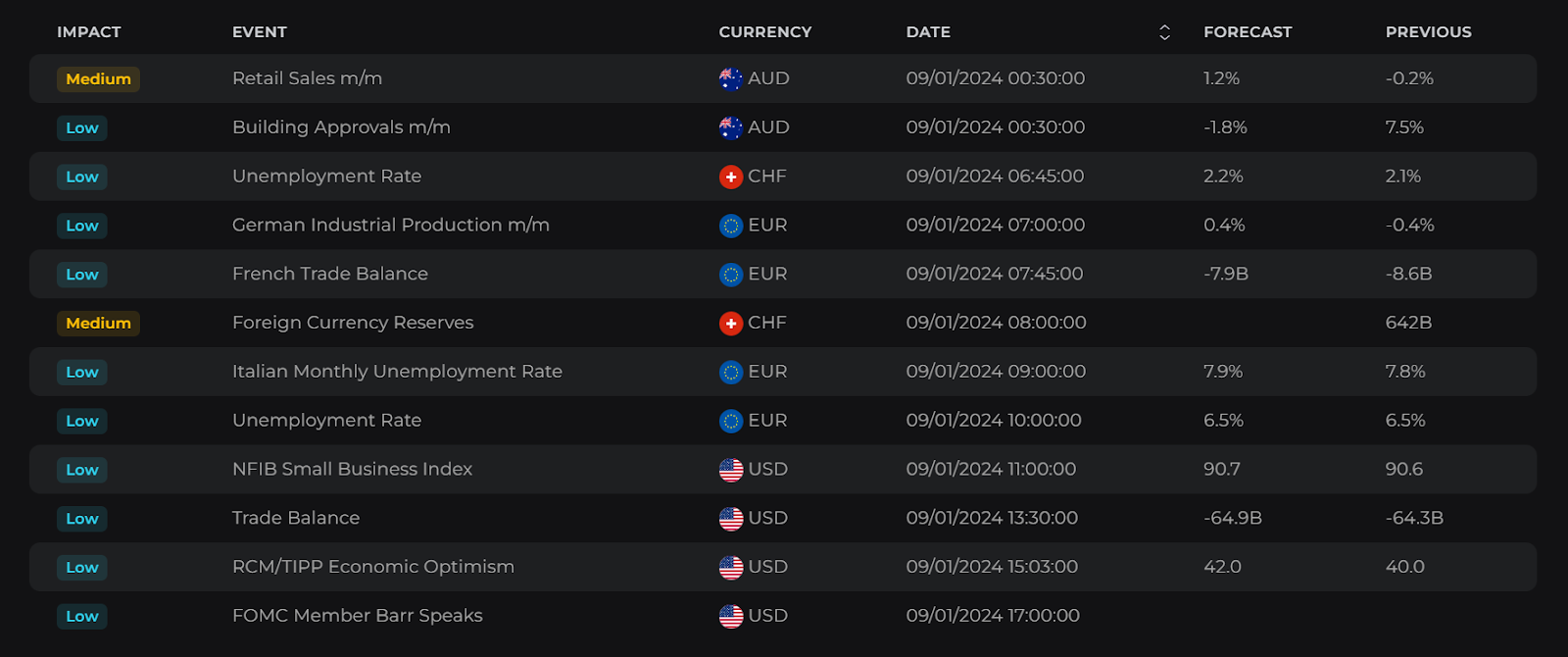

Tuesday, January 9th, 2024

Tuesday kicks off in Australia, with Retail Sales figures set to be released 30 minutes past midnight. Current market expectations suggest that Retail Sales might see a significant increase of 1.2%, potentially the largest growth of the year. This is typically attributed to increased spending during the holiday season and in preparation for Christmas.

At 6:45am, the Swiss State Secretariat for Economic Affairs is scheduled to release the Unemployment Rate, which remained stable at around 2% throughout 2023. Then, 15 minutes later, the focus shifts to Germany with the release of the monthly change in Industrial Production.

At 10:00am, the EuroStat is set to announce the Unemployment Rate for the Eurozone. However, no significant change is anticipated, as the rate has consistently been at 6.5% for an extended period, and market expectations align with this stability.

In the afternoon, at 1:30pm, there will be a detailed release of the International Trade data for both Canada and the US, offering insights into their trading activities.

There are no speeches scheduled in the economic calendar for Tuesday.

Wednesday, January 10th, 2024

Wednesday appears to be a relatively quiet day, with no major releases scheduled except for the Consumer Price Index (CPI) in Australia. The annual CPI for October 2023 in Australia showed an increase of 4.9%, a decrease from September’s five-month high of 5.6% and below the forecasted 5.2%. Current market expectations suggest a further decline in inflation, with consensus estimates at around 4.4%. Although this figure remains above the Reserve Bank of Australia’s (RBA) target range of 2-3%, it represents an improvement and indicates to the Bank that additional tightening may not be necessary, supporting a “wait and see” approach.

