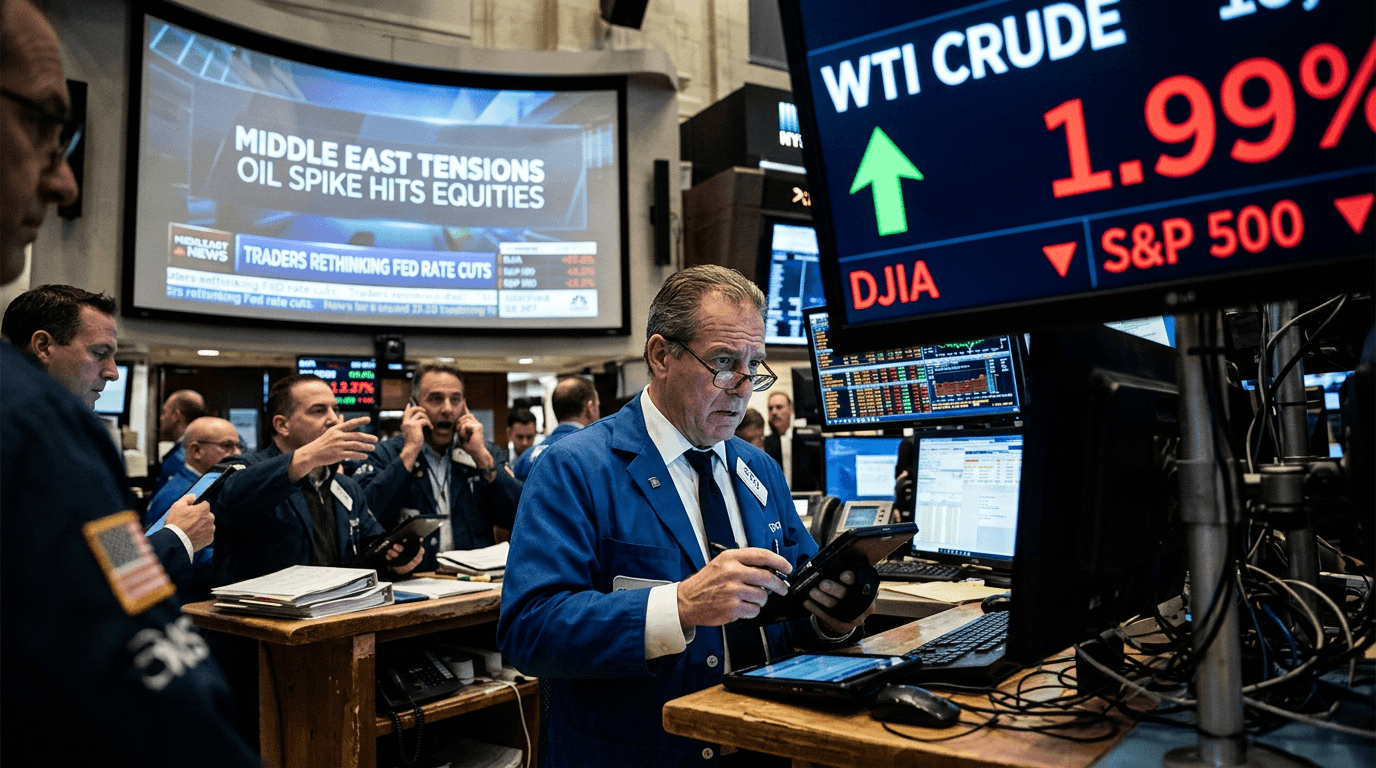

A sudden 9% spike in oil prices has ripped through global markets, pushing crude to recent highs, weighing on U.S. equities, and forcing traders to reassess how quickly the Federal Reserve can cut interest rates. The move is not just about energy; it is a macro shock that touches everything from inflation expectations to sector leadership on Wall Street.

WHAT’S DRIVING THE OIL SPIKE?

The catalyst is an escalation of conflict involving Iran and its neighbors, raising the risk of disruption to production and shipping routes in one of the world’s most critical energy corridors.[3][4] As military actions intensified, concerns grew that supply from the broader Middle East could be constrained, even if actual barrels have not yet been significantly shut in.[4][5]

In response, crude prices have jumped sharply. Brent, the global benchmark, has seen intraday moves of around 9%, trading above $100 per barrel in recent sessions.[3][7] U.S. oil benchmarks have also surged, with prices in the mid‑90s as traders price in a higher geopolitical risk premium.[2][7] In some episodes, prices were up nearly 9% even after giving back part of the initial spike.[6]

The shock is already visible at the pump. Average U.S. gasoline prices have risen by roughly 50 cents in a week, while diesel, crucial for shipping and logistics, has climbed by more than 80 cents per gallon.[3] That kind of jump feeds directly into business costs and consumer wallets, amplifying the macro impact of the oil move.

