## Navigating the Eurozone's Evolving Inflation Landscape

As the Eurozone's inflation dynamics continue to shift, traders find themselves in a complex environment that demands astute attention. Core inflation breached the European Central Bank's (ECB) 2% target in late 2025, but emerging geopolitical forces have reshaped expectations for 2026. For those invested in euro-denominated assets, understanding these changes is crucial, especially as they relate to central bank policies affecting currency markets.

### The Recent Inflation Trajectory

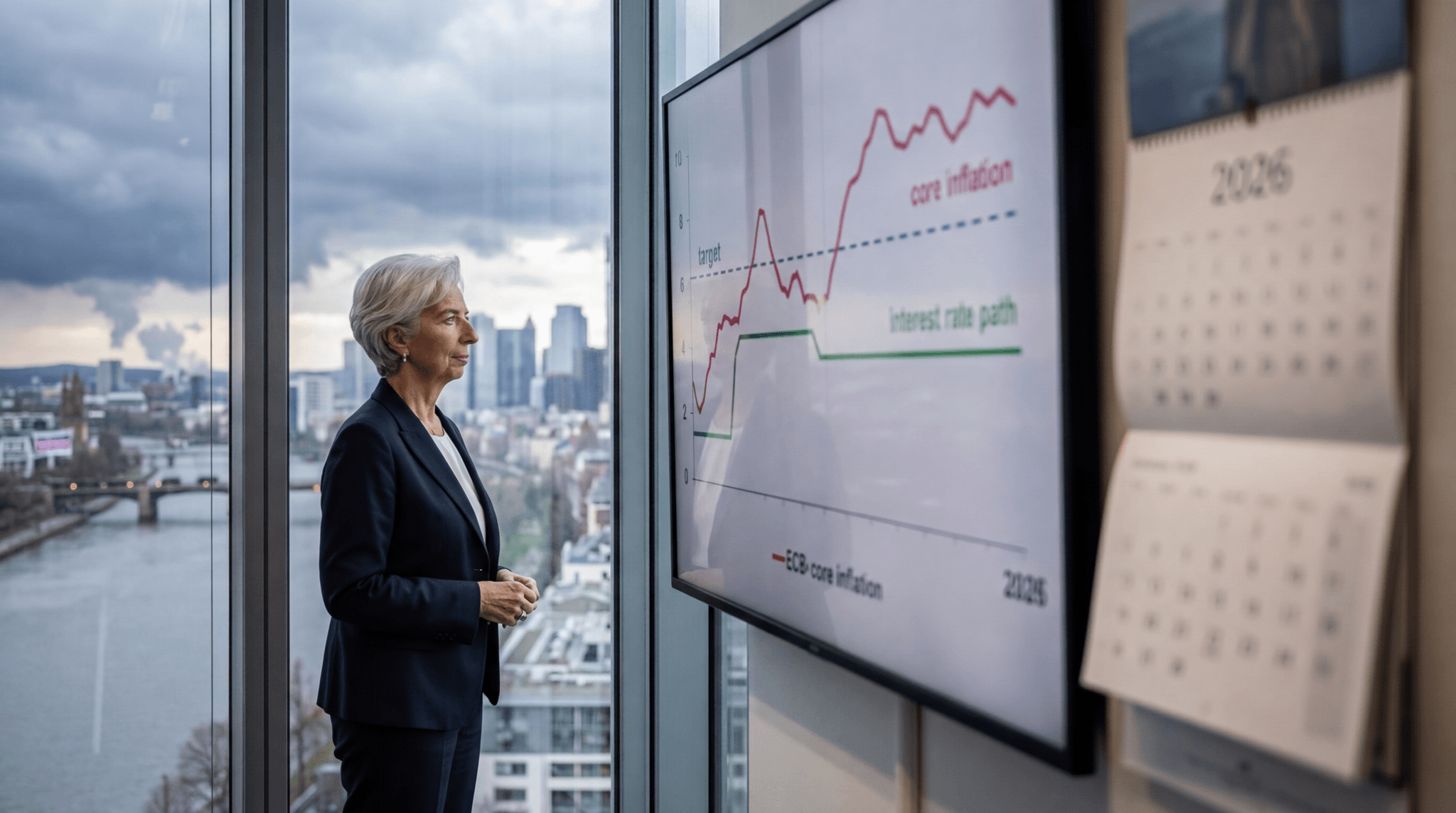

Throughout late 2025 and into early 2026, Eurozone core inflation remained stubbornly above the ECB's target for price stability. In November 2025, core inflation was at 2.4% year-on-year, moderating slightly to 2.3% by December as underlying pressures began to ease. This continued elevation above 2% was significant, suggesting that the sharp inflationary surge from previous years wasn't dissipating as quickly as anticipated. By January 2026, headline inflation dropped more notably to 1.7%, primarily due to declines in energy prices rather than widespread disinflation. Services inflation, however, was resilient, reaching 3.4% in December, highlighting ongoing price pressures in labor-intensive sectors.

### March's Pivotal Changes

March 2026 marked a turning point as the ECB shifted its stance. Contrary to expectations of rate cuts, the central bank held rates steady and increased its inflation forecasts for the year. Now, headline inflation is projected at 2.6% for 2026, far surpassing earlier forecasts of 1.9%. This adjustment is largely attributed to the Middle East conflict, which disrupted global energy markets and injected significant uncertainty into economic projections. The ECB also revised its 2026 GDP growth forecast downward to 0.9%, reflecting the conflict's dampening effects on consumer confidence and real incomes across the Eurozone.

### Implications for Interest Rate Policy

Keeping its key interest rates unchanged, the ECB noted that the main refinancing rate remains at 2.15%. Earlier in the year, market indicators suggested a 45% probability of rate cuts in 2026, but geopolitical shocks have shifted this outlook. The ECB emphasized a data-driven approach, not committing to a specific rate path. Policymakers pointed to risks in wage dynamics, global energy markets, and uneven demand across member states, suggesting a cautious stance. The ECB is likely to maintain this position unless economic conditions worsen substantially or inflation proves unexpectedly resilient.

### The Euro and Rate Expectations

When central banks maintain higher interest rates, their associated currencies typically benefit from increased yield attraction for international investors. The euro has remained stable around 1.1685 against the dollar in early 2026, with German Bund yields reflecting confidence in the ECB's inflation control strategy. However, the current environment is mixed for euro strength. While stable rates support the currency, the downward revision of growth forecasts and geopolitical uncertainties could hinder euro performance if risk appetite declines or the Eurozone economy lags behind major trading partners. Traders should monitor any divergence in monetary policy between the ECB and the Federal Reserve, as these have historically driven significant currency movements.

### Key Developments to Monitor

Looking ahead, several key developments require careful attention. First, the trajectory of energy prices will be critical, as disruptions in commodity markets directly impact inflation and policy expectations. Second, wage negotiations and labor market dynamics will determine whether core inflation can reliably move toward the 2% target. Third, upcoming ECB communications and economic data releases will offer insights into whether the central bank might eventually consider rate cuts later in 2026 or maintain its current stance. Lastly, the evolution of the Middle East situation could dramatically alter inflation and growth outlooks, with significant implications for ECB policy and euro valuations.

The consensus among major financial institutions suggests the ECB will likely hold rates steady through at least mid-2026, with significant policy adjustments potentially postponed until inflation dynamics become clearer and geopolitical risks diminish. This steady approach generally supports euro stability, although traders should be aware that downside risks to growth could eventually prompt the ECB to ease if economic conditions worsen more than currently expected.

NEWSIMPACTSCORE: 6