Commodity traders will be keeping an eye on the EIA Weekly Petroleum Status Report, scheduled for release at 3:30pm.

Luis de Guindos, the Vice-President of the ECB, is slated to give a speech at the Spain Investor Day in Madrid at 8:20 am. Later in the day, John Williams, President of the New York Federal Reserve, is scheduled to speak at 8:15 pm. Neither of these speeches is expected to lead to a significant increase in market momentum

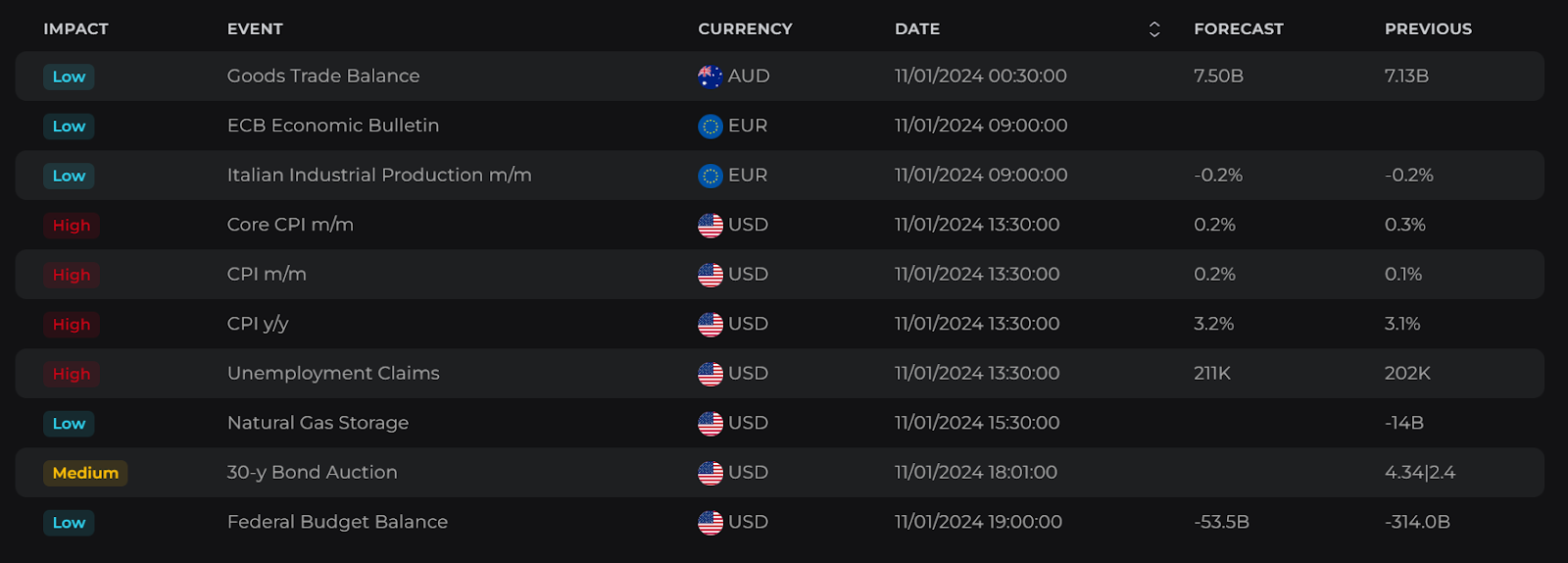

Thursday, January 11th, 2024

Thursday begins in Australia with the release of the country’s International Trade data at 12:30 am.

At 9 am, the European Central Bank (ECB) is scheduled to publish its Economic Bulletin. This bulletin provides comprehensive economic and monetary information that underpins the policy decisions of the Governing Council. Issued eight times a year, it is released two weeks following each monetary policy meeting of the ECB.

Arguably the most critical release of the week is the change in the US Consumer Price Index (CPI). In November 2023, the annual inflation rate in the US decelerated to 3.1%, marking the lowest level in five months, down from 3.2% in October and aligning with market forecasts. For December 2023, expectations are for the CPI to edge back up to 3.2%. Meanwhile, the Core Inflation Rate, which excludes volatile items like food and energy, is anticipated to decrease to 3.8%. While such figures are largely anticipated, any significant deviations could impact the Federal Reserve’s future actions and potentially introduce volatility into the market at the time of release. Therefore, it’s advisable for traders, whether holding positions in the dollar or not, to closely monitor this release for new opportunities.

There are no significant speeches scheduled for Thursday on the calendar.