HOW HIGHER OIL PRICES HIT U.S. EQUITIES

The equity market reaction has been swift and negative. When energy costs spike, they act like a tax on the economy: consumers have less disposable income, companies face higher input costs, and profit margins are squeezed, especially in energy‑intensive industries.

Several channels are at work

- Cost pressure on corporates: Airlines, shipping, trucking, chemicals, and manufacturing names see fuel and feedstock costs surge. With limited ability to pass on all of those costs immediately, earnings expectations can be revised lower.

- Consumer squeeze: Higher gasoline prices reduce real disposable income, particularly for lower‑ and middle‑income households that spend a larger share of their budget on fuel.[3] That can weigh on discretionary retailers, restaurants, travel, and leisure.

- Risk‑off sentiment: Geopolitical risk itself tends to push investors toward safer assets. Cyclical and growth equities often come under pressure as uncertainty rises, while investors favor cash, short‑term bonds, or defensive sectors.

There is one clear winner: the energy sector. Oil producers, refiners, and some service companies may benefit from wider margins and higher realized prices, at least in the short run. That can create a stark divergence within equity markets—energy and some commodities up, broader indices under pressure, and rate‑sensitive growth names particularly vulnerable.

INFLATION, THE FED, AND RATE‑CUT ODDS

The most important macro question is what this oil spike means for inflation and the Federal Reserve’s path for interest rates.

Energy is a direct component of inflation indices. Higher gasoline and fuel prices feed into headline CPI and PCE, and if sustained, can bleed into core measures through transportation costs, goods prices, and wage demands. Recent price jumps of around 9% in crude and sharp weekly increases in retail fuel prices raise the risk of an upside surprise in upcoming inflation prints.[3]

For the Fed, this complicates the picture. Before the latest tension, markets had been pricing in a series of rate cuts as inflation trended lower and growth showed signs of moderation. A fresh oil‑driven inflation impulse does two things:

- It increases uncertainty about whether inflation will return to target on the desired timeline.

- It reduces the Fed’s room to deliver rapid or aggressive rate cuts without risking a resurgence of inflation expectations.

As a result, traders have begun to trim expectations for near‑term cuts and push out the timing of the first move lower in rates. The bond market’s reaction typically shows up as higher yields on the front end of the curve, reflecting a higher “terminal rate” for longer or a slower easing cycle.

To monitor this, macro‑focused traders watch Fed funds futures and interest‑rate options closely, looking at how many basis points of cuts are priced in for the next few meetings and for the full year. A persistent oil shock that keeps Brent elevated—analysts have floated ranges of $80–$90 or higher in conflict scenarios—can keep the Fed cautious.[4]

Trading And Investing Implications

For active traders and investors, a move like this is both a risk and an opportunity. A few practical considerations:

- Respect the volatility: Oil moves of 5–10% in a single session are not normal. They often come with wider bid‑ask spreads, faster intraday swings, and higher realized volatility across related assets. Position sizing and risk management become critical.

- Watch cross‑asset correlations: Rising oil prices can correlate with a weaker equity market, a stronger U.S. dollar, and changing yield curves. Macro trades that used to be uncorrelated may start moving together.

- Sector rotation: Energy, certain commodities, and some defense‑related names may outperform, while airlines, logistics, and consumer discretionary could lag. Allocating or hedging at the sector level can be more effective than broad index exposure in this environment.

- Scenario thinking: Build at least three scenarios—rapid de‑escalation and oil retracement; prolonged tension with elevated but stable prices; and a severe disruption, such as major shipping interruptions through the Strait of Hormuz, that could push Brent well above $100.[4][5] For each, consider how equities, yields, credit spreads, and currencies might respond.

Simulated or paper trading environments can be useful laboratories for testing how a macro‑driven shock affects a portfolio without real capital at risk. They allow traders to experiment with hedges, adjust leverage, and practice trading around key event risks such as inflation data or central bank meetings.

Key Takeaways And What To Watch Next

For now, the market is grappling with a classic stagflation‑style risk: slower growth prospects from higher energy costs, combined with renewed inflation pressure that may keep interest rates higher for longer. That is a challenging mix for risk assets and helps explain why U.S. equities have come under pressure even as energy names rally.

Key takeaways

- A roughly 9% jump in oil prices tied to Middle East tensions has pushed crude to recent highs and driven a sharp rise in retail fuel costs.[3][6]

- Higher energy prices are undermining U.S. equities by squeezing margins, hurting consumer spending, and raising macro uncertainty.

- The inflation impulse from energy is reducing the odds of near‑term Federal Reserve rate cuts as markets re‑price the path of policy.

- Traders should focus on risk management, sector rotation, and scenario analysis rather than short‑term predictions.

Going forward, the most important variables to watch are developments on the geopolitical front, evidence of any actual disruption to physical supply or shipping lanes, upcoming inflation and growth data, and Fed communication about how policymakers are weighing energy shocks against their dual mandate.[4][5] The situation remains fluid, but the message from markets is clear: as long as oil remains elevated on geopolitical risk, both equities and rate‑cut hopes will be under pressure.