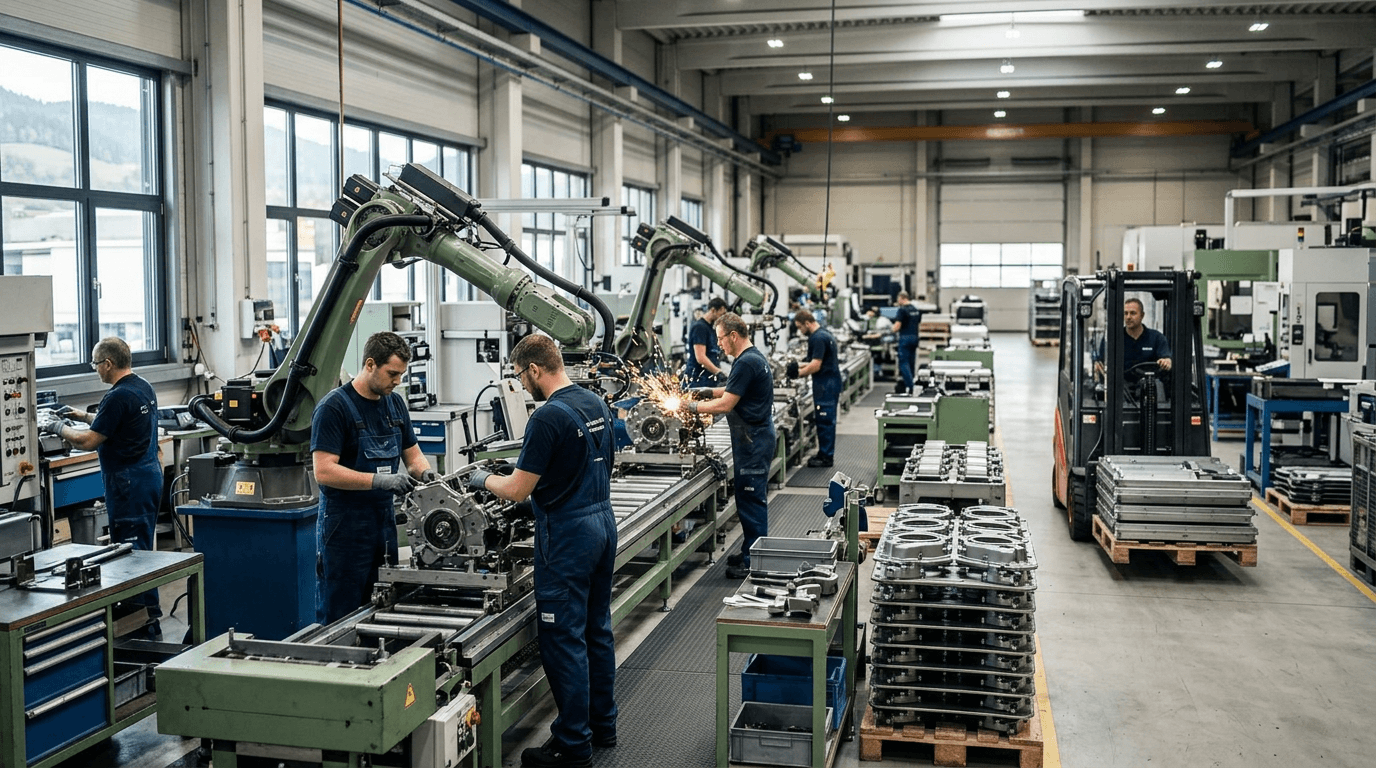

Austria's manufacturing sector is currently experiencing a robust upswing, marking its strongest performance in nearly four years. This surge signals a potential turning point for one of Europe's key industrial economies. The UniCredit Bank Austria Manufacturing Purchasing Managers' Index (PMI) rose sharply to 52.4 in March 2026, up from 49.4 in February. This marks the fastest expansion since May 2022, providing encouraging signs for the broader eurozone economic recovery. After two consecutive years of economic contraction, Austria's economy expanded by 0.6% in 2025, overcoming persistent challenges in construction and related sectors.

