Market Overview: A Calm Week Ahead

Hello, traders! A new trading week begins, and E8 brings you a comprehensive Market Overview, detailing key economic happenings and insights to navigate the FX Market. Stay informed about market trends with our fundamental analysis.

Last week experienced significant volatility with central banks deliberating on their monetary policies and future prospects. This week presents a contrast, as the economic calendar appears less eventful. However, monitoring this week’s data will be crucial as it is set to play a key role in shaping the developments of the upcoming week.

Key Events of the Week Include:

- Consumer Sentiment in Australia and Germany

- Preliminary Inflation Figures from Spain, France and Italy

- GDP Growth Rate in Canada

- US Core PCE Price Index

- Personal Income and Spending in the United States

Monday, March 25th, 2024

The week will kick off slowly with minimal activities scheduled on the economic calendar. However, as the day concludes, roughly 30 minutes prior to midnight, Australia will unveil the most recent change in Consumer Confidence.

Speeches:

- 10:00 am – ECB Christine Lagarde

- 12:25 pm – FED Raphael Bostic

- 02:15 pm – BoE Catherine L Mann

- 02:30 pm – FED Lisa Cook

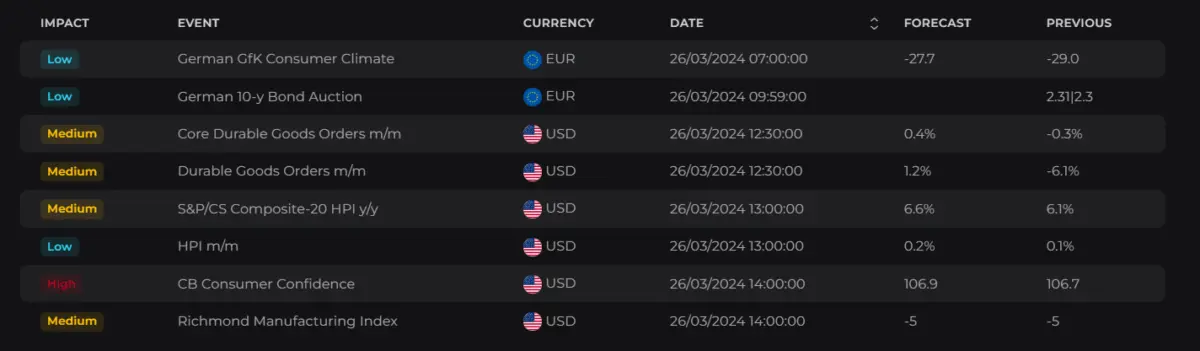

Tuesday, March 26th, 2024

The day begins at 7:00 am with Consumer Confidence data, this time from Germany, Europe’s largest economy.

At 12:30 pm, Canada will disclose its monthly changes in Manufacturing and Wholesale Sales. Simultaneously, and more significantly, the US will publish Durable Goods Orders data. Additionally, the US will announce Consumer Confidence figures at 2:00 pm. There are no other significant data releases scheduled for Tuesday.

Speeches:

- 02:20 am – RBA Ellis Connolly

- 12:15 pm – BoC Carolyn Rogers

- 07:00 pm – ECB Philip Lane

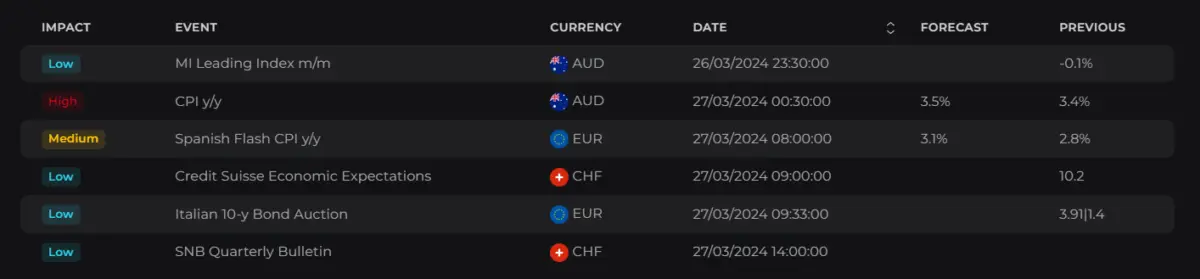

Wednesday, March 27th, 2024

At midnight, ANZ Bank will release the Business Confidence Index for New Zealand, aimed at reflecting business sentiment about the future state of their operations and the overall economy.

