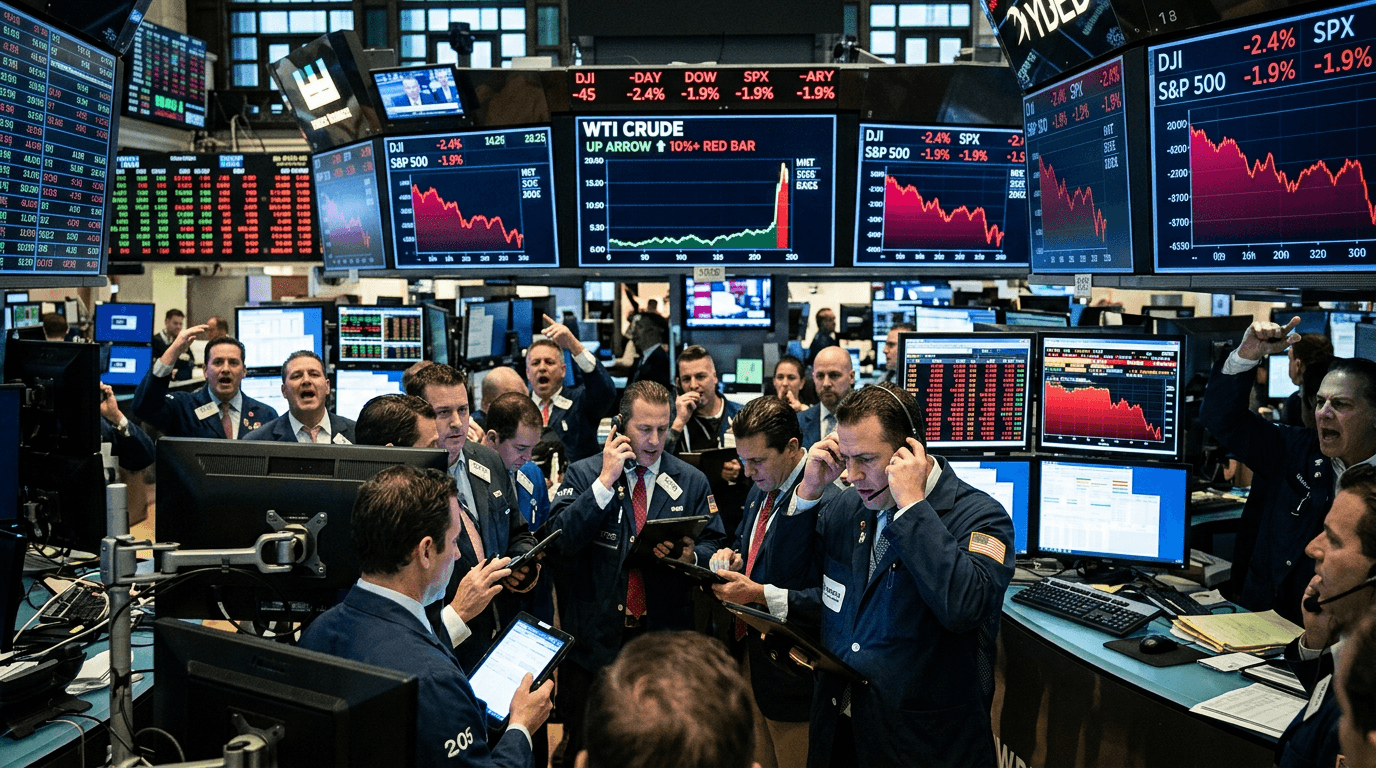

Oil’s latest jump, with US crude trading around $81.64 and Brent near $85.85, is a textbook reminder that geopolitics can move markets faster than economic data. War-related supply fears have jolted energy prices higher, knocked equities off recent highs, and revived worries that inflation could prove stickier than central banks – and investors – had hoped.[1][2] For traders, this is not just an oil story; it is a macro shock.

WHAT IS BEHIND THE LATEST OIL SPIKE?

The immediate driver is heightened geopolitical tension in key producing regions, including renewed conflict and threats to energy infrastructure and shipping lanes.[1][2][6] When a region that controls a large share of global exports is at risk, markets quickly price in the possibility that barrels may not reach customers on time, even if actual supply has not yet fallen.[1][6]

History shows that when infrastructure is attacked or transit chokepoints such as the Strait of Hormuz are threatened, oil can surge double digits in a matter of hours.[1][6] Futures markets are forward-looking: traders pay up for insurance against worst-case scenarios, and that “risk premium” gets embedded into prices almost instantly.

These moves are amplified by positioning and algorithmic trading. In calm periods, many funds run with lower volatility assumptions and higher leverage; when a geopolitical headline hits, models recalibrate, volatility spikes, and position-unwinding can accelerate the initial move in oil and related assets.[4] The result is a rapid, broad-based repricing of risk.

