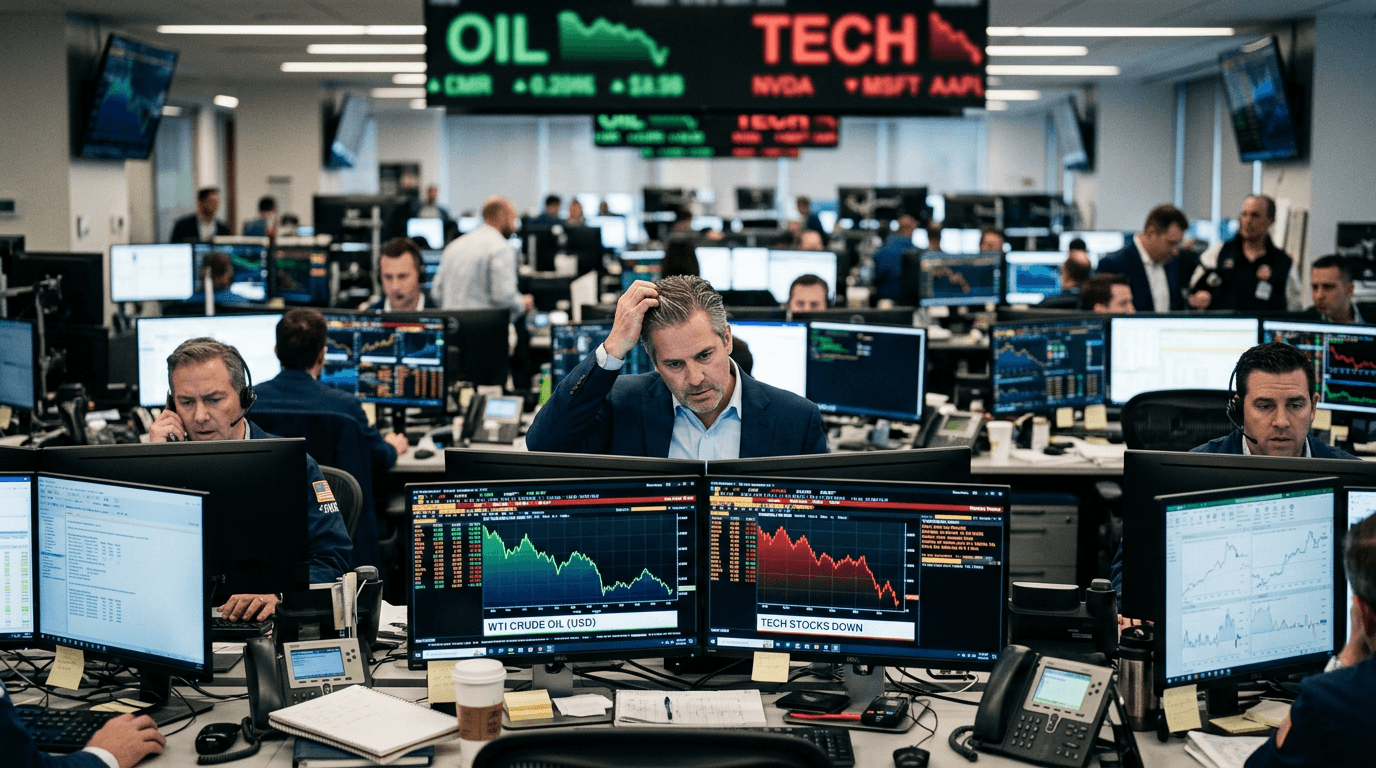

When bond markets sigh in relief but tech stocks start to sweat, traders know they’re looking at a more complicated story than a single headline suggests. The latest move lower in oil prices pushed Treasury yields down and briefly eased inflation fears, yet U.S. equities – especially high‑growth technology names – struggled. This divergence between fixed‑income relief and equity‑market anxiety is a timely reminder that markets rarely move in lockstep, and that narrative matters just as much as data.

Market Snapshot: Oil, Bonds, And Equities

When oil prices fall sharply, the first place traders look is the bond market. Lower energy costs tend to reduce headline inflation and, by extension, lower the perceived need for aggressive central bank tightening. That dynamic played out as crude slipped to a multi‑month low, with Treasury yields retreating and bond futures catching a bid.

In theory, falling yields are a positive for equities, particularly for long‑duration assets like tech stocks whose future cash flows are more sensitive to discount rates. Yet the equity tape told a different story. The S&P 500 and Nasdaq remained under pressure, even as bond yields moved down. That performance gap signals that traders are focusing less on the rate backdrop and more on valuation, earnings sustainability, and positioning risk in crowded tech trades.

The takeaway: lower yields are no longer an automatic green light for buying growth. Equity investors are weighing multiple forces at once, including stretched valuations, momentum fatigue, and sector‑specific risks.