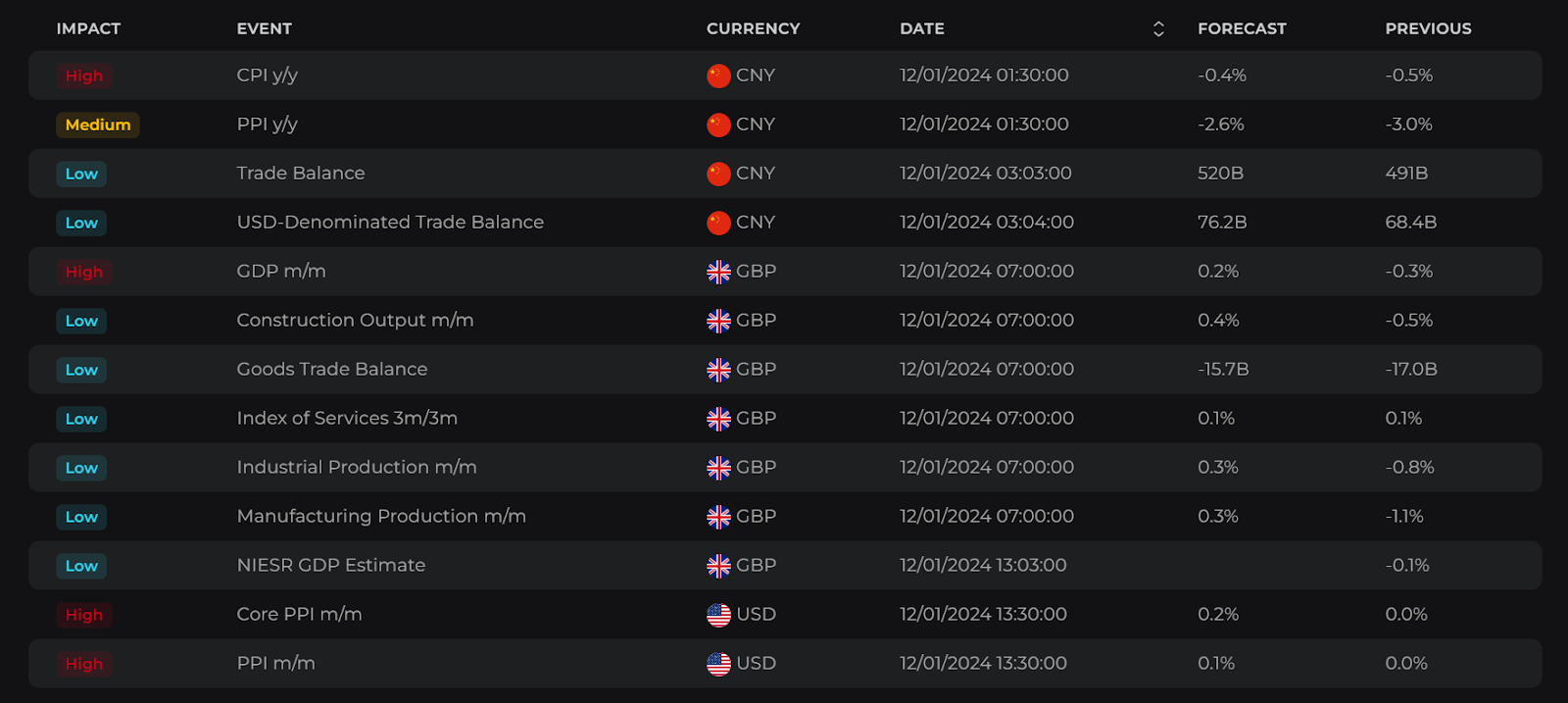

Friday, January 12th, 2024

As the week concludes, China will release its latest Inflation Rate data at 1:30 am. The country is currently grappling with a deflationary trend, exacerbated by a combination of domestic food price increases, adjustments in international oil prices, and subdued domestic demand. There’s no clear consensus for the upcoming inflation figures.

Additionally, at 3:00 am, China will offer a detailed insight into its International Trade.

The first significant update from the UK for the week arrives on Friday morning at 7:00 am. The UK’s Office for National Statistics is set to publish data on GDP, Goods Trade Balance, and Industrial and Manufacturing Production for November 2023. These releases are keenly awaited, especially since the previous figures were quite negative.

The week concludes with the release of the Producer Price Index (PPI) data from the US at 1:30 pm, providing a more detailed perspective on the price situation in the world’s largest economy.

The event calendar for Friday includes a speech by Mr. Lane, accompanied by a Q&A session, at the REBUILD Annual Conference focusing on Post-Pandemic Economic Governance and Next Generation EU in Dublin. Later in the day, at 3:00 pm, Neel Kashkari, President of the Minneapolis Federal Reserve Bank, is scheduled to speak. However, neither of these speeches is anticipated to have a significant impact on the market.

E8X Dashboard

Stay ahead of key economic events and data releases with our E8X Dashboard. It’s all there under the Economic Calendar tab, offering a user-friendly interface for your convenience.

Article topics

Trade with E8 Markets

Start our evaluation and get opportunity to start earning.Suggested Articles:

Disclaimer

The information provided on this website is for informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. We do not endorse or promote any specific investments, and any decisions you make are at your own risk. This website and its content are not responsible for any financial losses or gains you may experience.

Please consult with a legal professional to ensure this disclaimer complies with any applicable laws and regulations in your jurisdiction.