From Oil To Inflation: The Transmission Channel

Higher oil prices matter because energy is a core input across the economy. More expensive crude quickly translates into higher fuel costs for transportation, airlines, shipping, and logistics, and eventually into the prices of goods that rely on those services.[2][3] For firms already facing tight margins, the choice is either to absorb the cost hit or pass it on to consumers.

If companies pass those costs through, headline inflation measures tend to rise in the following months, as happened in prior conflict-driven oil shocks.[2][3] Central banks, which had begun to talk more confidently about disinflation, then face a tougher trade-off: tolerate higher inflation for longer or signal tighter policy, even as growth risks increase.[2]

Analysts note that prolonged energy shocks can trim growth while pushing inflation higher – the classic “stagflationary” mix.[2][3] Vanguard’s scenario analysis, for example, shows that sustained very high energy prices can shave around a percentage point off euro area GDP and tilt the economy toward recession.[3] The longer the conflict drags on, the larger the potential hit.

Why Equities Are Under Pressure

Equity markets do not like sudden spikes in input costs, especially when paired with elevated geopolitical risk. In past episodes of Middle East flare-ups, US index futures weakened as traders priced in lower profit margins, softer demand, and higher discount rates for future cash flows.[1][4] This time is no different: higher oil is feeding a “risk-off” move that leaves major indices under pressure.

The impact is uneven across sectors. Energy producers and some commodity-linked names can benefit from higher realized prices, but energy-intensive sectors such as airlines, transport, chemicals, and parts of manufacturing tend to suffer.[1][5] Consumer discretionary stocks may also struggle if households divert more income to fuel and utilities, leaving less room for optional spending.

Valuations matter, too. When risk-free yields are already elevated, a fresh inflation scare can push bond yields higher and compress the multiples investors are willing to pay for growth stories.[2][4] Expensive, long-duration assets – such as richly valued tech stocks – are particularly sensitive to shifts in interest rate expectations and risk premiums.[2]

Safe Havens, Bonds And Currencies

One of the clearest signals of stress during an oil shock is the rotation into perceived safe havens. In previous spikes tied to geopolitical headlines, flows into government bonds, the US dollar, and gold have picked up as investors seek protection from both market volatility and worst-case conflict scenarios.[1][4][7] That pattern is resurfacing as energy prices jump and equity volatility climbs.

Bond markets face a tug-of-war. On one side, higher oil and inflation expectations argue for higher yields; on the other, risk aversion and demand for safety support government debt prices.[2][4] The result is often not a clear trend, but higher rate volatility, which can be challenging for leveraged trades in fixed income and credit.

Volatility indices like the VIX tend to rise as markets digest headlines and reassess risk.[4] Elevated volatility does not automatically mean a crash is coming, but it does change the opportunity set: options become more expensive, intraday ranges widen, and traders need to adjust both their sizing and their expectations.

How Traders And Investors Can Navigate The Shock

The key for traders is not to predict every geopolitical twist, but to understand the transmission chain: from conflict risk to oil, from oil to inflation and central bank expectations, and from there to equities, bonds, and currencies.[1][2] Once you see that map clearly, you can build scenarios and plan responses rather than trading every headline impulsively.

One important lesson from history is that many geopolitically driven oil surges are sharp but not permanent.[1] As emergency supply is tapped, other producers ramp up, or demand softens, prices often retrace part of the initial move.[1][3] That does not mean this time will be identical, but it argues for focusing on the duration and scale of the disruption rather than the first-day spike.

For equity traders, this environment rewards selective positioning. Consider: - Which sectors are hurt most by higher fuel and input costs? - Which companies have pricing power to pass through inflation? - How might a higher-for-longer rate path change valuations across your watchlist?[2]

For macro and index traders, monitoring correlations is critical. Oil’s relationship with the dollar, real yields, and equity indices can shift depending on whether markets are more focused on growth or inflation risk.[2][4] Elevated volatility also makes risk management central: using predefined stop levels, smaller position sizes, and scenario testing can help avoid outsized drawdowns.

Simulated finance environments can be particularly useful in this kind of regime. They allow traders to stress-test strategies against oil shocks, experiment with sector rotation, or explore hedging approaches – such as tilting toward energy producers or inflation-protected assets – without real capital at risk. The goal is to turn a volatile, headline-driven period into a learning laboratory.

Key Takeaways

The latest spike in oil prices is a clear reminder that geopolitical risk remains a powerful driver of markets. It is pressuring equities, lifting inflation concerns, and complicating the outlook for central banks that were hoping for a smooth disinflation narrative.[1][2] For now, the move is meaningful but not yet at levels historically associated with severe global damage, making the duration of the conflict and supply disruption the critical variables.[2][3]

For traders and investors, the priority is disciplined adaptation. Understand how energy prices flow through to inflation and policy, identify which assets in your portfolio are most exposed, and adjust risk accordingly. Oil shocks are uncomfortable, but for prepared and well-educated market participants, they also create opportunities to refine strategies, test assumptions, and potentially find mispriced assets across the global market landscape.