Half an hour later, the Australian Bureau of Statistics is scheduled to unveil the Monthly CPI Indicator, which remained at 3.4% year-on-year in January 2024, consistent with the previous month and below market expectations of 3.6%. This latest figure represents the lowest since November 2021, driven by a slowdown in transport costs, notably automotive fuel, and housing prices. Currently, the consensus stands at 3.5%, with many analysts predicting a higher figure that could impact the RBA’s rate decisions, especially if inflation continues to rise. The RBA anticipates inflation moving towards the 2–3% range in 2025, with a midpoint in 2026, as discussed in its last monetary policy meeting.

The fourth-largest economy in the Eurozone will disclose its Preliminary Inflation data at 8:00 am. Although individual country figures might not significantly impact the market, additional data from Europe’s largest economies throughout this week will provide insights into the potential overall Eurozone inflation to be announced next week.

At 10:00 am, Switzerland and the Eurozone are set to release Economic Sentiment data, with the Eurozone also publishing figures on Industrial Sentiment and Consumer Confidence.

Later in the evening, the Bank of Japan (BoJ) will issue the Summary of Opinions report from its latest Monetary Policy Meeting held on March 19th. This report will include the BOJ’s forecasts for inflation and economic growth.

Speeches:

- 01:00 am – BoJ Naoki Tamura

- 09:00 am – ECB Piero Cipollone

- 10:00 pm – FED Christopher Waller

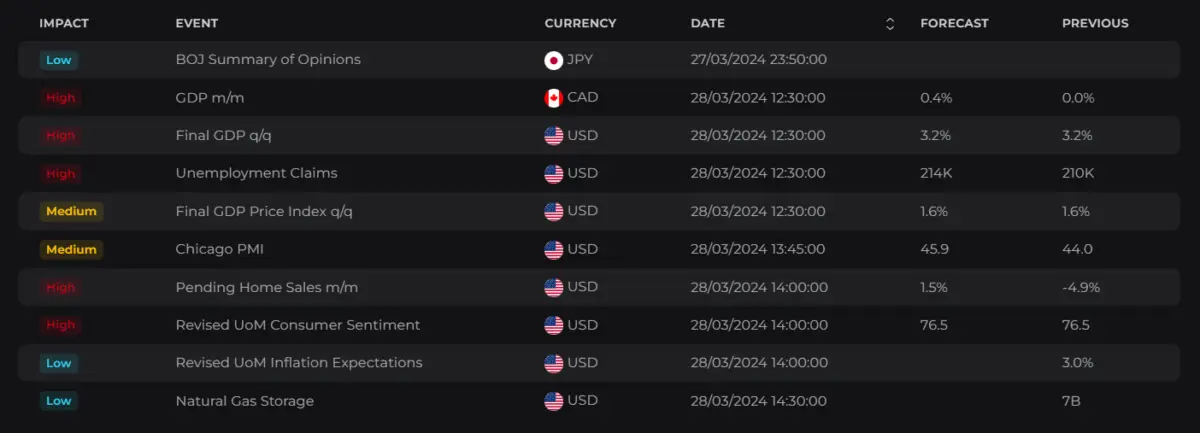

Thursday, March 28th, 2024

The day kicks off in Australia with Housing Credit and Retail Sales data released at 12:30 am.

Germany will then follow with its Retail Sales report, which measures a gauge of retail goods and services sold over a particular period, at 7:00 am. Two hours later, Germany will release additional data from the country’s labor market.

At 8:00 am, the Swiss Economic Institute (KOF) is scheduled to release its Leading Indicators, reflecting the optimism of company leaders regarding economic performance and their own organizations’ futures. This index includes 219 indicator variables weighted statistically, with the GDP module (excluding the construction and banking sectors) being the most significant, representing over 90% of Swiss GDP.