Decoding the PMI Surge

The Purchasing Managers' Index is a vital early indicator of manufacturing health, with any score above 50 indicating sector expansion. Austria's rise from the mid-40s to 52.4 reflects a significant acceleration, showcasing growing confidence among manufacturers and increased business activity. This expansion level, unseen since May 2022, predates the slowdown that affected European manufacturing throughout 2023 and 2024.

This recovery's strength is significant as it shows Austrian manufacturers responding positively to market conditions, despite global challenges. The growth, following two years of economic contraction, highlights the cyclical nature of industrial activity and suggests that pent-up demand is finally being released into the manufacturing sector.

Supply Chain Disruptions Fueling Demand

A primary catalyst for the March surge appears to be supply chain anxieties triggered by geopolitical tensions in the Middle East. As firms worry about potential disruptions to global logistics and material flows, many are building safety stocks and securing inventory against possible bottlenecks. This defensive buying behavior, although not the most sustainable growth driver, translates into real increases in new orders and production activity.

New orders saw their fastest growth in nearly four years, indicating that customers actively seek Austrian manufacturing capacity to diversify their supply chains and mitigate risk. German demand was notably strong, with export orders rising for only the second time in nearly four years, as manufacturers in Europe's largest economy turn to Austria for alternative sourcing options. This regional strength suggests Austria's industrial base remains competitive and capable of capturing additional market share amid global supply chain reconfiguration.

The Inflation Dilemma

While output and order expansion represent positive momentum, Austrian manufacturers face significant cost pressures that could limit profitability and future investment. Input price inflation reached its highest level since October 2022, driven by surging energy, fuel, and transportation costs exacerbated by the Middle East crisis. For an energy-intensive manufacturing economy like Austria, maintaining margins amid these cost increases poses a real challenge.

Moreover, selling price inflation has climbed to a 37-month high as manufacturers attempt to pass increased costs to customers. This dynamic creates tension between maintaining competitiveness in export markets and protecting profitability. Manufacturers must choose between absorbing cost increases or risking losing price-sensitive customers to lower-cost alternatives.

Employment Trends and Future Outlook

Despite strong output and orders, employment indicators offer a more cautious signal about the recovery's sustainability. Manufacturing employment has continued to decline, though the rate of job losses moderated to its weakest pace in three months. This pattern suggests manufacturers may focus on productivity improvements and efficiency gains rather than expanding headcount, a common strategy during economic uncertainty.

Looking ahead, the outlook remains mixed. Output expectations for the next 12 months have dropped to their lowest level since September 2025, with manufacturers expressing concerns about future demand sustainability and the cumulative impact of price increases. This forward-looking pessimism contrasts sharply with the current strength in orders, implying that firms view the recent surge as potentially temporary or driven by inventory building rather than underlying demand growth.

Implications for the Broader Economy

Austria's manufacturing revival has broad implications beyond the factory floor. The manufacturing sector, a significant portion of Austrian economic activity, typically leads broader economic trends. If current momentum can be sustained beyond the inventory-building phase, it could support faster overall economic growth in 2026 and provide employment opportunities as firms expand capacity.

However, persistent inflation, geopolitical uncertainty, and moderating forward expectations suggest caution is warranted. The 0.6% growth achieved in 2025 provides a baseline, but significantly faster expansion will require more durable demand sources beyond supply chain anxiety-driven purchasing.

The surge in Austrian manufacturing represents a genuine improvement in industrial conditions and offers hope that Europe's middle-tier economies can maintain momentum even as major economies face mixed signals. Whether this March strength marks the beginning of a sustained recovery or merely a cyclical bounce within a broader period of mediocre growth will become clear in the coming months as new orders data and employment figures continue to develop.

---