Why Tech Is Nervous While Bonds Are Relieved

To understand why tech is jittery, it helps to think in terms of time horizons. Bond markets are largely reacting to macro signals: inflation data, energy prices, and central bank expectations. Equity investors, especially in tech, are balancing those macro inputs with micro risk: earnings durability, competitive dynamics, and the cost of funding massive AI and cloud investments.

Over the past year, mega‑cap tech and semiconductor names have delivered outsized gains driven by AI optimism, structural growth narratives, and enormous capital inflows. That rally effectively pulled forward years of expected returns. When prices embed a lot of future perfection, even a benign move in rates may not be enough to keep the momentum going.

So while bond traders see falling oil and lower yields as a simple “less inflation, more breathing room” story, tech equity traders are asking tougher questions: Are earnings expectations too optimistic? Have AI‑linked stocks become crowded trades? Is the market pricing in a growth scenario that’s difficult to sustain if global demand slows? As a result, any sign of macro uncertainty or sector‑specific stress can trigger profit‑taking, even in a supportive rate environment.

The takeaway: tech weakness in the face of lower yields reflects valuation and positioning stress, not a simple macro contradiction.

Valuations, Ai Hype, And The Froth Question

The phrase “high tech valuations” is doing a lot of work in this environment. Many leading tech and AI‑related names now trade at multiples that assume strong earnings growth for years. That’s not inherently unreasonable for structurally advantaged companies, but it leaves little margin for error.

Recent trading has highlighted three sources of discomfort:

First, earnings expectations are lofty. Markets are demanding that tech firms not only deliver strong results, but also guide confidently on AI monetization, cloud profitability, and enterprise demand. Any hint of a plateau can trigger outsized downside.

Second, AI optimism has created pockets of speculative fervor. Certain chipmakers and high‑beta software names have seen parabolic runs, followed by sharp intraday reversals. These swings suggest that some investors are trading narrative rather than fundamentals.

Third, sector leadership has grown narrow. A handful of giants have carried index performance, increasing concentration risk. When those leaders wobble, broad indices feel the impact quickly, even if other sectors are stable or improving.

Put together, these factors make tech vulnerable to “valuation shock” – moments where investors collectively reassess how much future growth they’re willing to pay for. That reassessment can occur even when the macro backdrop, including yields, looks more supportive.

The takeaway: the real risk isn’t that tech is expensive in isolation; it’s that expectations, positioning, and index concentration magnify every wobble.

Implications For Active Traders And Simulated Finance

For active traders, the divergence between bonds and tech equities creates both opportunity and complexity. Rate‑sensitive instruments may be pricing in a smoother inflation path thanks to lower oil, while equity markets are signaling caution around growth assumptions and sector crowding. That mismatch gives traders room to test relative‑value and cross‑asset strategies.

In a Simulated Finance (SimFi) environment, like trading on a platform such as E8 Markets, this kind of regime is particularly valuable. It allows traders to:

Experiment with equity‑index versus bond‑future pairs, exploring how spreads behave when macro and micro narratives diverge.

Practice trading sector rotation, shifting simulated exposure between tech, defensives (such as utilities and staples), and cyclicals as sentiment evolves.

Test volatility and option‑based strategies that profit from elevated tech swings without taking real‑world capital risk.

Because the moves are driven by both valuation reassessment and macro data, they offer a realistic sandbox for learning how different asset classes communicate – and sometimes disagree – about the future.

The takeaway: simulated trading is well suited to this environment, letting traders stress‑test strategies in a market shaped by conflicting signals.

HOW TRADERS CAN NAVIGATE THESE CROSS‑CURRENTS

When bonds rally on lower yields but tech stays under pressure, traders need a framework that goes beyond simple “risk‑on/risk‑off” thinking. A few practical guidelines can help:

Separate macro from micro. Treat rate moves and inflation expectations as one layer of the story, and sector‑specific earnings and valuation risks as another. Don’t assume they must always point in the same direction.

Watch leadership and breadth. Track whether a handful of names are driving tech weakness or whether selling is broad‑based across growth. Narrow leadership increases vulnerability to sharp reversals.

Respect positioning risk. Crowded trades, especially in AI‑linked stocks, can reverse violently on relatively small news. Use simulated environments to practice risk management and position sizing.

Plan for volatility, not just direction. Elevated uncertainty around tech valuations and AI earnings paths means intraday swings can be large in both directions. Structure trades with clear exit rules, and test different scenarios in a SimFi setting before deploying real capital.

In short, this episode of tech jitters amid bond‑market relief underscores a central lesson for modern traders: markets can interpret the same data through different lenses. Oil and yields may be telling one story about inflation, but tech valuations and investor positioning are telling another about growth and risk appetite. The traders who perform best are often those who can hold both ideas in mind and build strategies that respect the complexity of the tape.