New data releases will continue at 12:30 pm, starting with Canada, which will announce its GDP data for January 2024 and Preliminary GDP data for February. Following Canada, the US will release changes in Corporate Profits and, as usual, Initial Jobless Claims. The number of US unemployment benefit claimants dropped by 2,000 to 210,000 for the week ending March 16th, 2024, below the anticipated 215,000. This demonstrated the continued strength of the US labor market, supporting the Federal Reserve’s assessment and potentially delaying rate cut starts. Current market expectations remain at 215,000, identical to last week’s consensus.

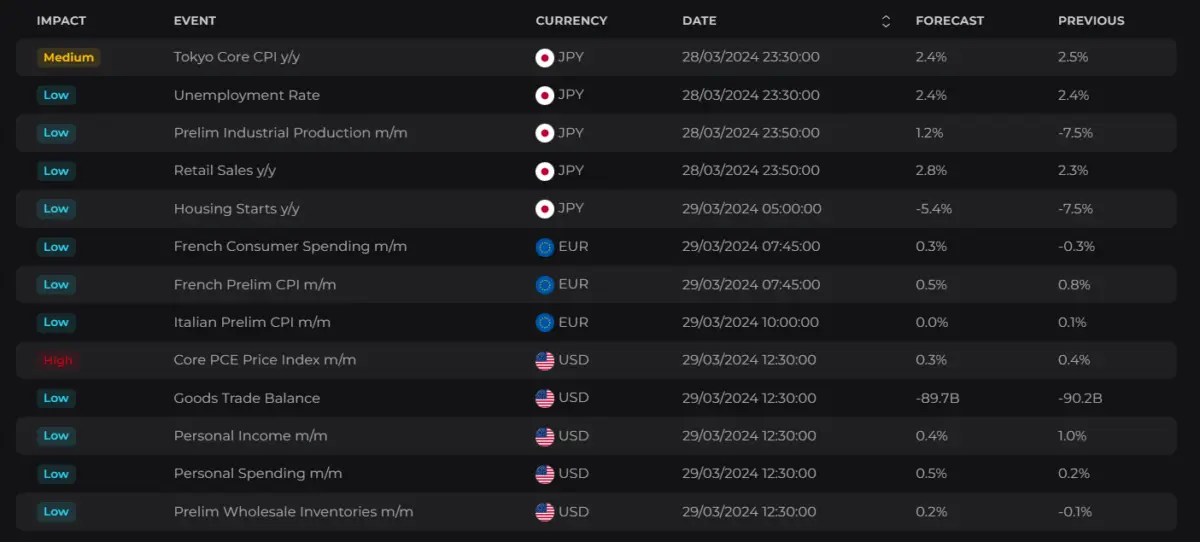

Japan will release a crucial set of data later in the evening, starting with the Unemployment Rate at 11:30 pm, followed by CPI figures for Tokyo, Japan’s largest economy. Twenty minutes after these releases, Japan will also report monthly changes in Industrial Production and Retail Sales.

Friday, March 29th, 2024

Further inflation data from European economies is scheduled for release on Friday. France, the second-largest economy in the Euro Area (EA), will unveil its Preliminary Inflation Rate at 7:45 am, followed by Italy, the third-largest EA economy, at 10:00 am.

In the US, Core PCE prices, which exclude food and energy costs, will be released at 12:30 pm. This data will also provide detailed insights into consumer spending and income, representing some of the most crucial information from the US this week. The week will conclude with Jerome Powell participating in a moderated discussion with Kai Ryssdal at the Federal Reserve Bank of San Francisco’s Macroeconomics and Monetary Policy Conference.

Speeches:

- 03:30 pm – FED Jerome Powell

Article topics

Trade with E8 Markets

Start our evaluation and get opportunity to start earning.Suggested Articles:

Disclaimer

The information provided on this website is for informational purposes only and should not be construed as investment advice. Always conduct your own research and consult with a qualified financial advisor before making any investment decisions. We do not endorse or promote any specific investments, and any decisions you make are at your own risk. This website and its content are not responsible for any financial losses or gains you may experience.

Please consult with a legal professional to ensure this disclaimer complies with any applicable laws and regulations in your jurisdiction.